The need for presenting the real-time traffic info to passengers and drivers is one of the main factors driving the demand for the market. Development in emergency services and traffic management empowers the authorities to quickly respond to the accidents and emergencies with more efficiency. Usage of such systems maximizes efficacy in shortens the travel duration and traffic management. The use of various public transportation results in reduction of airborne pollutants and the carbon dioxide emissions.

High traffic jamming due to increasing number of automobiles has contributed to need for progressive public traffic management systems. Consequent need for smart vehicles with the public-private partnerships is expected to be major growth driver. Various initiatives undertaken to organise advanced traffic management systems (TMS) such as Vehicle-to-Vehicle and Vehicle-to-Infrastructure (V2I) communication is projected to be some of the key growth strategies.

Segment Overview

Based on application, the ITS market can be categorised into traffic management, , freight management, environment protection, public transport, automotive telematics, road safety and security, road user charging, and parking management.

The U.S. traffic management segment is likely to command maximum market share from 2019 to 2025. ITS deployment is mainly driven by the government regulations in North America and Europe. Traffic Management Systems (TMS) operation performance and enhance reliability of road networks. They include the vehicle detection systems, ramp metering systems bridge traffic management systems, among others. Growing traffic jams result in traffic time, fuel wastage, and monetary losses. They adversely impact socio-economic development and growth of a country. Hence, traffic management systems are installed to minimize financial burden on transport authorities and governments.

Regional Overview

The U.S. Department of Transportation has been investing heavily in R and D, adoption, and the deployment of ITS across region. DOT and University of Michigan Transportation Research Institute directed a Safety Pilot Model Deployment in Michigan from the year 2015 to 2013 using DSRC-enabled apparatus in real world environment. Furthermore, in 2015, DOT declared that push towards mandating theV2V technology in U.S. for all the light vehicles based on the SPMD.

The economic benefits of various IT deployment are mainly notable in developing markets such as Russia, Brazil, India, South Africa, China, and (BRICS) nations. Cooperative and In-vehicle systems not only provide monetary benefits to the car owners but also assistance in avoiding jammed routes and reducing overall fuel consumption and the travel time. Car manufacturers in various established and emerging economies are fitting the systems in car models to discriminate their products from the competitors.

Competitor overview

Key players in the market include Kapsch TrafficCom, Siemens AG, and Hitachi Ltd. This is largely on account of the diversified customer base and wide range of technologically advanced types employed in intelligent transportation system industry. Other noticeable vendors include Denso Corporation, Garmin International, Efkon Ag, and Lanner Electronics among others.

Key Players

- Agero, Inc.

- ADCCO LLC

- DENSO Corporation

- EFKON AG

- Hitachi Ltd.

- Garmin International, Inc.

- Iteris, Inc.

- Lanner Electronics, Inc.

- Nuance Communications, Inc.

- Ricardo PLC

Market Segmentation

By Type

- ATPS

- ATIS

- ATMS

- APTS

- EMS

- Freight Management

- Traffic Management

- Road Safety and Security

- Public Transport

- Automotive Telematics

- Parking Management

- Environment Protection

- Road Tolling System

- North America

- US

- Canada

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- UAE

- Rest of LAMEA

1 Executive Summary 20

2 Preface 21

- 2.1 Abstract 21

- 2.2 Stakeholder 21

- 2.3 Research Scope 22

- 2.4 Research Methodology 22

- 2.4.1 Data Mining 22

- 2.4.2 Data Validation 24

- 2.4.3 Research Approach 25

- 2.5 Research Sources 25

- 2.5.1 Primary Research Sources 25

- 2.5.2 Secondary Research Sources 26

- 2.5.3 Assumptions 26

3 Market Trends 27

- 3.1 Introduction 27

- 3.2 Drivers 28

- 3.2.1 Increasing Concern about Traffic Congestion 28

- 3.2.2 Increasing Need of Road Safety Improvements 28

- 3.2.3 Increasing Government Initiative 29

- 3.2.4 Shifting of Freight Industry from Unorganized to Organized Sector 29

- 3.2.5 Reduced Fatalities and Injuries 30

- 3.3 Restraints 30

- 3.3.1 Lack of Proper Infrastructure for Implementation of ITS in Developing and Under Developed Economies 30

- 3.3.2 High Cost for ITS Safety Systems Does Not Allow High Penetration 30

- 3.4 Opportunities 31

- 3.4.1 Successful Implementation of Connected Cars Technology Opening Doors for the Intelligent Transportation System 31

- 3.4.2 Increasing Demand of ITS will show the Significant Growth in Wireless Application that (includes device and application) 31

- 3.4.3 Implementation of Intelligent Transportation System helps for Smarter Mapping for Making Important Decision 32

- 3.5 Threats 32

- 3.5.1 Security Breach Related to Data Storage 32

- 3.6 Products 32

- 3.7 Application 33

- 3.8 Component 33

- 3.9 Emerging Market 34

4 Porters Five Force 35

- 4.1 Bargaining Power of suppliers 35

- 4.2 Bargaining Power of Buyers 35

- 4.3 Threat of Substitutes 35

- 4.4 Threat of New Entrants 36

- 4.5 Competitive Rivalry 36

5 Intelligent Transportation System (ITS) Market, By Product 37

- 5.1 Introduction 37

- 5.2 Advanced Transportation Management Systems (ATMS) 39

- 5.3 Advanced Public Transportation Systems (APTS) 40

- 5.4 Advanced Transportation Pricing Systems (ATPS) 41

- 5.5 Advanced Traveler Information Systems (ATIS) 42

- 5.6 Cooperative Vehicle Systems 43

6 Intelligent Transportation System (ITS) Market, By Applications 44

- 6.1 Introduction 44

- 6.2 Automotive Telematics 46

- 6.3 Traffic Management 47

- 6.4 Collision Avoidance system 48

- 6.5 Road User Charging 49

- 6.6 Road Safety and Security 49

- 6.7 Traffic Signal Control 50

- 6.8 Freight Management (Commercial) 51

- 6.9 Parking Management 52

- 6.10 Public Transport 53

- 6.11 Environment Protection 54

- 6.12 Traffic Enforcement Camera 55

7 Intelligent Transportation System (ITS) Market, By Component 56

- 7.1 Introduction 56

- 7.2 Sensor 57

- 7.2.1 Speed Sensor 58

- 7.2.2 Vehicle Detection Sensor 59

- 7.2.3 Pedestrian Presence Sensor 59

- 7.3 Surveillance Camera 60

- 7.3.1 AID Camera 61

- 7.3.2 Thermal Camera 61

- 7.4 Software 62

- 7.4.1 Transit Management System 62

- 7.4.2 Visualization Software 63

- 7.4.3 Video Detection Management 63

- 7.4.4 Others 64

- 7.5 Interface Board 64

- 7.5.1 Vehicle Detection Board 65

- 7.5.2 Communication Board 65

- 7.5.3 Multifunctional Board 66

- 7.6 Monitoring and Detection System 66

- 7.6.1 Intelligent Traffic Controller 67

- 7.6.2 Automatic Number Plate Recognition 67

- 7.7 Telecommunication Network 68

- 7.7.1 Wireless 69

- 7.7.2 Fiber Optics 69

- 7.7.3 Copper Lines 70

- 7.8 Others 71

8 Intelligent Transportation System (ITS) Market, By Geography 72

- 8.1 North America 72

- 8.1.1 U.S. 72

- 8.1.2 Canada 73

- 8.1.3 Mexico 73

- 8.2 Europe 90

- 8.2.1 Germany 90

- 8.2.2 France 90

- 8.2.3 Italy 91

- 8.2.4 U.K. 91

- 8.2.5 Spain 91

- 8.2.6 Rest of Europe 92

- 8.3 Asia-Pacific 109

- 8.3.1 Japan 109

- 8.3.2 China 109

- 8.3.3 India 109

- 8.3.4 Australia 110

- 8.3.5 New Zealand 110

- 8.3.6 Rest of Asia-Pacific 110

- 8.4 Rest of the World 128

- 8.4.1 Middle East 128

- 8.4.2 Brazil 128

- 8.4.3 Argentina 128

- 8.4.4 South Africa 129

- 8.4.5 Egypt 129

9 Key Developments 147

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures 147

- 9.2 Acquisitions & Mergers 149

- 9.3 New Product Launch 151

- 9.4 Expansions 153

- 9.5 Other Key Strategies 154

10 Company Profiles 155

- 10.1 Roper Technologies, Inc. 155

- 10.1.1 Business Overview 155

- 10.1.2 SWOT Analysis 156

- 10.1.3 Financial Overview 156

- 10.1.4 Products Overview 156

- 10.1.5 Key Activities 157

- 10.2 Hitachi Ltd 158

- 10.2.1 Business Overview 158

- 10.2.2 SWOT Analysis 158

- 10.2.3 Financial Overview 159

- 10.2.4 Products Overview 159

- 10.2.5 Key Activities 160

- 10.3 Siemens AG 162

- 10.3.1 Business Overview 162

- 10.3.2 SWOT Analysis 162

- 10.3.3 Financial Overview 163

- 10.3.4 Products Overview 163

- 10.3.5 Key Activities 163

- 10.4 Thales Group 165

- 10.4.1 Business Overview 165

- 10.4.2 SWOT Analysis 165

- 10.4.3 Financial Overview 166

- 10.4.4 Products Overview 166

- 10.4.5 Key Activities 167

- 10.5 Xerox Corporation 168

- 10.5.1 Business Overview 168

- 10.5.2 SWOT Analysis 168

- 10.5.3 Financial Overview 169

- 10.5.4 Products Overview 169

- 10.5.5 Key Activities 170

- 10.6 BRISA 171

- 10.6.1 Business Overview 171

- 10.6.2 SWOT Analysis 171

- 10.6.3 Financial Overview 172

- 10.6.4 Products Overview 172

- 10.7 Kapsch Trafficcom 173

- 10.7.1 Business Overview 173

- 10.7.2 SWOT Analysis 173

- 10.7.3 Financial Overview 174

- 10.7.4 Products Overview 174

- 10.7.5 Key Activities 174

- 10.8 Q Free 175

- 10.8.1 Business Overview 175

- 10.8.2 SWOT Analysis 175

- 10.8.3 Financial Overview 176

- 10.8.4 Products Overview 176

- 10.8.5 Key Activities 177

- 10.9 Efkon AG 178

- 10.9.1 Business Overview 178

- 10.9.2 Products Overview 178

- 10.10 Lanner Electronics Inc. 179

- 10.10.1 Business Overview 179

- 10.10.2 Financial Overview 179

- 10.10.3 Products Overview 180

- 10.10.4 Key Activities 180

- 10.11 Denso Corporation 181

- 10.11.1 Business Overview 181

- 10.11.2 SWOT Analysis 181

- 10.11.3 Financial Overview 182

- 10.11.4 Products Overview 182

- 10.11.5 Key Activities 183

- 10.12 TomTom International BV 184

- 10.12.1 Business Overview 184

- 10.12.2 Financial Overview 184

- 10.12.3 Products Overview 184

- 10.12.4 Key Activities 185

- 10.13 Savari Inc. 186

- 10.13.1 Business Overview 186

- 10.13.2 Products Overview 186

- 10.14 Nuance Communications Inc. 187

- 10.14.1 Business Overview 187

- 10.14.2 SWOT Analysis 187

- 10.14.3 Financial Overview 187

- 10.14.4 Products Overview 188

- 10.14.5 Key Activities 188

- 10.15 Garmin Ltd. 190

- 10.15.1 Business Overview 190

- 10.15.2 SWOT Analysis 190

- 10.15.3 Financial Overview 191

- 10.15.4 roducts Overview 191

- 10.15.5 Key Activities 192

11 Appendix 193

- 11.1 Discussion Blue Print 193

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

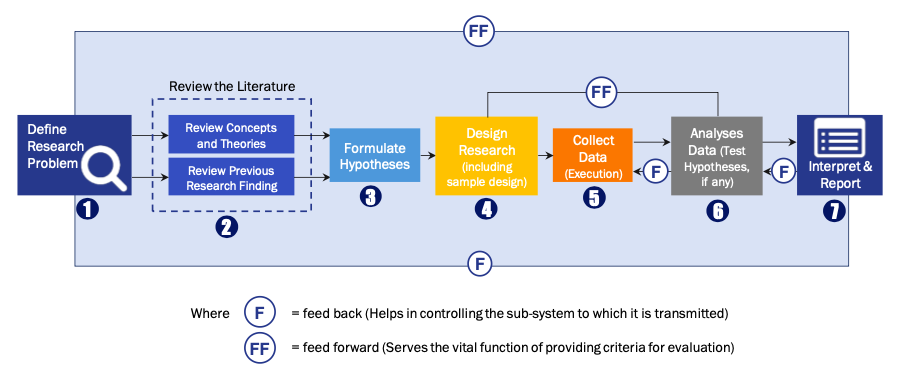

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model