As the COVID-19 pandemic continuing its effect around the world, many defense and aerospace companies are facing its impact during this time around the world. For instance, commercial aviation companies in the U.S., France, Germany, and Canada are facing disruption in the production process and reduced demand as workforces staying at home, passengers stop traveling, and delay in delivery of new aircraft. Analysts expecting a drop from 3,000 to 4,000 aircraft during the pandemic period. On the defense side, contractors operating in the sector are in a better position, hence the impact of the pandemic is likely low in the short to mid-term. However, low demand due to budget constraints affecting the production as in aircraft manufacturing.

Market Overview

The size of the global submarine market reduced drastically toward the end of the Cold War in 1991. However, since then, BRIC countries and other developing countries in Asia-Pacific are investing in the market to strengthen their naval capabilities.

Factors such as growing demand for UUVs, rising investments for submarines, use of nuclear energy, and regional disputes between countries have fueled the need for nuclear submarines. 3D printing or additive manufacturing helps the manufacturers create and design things in an innovative way that surpass conventional methods such as computerized numerical control (CNC) cutting, mold manufacturing, and canvas printing. This is expected to create growth opportunities for players operating in the global market.

The submarine market is expected to register a significant CAGR during the forecast period. The growing emphasis of many countries toward modernizing their naval defense units, like submarines, surface-mine countermeasures, unmanned underwater vehicles, and other combat and tactical UUVs, is expected to drive the submarine market in the coming years. The increasing maritime threats, like sea-based terrorism and other illegal activities, pose a challenge to the militaries. In order to counter these challenges, submarines are used for surveillance and under-sea attack purposes.

The growing emphasis on the indigenous production of advanced submarines by various countries is opening new avenues for the market.

Segment Overview

Currently, the SSN segment has the highest market share out of all the segments. The militaries of several countries opt for these submarines owing to their advantages, such as being faster, more efficient, and having longer endurance capabilities. In addition, SSN submarines do not have to dive to surface periodically for air, which preserves their stealth attribute. Owing to these advantages and their better warfare capabilities, the SSN segment is projected to register the highest CAGR during the forecast period.

Regional Overview

In 2018, North America dominated the submarine market, due to the factors, such as the high military spending of the United States and the aggressive procurement of submarines, coupled with the increased focus on unmanned underwater vehicles. Additionally, the revenues from North America are projected to register the highest CAGR during the forecast period. The development of advanced submarines and the focus of the United States on procuring next-generation submarines are the main reasons for the high anticipated growth of the market in the region. Moreover, increasing focus on the Virginia-class submarines that are being built by the United States may contribute to the strong growth of the market in the region, in the coming years.

Competitor overview

Huntington Ingalls Industries, BAE Systems PLC, Daewoo Shipbuilding & Marine Engineering, General Dynamics Corporation, and Hyundai Heavy Industries are some of the prominent players in the market. Major players in the market are trying to make use of the technological advancements to develop and launch new generation submarines, thereby, attracting a larger range of customers. Countries in Asia-Pacific are investing huge amounts for procuring new submarines. Players can shift their focus on these countries from countries, like the United States, which have already made long-term contracts with the existing players. Acquisitions of other players can help the existing players gain a huge market share. In January 2019, Hyundai Heavy Industries Group signed a deal to consolidate two of South Korea's biggest shipbuilders, thereby, helping Hyundai Heavy Industries Group to increase its market revenues.

Key Players

- Navantia

- Naval Group

- FINCANTIERI SpA

- Huntington Ingalls Industries

- Hyundai Heavy Industries

- General Dynamics Electric Boat

- BAE Systems PLC

- Daewoo Shipbuilding & Marine Engineering

- Saab AB

- ThyssenKrupp Marine Systems

- United Shipbuilding Corporation

- ASC PTY LTD

Market Segmentation

By Type

- SSBN submarine

- SSN submarine

- SSK submarine

- North America

- US

- Canada

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- UAE

- Rest of LAMEA

Request for TOC

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

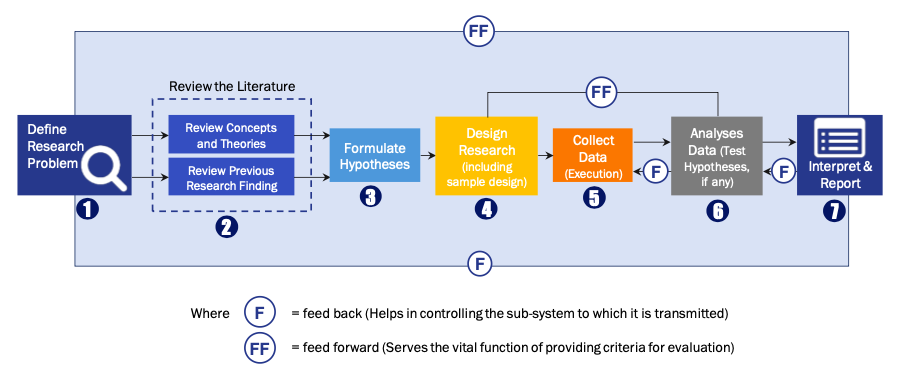

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model