Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Apheresis Equipment Market refers to the industry focused on devices and technologies used to separate and collect specific components of blood, such as plasma, platelets, leukocytes, or red blood cells, while returning the remaining components to the patient or donor. Apheresis equipment is widely used in therapeutic treatments and blood component collection procedures in hospitals, blood banks, and research institutions. These systems play an essential role in managing diseases such as autoimmune disorders, hematologic conditions, and neurological diseases, as well as in plasma and platelet donations. Increasing demand for blood components, advancements in medical technology, and growing adoption of therapeutic apheresis are driving market expansion globally.

The apheresis equipment market is evolving with several technological and healthcare trends. One major trend is the growing adoption of automated and portable apheresis systems that improve procedural efficiency and patient safety. Advancements in centrifugation technology and membrane filtration systems are enhancing separation accuracy and reducing treatment time. Another trend is the rising use of therapeutic apheresis in treating autoimmune diseases, neurological disorders, and haematological conditions. Additionally, the expansion of plasma collection centres to support biopharmaceutical manufacturing is driving equipment demand. Integration of digital monitoring, improved disposables, and user-friendly system interfaces is also transforming clinical workflows and enabling broader adoption of apheresis technologies worldwide.

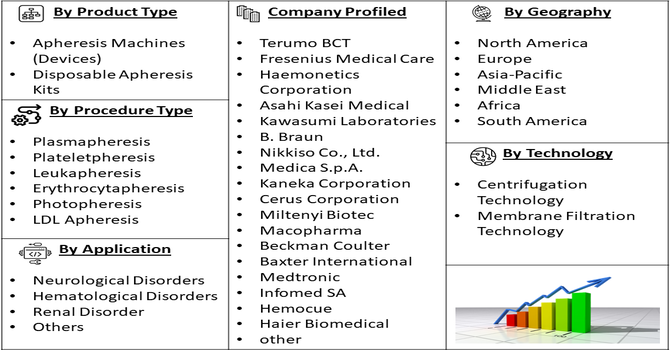

Segmentation: The Global Apheresis Equipment Market is segmented by Product Type (Apheresis Machines (Devices) and Disposable Apheresis Kits), Technology (Centrifugation Technology and Membrane Filtration Technology), Procedure Type (Plasmapheresis, Plateletpheresis, Leukapheresis, Erythrocytapheresis, Photopheresis, LDL Apheresis and Others), Application (Neurological Disorders, Hematological Disorders, Renal Disorder and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The rising demand for blood components such as plasma, platelets, and red blood cells is a major driver of the global apheresis equipment market. Plasma-derived therapies are widely used to treat immune deficiencies, bleeding disorders, neurological diseases, and other chronic conditions. With increasing prevalence of such diseases and growing healthcare awareness, the need for efficient blood component collection technologies has significantly increased. Apheresis equipment enables selective collection of specific blood components while maintaining donor safety and efficiency. Additionally, the rapid growth of the biopharmaceutical industry and rising demand for plasma-based therapeutics are encouraging expansion of plasma donation centers, further boosting demand for advanced apheresis systems worldwide.

The increasing use of therapeutic apheresis in the treatment of various medical conditions is another key factor driving market growth. Therapeutic apheresis procedures help remove harmful substances such as autoantibodies, toxins, or abnormal proteins from the blood, making them effective in treating autoimmune diseases, neurological disorders, and hematologic conditions.

As medical research continues to demonstrate the clinical benefits of apheresis therapy, healthcare providers are increasingly adopting these procedures in specialized treatment protocols. The strategic localization initiative by Terumo Blood and Cell Technologies in partnership with Terumo Medical Products (Hangzhou) Co., Ltd. in 2024 strengthened the global apheresis equipment market by expanding local manufacturing capabilities in China. The move improved product availability, reduced supply chain barriers, and supported broader adoption of advanced blood collection technologies.

Advancements in automated apheresis equipment have also improved treatment efficiency, safety, and patient comfort. These developments are encouraging hospitals and clinics to integrate apheresis technologies into routine disease management practices.

Market Restraints:

The major restraint affecting the global apheresis equipment market is the high cost associated with purchasing and maintaining advanced apheresis systems. These devices require significant capital investment, specialized consumables, and trained medical professionals to operate them effectively. Additionally, therapeutic apheresis procedures can be expensive, which may limit accessibility in low- and middle-income countries where healthcare budgets are constrained. Maintenance, regulatory compliance, and disposable kit costs further increase the overall treatment expenses. As a result, some hospitals and blood collection centers may hesitate to adopt these systems, potentially slowing market growth in cost-sensitive regions despite increasing demand for blood component therapies.

The socioeconomic impact of the apheresis equipment market is significant because these technologies support life-saving treatments and blood component collection essential for modern healthcare. Apheresis procedures enable targeted treatment for patients with complex diseases, reducing hospitalization duration and improving quality of life. Increasing availability of plasma-derived therapies and platelet transfusions contributes to better outcomes for patients with immune disorders, cancer, and rare diseases. The expansion of plasma collection centers also generates employment opportunities and stimulates growth in the healthcare and biopharmaceutical industries. Furthermore, investments in blood donation infrastructure and medical technology are strengthening healthcare systems and improving access to advanced therapeutic treatments worldwide.

Segmental Analysis:

The Disposable Apheresis Kits segment is expected to witness the highest growth over the forecast period due to the increasing demand for safe and infection-free blood component collection procedures. Healthcare providers are increasingly adopting single-use kits to minimize the risk of cross-contamination and ensure compliance with strict safety regulations in blood banks and hospitals. The rising number of blood donations, growing awareness about apheresis procedures, and the expansion of plasma collection centers are also contributing to market growth. In addition, technological advancements in kit design that enhance efficiency and reduce procedure time are supporting adoption. The expanding use of apheresis in therapeutic treatments and component separation further strengthens the growth potential of disposable apheresis kits.

The Centrifugation Technology segment is anticipated to experience the highest growth during the forecast period owing to its widespread use in efficient blood component separation. This technology enables precise separation of plasma, platelets, red blood cells, and other blood components, making it highly valuable in clinical and therapeutic applications. Increasing demand for blood components in the treatment of chronic diseases, trauma cases, and surgical procedures is driving adoption. Furthermore, advancements in centrifugation systems that improve automation, accuracy, and processing speed are enhancing operational efficiency in hospitals and blood banks. Growing investments in healthcare infrastructure and rising awareness about component-based transfusion therapies are expected to further accelerate the demand for centrifugation-based apheresis technologies.

The Plateletpheresis segment is expected to witness the highest growth over the forecast period due to the rising demand for platelets in the treatment of various medical conditions. Platelet transfusions are critical for patients undergoing chemotherapy, bone marrow transplantation, and major surgeries, as well as those suffering from blood disorders that affect platelet production. The increasing incidence of cancer and other chronic diseases is significantly contributing to the growing need for platelet collection procedures. Additionally, plateletpheresis allows the collection of a higher concentration of platelets from a single donor, improving treatment efficiency and reducing the need for multiple donors. Advancements in apheresis devices and increasing awareness about voluntary platelet donation further support segment growth.

The Haematological Disorders segment is projected to witness the highest growth over the forecast period as apheresis therapies play an important role in the management and treatment of various blood-related conditions. Disorders such as leukemia, lymphoma, sickle cell disease, and other immune-mediated blood diseases often require therapeutic apheresis to remove abnormal cells or harmful substances from the bloodstream. The increasing prevalence of these disorders, along with improved diagnostic capabilities, is driving demand for advanced treatment options. In addition, growing adoption of apheresis in hospitals and specialty clinics for disease management is contributing to market expansion. Rising healthcare expenditure and ongoing research focused on innovative therapeutic applications are further supporting the growth of this segment.

The North American region is expected to witness the highest growth over the forecast period due to the presence of advanced healthcare infrastructure and strong adoption of innovative medical technologies.

The region benefits from a well-established network of blood banks, plasma collection centers, and specialized treatment facilities that support the widespread use of apheresis procedures. For instance, in January 2025, the 510(k)-clearance granted by the U.S. Food and Drug Administration for the Aurora Xi automated plasma separator strengthened the global apheresis equipment market by introducing membrane-based plasma separation that reduced platelet damage and improved single-donor platelet yield. This advancement supported efficiency in blood banks and encouraged adoption of next-generation apheresis technologies.

Moreover, the increasing prevalence of chronic and haematological diseases, along with a growing number of surgical procedures, is driving demand for blood component therapies. For instance, in 2025, Blood Cancer United, stated reported that an estimated combined total of 192,070 people in the US are expected to be diagnosed with leukaemia, lymphoma or myeloma in 2025.

In addition, supportive government initiatives, favourable reimbursement policies, and strong research and development activities by leading healthcare companies are contributing to regional market growth. Rising awareness about blood donation and component-based transfusion therapy further supports expansion.

| Report Matrics | Details |

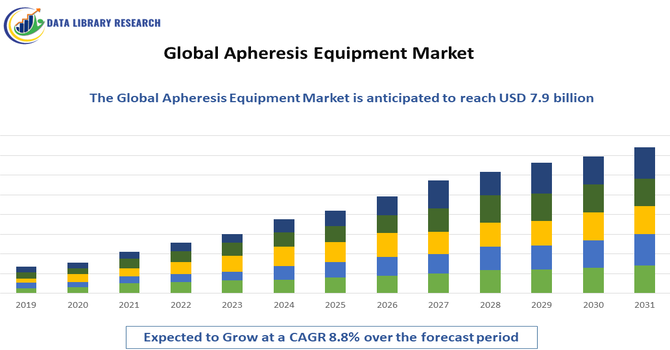

| Market Size Value | USD 7.9 billion |

| Growth Rate | CAGR of 8.8% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The global apheresis equipment market is highly competitive, with several multinational medical technology companies dominating the sector alongside specialized manufacturers. Leading players focus on developing advanced automated apheresis systems, disposable kits, and integrated software solutions to enhance treatment efficiency and safety. Companies compete through product innovation, regulatory approvals, and expansion of plasma collection networks. Strategic collaborations with hospitals, blood banks, and research organizations are also common to increase adoption of therapeutic apheresis technologies. Additionally, firms are investing in research and development to improve device portability, automation, and patient comfort, enabling them to strengthen their market positions in both developed and emerging healthcare markets.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

Market growth is primarily driven by the rising demand for source plasma used in biopharmaceuticals and the increasing prevalence of chronic diseases like leukemia and autoimmune disorders. Advancements in automated blood separation technology and a growing global focus on personalized medicine and cell therapies are further accelerating the adoption of apheresis equipment.

Q2. What are the main restraining factors for this market??

Growth is significantly hindered by the high cost of apheresis machines and disposable kits, which limits access in budget-constrained regions. A global shortage of skilled medical professionals to operate complex equipment and stringent donor recruitment criteria also pose challenges. Additionally, the risk of procedure-related complications and varying regional regulatory hurdles can slow market expansion.

Q3. Which segment is expected to witness high growth?

The Disposable Apheresis Kits segment was expected to witness the highest growth over the forecast period due to increasing demand for safe and sterile blood component collection procedures. Rising adoption of single-use medical devices, expanding plasma collection activities, and growing therapeutic apheresis applications across hospitals and blood banks further supported segment growth.

Q4. Who are the top major players for this market?

The market is dominated by a few global technology leaders, including Terumo BCT, Fresenius Medical Care (Fresenius Kabi), and Haemonetics Corporation. Other significant players driving innovation through advanced separation systems and consumables include Asahi Kasei Medical, Baxter International, B. Braun Melsungen AG, and Mallinckrodt (Therakos).

Q5. Which country is the largest player?

The United States is the largest market player, in the global share. Its dominance is sustained by a robust healthcare infrastructure, high investment in R&D for blood-related therapies, and a massive network of blood and plasma donation centers that early-adopt sophisticated automated apheresis technologies.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model