Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Data Center Thermal Management Market involves solutions and technologies designed to regulate and control the heat generated within data centers to ensure efficient performance, reliability, and reduced energy consumption. Thermal management encompasses cooling hardware (chillers, heat exchangers), liquid and air based systems, smart monitoring, and control software that optimize temperature and humidity across server racks and critical infrastructure.

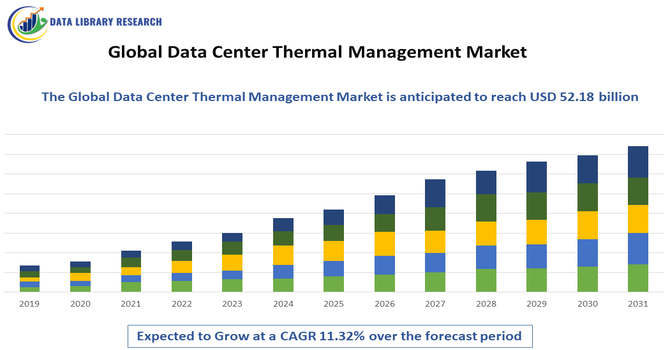

As data centers expand with high performance computing, AI, hyperscale, and edge facilities, advanced cooling and thermal analytics are essential for maintaining optimal operating conditions, lowering power usage effectiveness (PUE), and meeting sustainability targets. Market growth is driven by rapid digital transformation and sustainability mandates globally.

The Global Data Center Thermal Management Market witnessed significant technological evolution, focusing on AI driven cooling optimization and liquid and immersion cooling adoption to meet escalating heat loads from high density servers. Advanced solutions employing machine learning and IoT sensors dynamically adjusted airflow and cooling based on real time data, improving efficiency and reliability. Liquid and hybrid cooling systems gained traction due to superior thermal control for artificial intelligence and high performance computing workloads. Modular and scalable cooling infrastructure became prominent for hyperscale and edge data centers, while sustainability imperatives pushed vendors to integrate energy efficient and eco friendly designs. North America remained a key adopter of cutting edge thermal solutions.

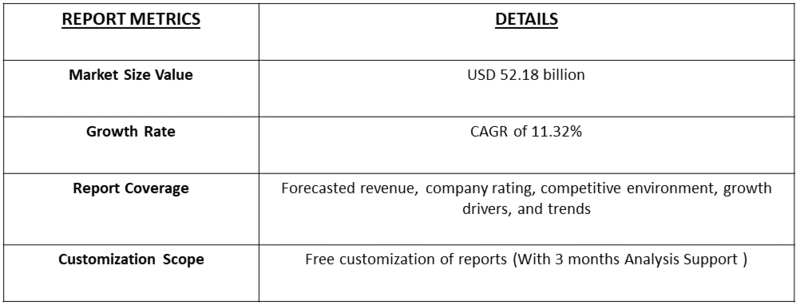

Segmentation: The Global Data Center Thermal Management Market is segmented by Solution Type (Air Cooling Systems, Liquid Cooling Systems, Cooling Infrastructure Components and Thermal Monitoring & Control Software), Cooling Technology (Air Based Cooling, Liquid Based Cooling and Hybrid Cooling), Deployment Type (On Premises Data Centers, Colocation Data Centers, Hyperscale Data Centers and Edge Data Centers), End Use Industry (IT & Telecom, BFSI (Banking, Financial Services, Insurance), Government & Public Sector, Healthcare & Life Sciences, Retail & E Commerce and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The major driver of the Global Data Centre Thermal Management Market was the rapid expansion of data centres driven by cloud computing, AI, and high performance workloads. As server density increased, heat generation rose proportionally, creating critical needs for advanced thermal management to maintain operational stability and prevent equipment failure.

Hyperscale and edge facilities required scalable, efficient cooling systems to balance performance with uptime reliability. For instance, in October 2024, Wieland acquired Onda S.p.A., enhancing its thermal solutions portfolio. The merger strengthened capabilities in advanced heat exchangers, addressed growing data center heat loads, and supported global expansion, positively impacting the Global Data Center Thermal Management Market.

Operators aimed to reduce PUE and energy costs while ensuring uptime continuity, which accelerated adoption of precision cooling, liquid cooling, and hybrid solutions. This trend pushed investments toward smart, high efficiency thermal systems capable of addressing evolving infrastructure demands.

Environmental sustainability and energy efficiency mandates strongly propelled the Global Data Center Thermal Management Market. Data centers consume significant power, and cooling accounts for a large portion of that usage, prompting operators to pursue greener technologies to meet regulatory requirements and corporate ESG goals.

In Febraury 2026, Boyd expanded its Juarez, Mexico facility from 217,000 to 460,000 square feet, increasing production of AI data center liquid cooling systems. This expansion supported energy-efficient, sustainable thermal solutions and reinforced growth in the Global Data Center Thermal Management Market.

Vendors developed energy efficient systems, free cooling, and liquid immersion technologies that reduced electricity and water use. These solutions helped minimize carbon footprints and operational costs. Government incentives for clean infrastructure and investor focus on sustainable assets further boosted demand. The push for reduced emissions and eco friendly thermal management positioned data centers as leaders in technological sustainability.

Market Restraints:

A notable restraint on the Global Data Center Thermal Management Market was the high initial investment and integration complexity of advanced thermal systems. Deploying liquid cooling, immersion solutions, or AI driven controls required significant capital expenditure, specialized engineering expertise, and complex retrofitting in existing data centers. Many organizations, particularly SMEs, faced budget limitations and technical constraints, slowing adoption. Legacy infrastructure often lacked compatibility with newer thermal technologies, necessitating extensive redesigns. Skilled workforce shortages in thermal system design and maintenance further delayed implementation. These challenges restricted market expansion and adoption rates in regions with limited technical resources or funding, despite the clear long term efficiency benefits.

The Global Data Center Thermal Management Market contributed significantly to economic and environmental goals by enhancing energy efficiency, reducing operational costs, and supporting digital infrastructure growth. Efficient thermal systems lowered power and water consumption, assisting companies in meeting sustainability regulations and reducing carbon footprints. Investments in cooling and thermal analytics created jobs in R&D, manufacturing, and services, fostering specialized skill development. Advanced thermal solutions enabled reliable data center operation, which is critical for digital economies, cloud computing, and online services. Improved efficiency also bolstered competitiveness for enterprises reliant on high performance computing and AI, supporting broader technological adoption across sectors while aligning with global energy efficiency and ESG commitments.

Segmental Analysis:

The cooling infrastructure components segment witnessed the highest growth over the forecast period due to rising demand for critical supporting hardware such as chillers, cooling towers, pumps, and heat exchangers. These components enabled efficient thermal regulation in high-density data centers, ensuring server reliability and uptime. Investments in modular and scalable infrastructure allowed operators to optimize energy use and reduce power usage effectiveness (PUE). Growth was driven by hyperscale, colocation, and enterprise facilities upgrading legacy cooling systems. Advanced monitoring and AI-driven integration with these components further enhanced efficiency, reinforcing the segment as a major contributor to overall market expansion.

The air-based cooling segment experienced the highest growth over the forecast period due to widespread adoption in enterprise, colocation, and hyperscale data centers. Computer Room Air Conditioners (CRAC), Computer Room Air Handlers (CRAH), and precision air systems remained cost-effective, reliable, and easily deployable. Air-based solutions supported structured airflow management, hot/cold aisle containment, and energy efficiency initiatives. Investments in AI and IoT-enabled temperature monitoring enhanced precision and minimized energy waste. While liquid and hybrid cooling gained traction, air-based systems maintained dominance in regions with established infrastructure, contributing significantly to the market’s growth and providing flexible, scalable solutions for evolving thermal management demands.

The edge data centers segment witnessed the highest growth over the forecast period as demand surged for low-latency, distributed computing closer to end users. Compact, high-performance servers required advanced yet space-efficient thermal management solutions. Cooling technologies, including air, liquid, and hybrid systems, were adapted to smaller footprints and variable load profiles. The proliferation of IoT, 5G networks, and real-time applications accelerated edge deployments, creating opportunities for modular and energy-efficient cooling infrastructure. Vendors provided pre-integrated thermal solutions, reducing installation complexity. Growth was particularly strong in urban and industrial hubs where localized computing and low-latency services were essential, driving adoption of specialized edge cooling solutions.

The IT & telecom end-use segment witnessed the highest growth over the forecast period due to rapid expansion of cloud computing, hyperscale data centers, and telecom infrastructure. Rising demand for high-speed connectivity, 5G rollout, and cloud-based services significantly increased data center density and heat generation. Thermal management solutions, including precision air conditioning, liquid cooling, and smart monitoring, became critical for uptime, reliability, and energy efficiency. Investment in AI-driven cooling, predictive analytics, and hybrid systems allowed operators to optimize operations. The segment’s growth was fueled by global digital transformation, the increasing volume of data traffic, and regulatory pressure to maintain energy-efficient and sustainable data center operations.

The North American region witnessed the highest growth over the forecast period due to a mature data center ecosystem, early adoption of advanced cooling technologies, and significant investment in hyperscale and cloud infrastructure. Stringent environmental regulations and sustainability mandates encouraged deployment of energy-efficient thermal solutions, including AI-driven air management and liquid cooling.

Major cloud providers and enterprises upgraded legacy systems to reduce PUE and operational costs. For instance, in December 2024, Schneider Electric launched AI-ready data center solutions with NVIDIA, including a 132 kW-per-rack liquid-cooled AI cluster and compact Galaxy VXL UPS, which enhanced efficiency, accelerated adoption of advanced cooling, and boosted North America’s Data Center Thermal Management Market growth.

Strong R&D capabilities, availability of skilled workforce, and robust distribution networks supported the adoption of cutting-edge thermal management technologies. North America remained a key market, leading innovation and setting global standards for energy-efficient and sustainable data center operations.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Data Center Thermal Management Market was shaped by established multinational corporations and innovative niche firms. Large players dominated through extensive product portfolios, strong R&D capabilities, global service networks, and strategic partnerships. Companies competed on energy efficiency, smart controls, and integrated thermal management solutions. New entrants in liquid and immersion cooling introduced disruptive technologies, intensifying innovation based competition. Regional players gained traction in emerging markets by providing localized solutions with tailored support and competitive pricing. Vendors sought differentiation through AI enabled predictive cooling, modular units, and sustainability focused designs. Collaborative ventures and acquisitions strengthened capabilities and expanded market reach.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The explosive growth of Artificial Intelligence (AI) and High-Performance Computing (HPC) is the primary driver, as these technologies require massive power densities that generate intense heat. Additionally, the global expansion of 5G networks and cloud services necessitates more edge data centers, significantly increasing the demand for advanced cooling infrastructure.

Q2. What are the main restraining factors for this market?

High initial capital expenditure for advanced cooling systems, such as liquid cooling, acts as a significant barrier for many operators. Additionally, the high energy consumption of traditional cooling methods conflicts with strict global carbon emission regulations, forcing companies to find a balance between thermal efficiency and environmental sustainability goals.

Q3. Which segment is expected to witness high growth?

The cooling infrastructure components segment was expected to witness the highest growth over the forecast period due to increased demand for chillers, pumps, heat exchangers, and cooling towers. Rising data center density, hyperscale expansions, and modernization of legacy systems drove adoption, while AI-enabled integration enhanced energy efficiency and operational reliability.

Q4. Who are the top major players for this market?

The market is led by established infrastructure giants including Vertiv Holdings Co., Schneider Electric, and Eaton. Other dominant players include STULZ GmbH, Rittal, and Asetek. These companies are currently focusing on modular cooling solutions and strategic partnerships with chipmakers to optimize thermal management for next-generation silicon architectures and hardware.

Q5. Which country is the largest player?

The United States is the largest player in this market. It hosts the world’s highest concentration of hyperscale data centers owned by tech giants like Google, Microsoft, and AWS. Massive investments in domestic AI infrastructure and a robust focus on energy-efficient cooling technologies keep the U.S. at the forefront.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model