Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Energy-efficient Dry-type Power Transformer Market refers to the global industry for transformers that distribute electrical energy without liquid insulation and are designed to minimize energy losses, enhance safety, and meet regulatory efficiency standards. These transformers use advanced insulation materials such as cast resin and vacuum pressure-impregnated systems to reduce no-load and load losses while improving thermal performance and reliability. Energy-efficient dry-type transformers are widely used in industrial, commercial, utility, and renewable energy applications due to their fire-resistant, low-maintenance, and eco-friendly characteristics, aligning with global sustainability goals and strict safety norms in modern electrical infrastructure.

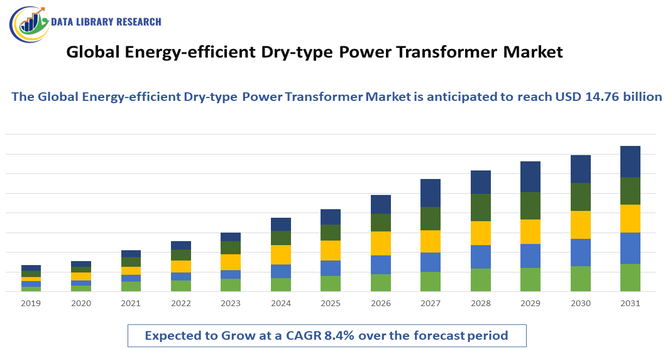

Market trends show strong adoption of energy-efficient dry-type transformers driven by stringent fire-safety and environmental regulations and the global push toward carbon reduction. These units are increasingly integrated into renewable energy systems, smart grids, and digitized power distribution networks with embedded sensors and predictive analytics. Asia-Pacific leads growth due to rapid urbanization, infrastructure expansion, and renewable deployment. Demand is rising from data centers, metro rail systems, and commercial buildings seeking compact, low-loss, and safer distribution solutions. Smart monitoring and IoT integration further enhance reliability and reduce operating costs, strengthening long-term adoption of energy-efficient dry-type transformers worldwide.

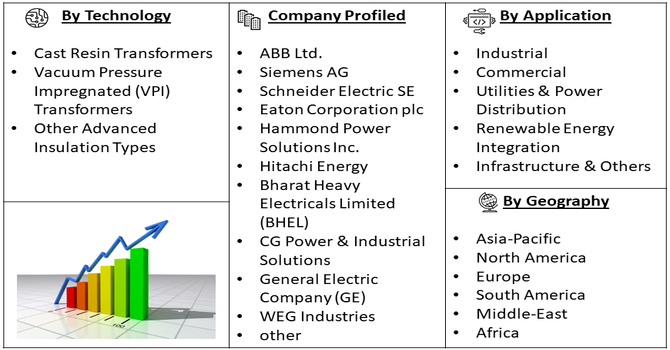

Segmentation: The Energy-efficient Dry-type Power Transformer Market is segmented by Technology (Cast Resin Transformers, Vacuum Pressure Impregnated (VPI) Transformers and Other Advanced Insulation Types), Phase (Single-Phase Dry-type Transformers and Three-Phase Dry-type Transformers), Voltage Level (Low Voltage – up to ~1 kV, Medium Voltage – commonly 1-36 kV and High Voltage – above ~36 kV ), Power Rating (Up to 500 kVA, 501 kVA to 2000 kVA and >2000 kVA), Application (Industrial, Commercial, Utilities & Power Distribution, Renewable Energy Integration and Infrastructure & Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

A primary driver is the global emphasis on energy efficiency and regulatory compliance, which pushes utilities and industries to adopt dry-type transformers with lower core and copper losses. These transformers help reduce electricity waste, support sustainability targets, and comply with minimum energy performance standards in regions like the EU and parts of Asia.

In January 2026, Farady Electric strengthened its global expansion strategy by participating in the IEEE PES Transmission and Distribution Conference in the United States, showcasing advanced dry-type and liquid-filled transformers tailored for North America. Its presence emphasized energy efficiency, regulatory compliance, and sustainable grid solutions, reinforcing growth momentum in the energy-efficient dry-type power transformer market.

Enhanced efficiency also leads to lower lifecycle costs and aligns with corporate ESG goals, encouraging capital investment in advanced dry-type designs that reduce both no-load and load losses. The shift from conventional oil-filled transformers to energy-efficient dry types accelerates as grid modernization and electrification efforts expand worldwide.

Another key driver is the demand for safer, fire-resistant distribution solutions in dense urban and critical environments. Dry-type transformers eliminate the risk of oil leaks or explosions, making them ideal for indoor spaces, high-rise buildings, and underground substations. Rapid urbanization and infrastructure expansion increase demand for reliable power systems that also integrate seamlessly with renewable energy sources. As renewable capacity grows, dry-type transformers are often chosen for distributed generation and smart grid applications due to their environmental compatibility and robustness in variable load conditions, reinforcing market growth.

Market Restraints:

The relatively high upfront capital cost compared to traditional oil-filled transformers. Advanced insulation materials like epoxy resin and vacuum pressure-impregnated systems, along with precision engineering to achieve low losses, drive production costs higher. This high initial investment can deter price-sensitive buyers, especially in developing economies and large utility projects where budget constraints are critical. Additionally, dry-type units currently have limitations in very high-voltage applications, restricting their adoption in certain segments. The longer payback period on efficiency gains and installation cost sensitivity remain barriers to broader market penetration.

The energy-efficient dry-type transformer market contributes significantly to socioeconomic development by improving power reliability and safety across utilities, industries, and cities. Enhanced energy efficiency reduces electricity waste, leading to lower operating costs for businesses and utilities and supporting broader sustainability targets. Adoption in urban infrastructure and critical facilities like hospitals and data centers enhances resilience and reduces outage risks. Job creation in manufacturing, installation, maintenance, and smart-grid integration drives economic growth, particularly in emerging economies undertaking grid modernization and electrification initiatives. Furthermore, reduced fire and environmental risks positively impact public safety, lowering insurance costs and helping countries meet environmental and energy performance regulations.

Segmental Analysis:

The Vacuum Pressure Impregnated (VPI) transformers segment is expected to witness the highest growth over the forecast period due to its superior insulation performance and enhanced electrical reliability compared with conventional cast-resin designs. VPI transformers undergo a process where insulation materials are thoroughly saturated under vacuum and pressure, significantly improving dielectric strength and moisture resistance. This makes them particularly suitable for harsh environments, critical industrial facilities, and high-efficiency applications demanding minimal maintenance. Moreover, increasing utility and industrial investments in reliable, fire-safe distribution equipment are driving preference for VPI units. With rising emphasis on energy conservation and regulatory efficiency norms, demand for technically advanced VPI dry-type transformers is projected to expand rapidly.

The three-phase dry-type transformers segment is anticipated to register the highest growth over the forecast period as industries and utilities transition toward robust and efficient power distribution solutions. Three-phase transformers are essential for large-scale electrical systems because they deliver balanced power, support heavy loads, and enhance grid stability. As electrification expands across manufacturing, commercial infrastructure, and renewable energy projects, three-phase dry-type units are increasingly favored due to their safety advantages, lower fire risks, and reduced maintenance requirements compared with oil-filled alternatives. Urbanization, smart grid initiatives, and demand for energy-efficient technologies further propel adoption, making three-phase dry-type transformers a preferred choice for high-capacity electrical networks worldwide.

The medium voltage (commonly 1–36 kV) segment is projected to witness the highest growth throughout the forecast period, driven by widespread use in utility distribution systems, commercial complexes, and industrial facilities. Medium voltage dry-type transformers efficiently manage power between high-voltage transmission and low-voltage end users, offering an ideal balance of performance, safety, and cost. The absence of oil minimizes fire hazards, making them well-suited for indoor installations and environments with strict safety standards. Growth in infrastructure projects, electrification of industries, and renewable energy integration further boost demand for medium voltage solutions. Additionally, stringent energy efficiency regulations and technological advancements in insulation and core materials enhance performance, fostering faster market uptake.

The utilities & power distribution segment is expected to experience the highest growth during the forecast period, as power companies worldwide modernize and expand grid infrastructure to meet rising electricity demand. Energy-efficient dry-type transformers play a critical role in distribution networks by reducing losses, enhancing safety, and minimizing maintenance requirements compared with oil-filled alternatives. Utilities increasingly adopt these units for substations, urban networks, and sensitive load centers where fire safety and environmental compliance are priorities. The push toward smart grids, renewable integration, and decentralized generation further supports adoption, with dry-type transformers enabling efficient load balancing and improved grid stability. Growth in electrification initiatives, particularly in developing regions, reinforces the segment’s momentum.

The North American region is expected to witness the highest growth over the forecast period, driven by substantial investments in grid modernization, industrial electrification, and stringent safety and efficiency regulations. Utilities and commercial sectors in the United States and Canada are increasingly adopting energy-efficient dry-type transformers to replace aging infrastructure, reduce losses, and enhance reliability.

Rising electricity demand, increasing renewable energy installations, and strong government initiatives supporting grid modernization significantly drive market expansion. For instance, in April 2022, Siemens Energy introduced CAREPOLE, an innovative single-phase cast-resin pole-mounted dry-type transformer tailored for the American grid. The launch strengthened North America’s energy-efficient dry-type transformer market by offering a more reliable, durable, and environmentally friendly alternative to oil-filled units, accelerating sustainable grid modernization and boosting regional adoption rates.

The region’s growing commercial construction sector, including metro rail projects, smart cities, data centers, and high-rise buildings, further fuels demand for safe and energy-efficient dry-type transformers. For instance, in 2025, Hitachi Energy announced a USD 22.5 million investment to expand and modernize its dry-type transformer operations in Southwest Virginia, including a new 75,000-square-foot facility in Atkins and upgrades in Bland. The expansion increased production capacity, strengthened regional supply chains, and accelerated growth in North America’s energy-efficient dry-type transformer market.

Additionally, supportive regulatory policies promoting energy efficiency and reduced carbon emissions encourage utilities and industries to adopt advanced transformer technologies, positioning Asia-Pacific as the fastest-growing regional market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the energy-efficient dry-type transformer market is characterized by global electrical equipment leaders and regional specialists competing on innovation, product efficiency, safety features, and digital capabilities. Major multinational players focus on R&D, partnerships, and capacity expansion to address smart grid and renewable integration demands. Asia-Pacific manufacturers leverage cost advantages and growing regional demand, while North American and European firms emphasize advanced monitoring and high-efficiency designs. Competition also includes strategic collaborations, M&A, and expansion into emerging markets. Product differentiation via IoT-enabled condition monitoring, higher thermal class materials, and low-loss designs is critical for sustaining market share amid growing safety and sustainability requirements.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the global transition toward green energy and stringent government regulations aimed at reducing carbon footprints. Increasing investments in renewable energy integration, such as wind and solar, require efficient distribution. Additionally, the rapid expansion of data centers and the modernization of aging electrical grids prioritize fire-safe, low-maintenance solutions.

Q2. What are the main restraining factors for this market?

The high initial cost of energy-efficient dry-type transformers compared to traditional oil-immersed versions remains a significant barrier for price-sensitive regions. Technical limitations, such as lower heat dissipation efficiency and voltage capacity constraints, also restrict their use in extra-high-voltage applications. Furthermore, fluctuating raw material prices for copper and high-grade steel impact manufacturing.

Q3. Which segment is expected to witness high growth?

The Utilities & Power Distribution segment is expected to witness the highest growth over the forecast period due to rising electricity demand, grid modernization initiatives, and renewable energy integration. Energy-efficient dry-type transformers reduce transmission losses, enhance safety, and support decentralized power systems, making them ideal for upgraded substations and expanding urban distribution networks.

Q4. Who are the top major players for this market?

Key market leaders include ABB Ltd., Schneider Electric, Siemens AG, and Eaton Corporation. These companies dominate through extensive R&D and global distribution networks. Other prominent players such as Hammond Power Solutions, TBEA Co., Ltd., and CG Power and Industrial Solutions contribute significantly by offering customized, highly efficient solutions for diverse industrial needs.

Q5. Which country is the largest player?

The United States region is expected to witness the highest growth over the forecast period due to significant investments in grid modernization, renewable energy integration, and replacement of aging power infrastructure. Strict energy efficiency standards, rising demand from data centers and industrial facilities, and increased focus on fire-safe, environmentally friendly technologies further drive adoption of energy-efficient dry-type transformers nationwide.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model