Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Organic Acid Market refers to the worldwide industry involved in the production, distribution, and sale of organic acids such as citric acid, lactic acid, acetic acid, and gluconic acid. These acids are widely used in food and beverages, pharmaceuticals, cosmetics, agriculture, and industrial applications for their preservative, flavoring, pH-regulating, and chelating properties. The market is driven by increasing demand for natural and bio-based acids, growing adoption in the pharmaceutical and personal care industries, and rising awareness of food safety and sustainability. Technological innovations and the development of bio-fermentation processes are further supporting the growth of this market globally.

The Global Organic Acid Market is witnessing strong trends toward bio-based and environmentally friendly production methods, with fermentation-based processes replacing chemical synthesis. Increasing consumer preference for natural ingredients in food, beverages, and personal care products is accelerating adoption. Demand for clean-label, preservative-free, and functional foods is driving citric and lactic acid consumption. Additionally, innovations in pharmaceutical and nutraceutical formulations are creating new applications for organic acids. Geographic expansion into emerging economies, coupled with growing industrial applications, is further stimulating market growth. Sustainability initiatives, renewable feedstocks, and integration of green chemistry principles are also shaping market strategies and product development in this sector.

Segmentation: The Global Organic Acid Market is segmented by Type (Citric Acid, Lactic Acid, Acetic Acid, Malic Acid and Other Organic Acids), Application (Food & Beverages, Pharmaceuticals & Nutraceuticals, Personal Care & Cosmetic, Industrial Applications and Agriculture), Source (Natural/Bio-based and Synthetic/Chemical-based), End-Use Industry (Food & Beverage Industry, Pharmaceutical Industry, Cosmetics & Personal Care Industry, Chemical & Industrial Manufacturing and Agriculture & Animal Feed), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The rising demand for organic acids in the food and beverage industry is a primary driver of market growth.

Organic acids like citric, lactic, and acetic acid are widely used as preservatives, flavor enhancers, pH regulators, and chelating agents. Increasing consumer awareness of food safety, clean-label products, and natural ingredients has accelerated adoption in beverages, dairy, bakery, and processed foods. For instance, in May 2024, Innovad Group’s acquisition of Brazilian feed additive supplier Oligo Basics expands its organic acid-based product portfolio in the animal nutrition sector. This strategic move strengthens Innovad’s presence in Latin America, driving innovation and growth in organic acid applications within animal feed, and contributing to the overall expansion and diversification of the global organic acid market.

Rapid urbanization, changing dietary patterns, and rising disposable incomes are fueling consumption in emerging economies. Additionally, the trend toward functional and fortified foods, which often incorporate organic acids for stability and taste, is further supporting global market expansion.

The expanding use of organic acids in pharmaceuticals and personal care products is a key growth driver.

Organic acids serve as excipients, pH adjusters, preservatives, and active ingredients in medicines, supplements, skincare, and cosmetics. Rising demand for safer, bio-based, and natural ingredients in these industries has increased the adoption of citric, lactic, and malic acids. Additionally, growth in the global healthcare sector, aging populations, and higher consumer spending on personal care products are driving market expansion. Pharmaceutical formulations require consistent quality and purity, which organic acids provide, further reinforcing their importance. This trend continues to boost production and innovation in the market.

Market Restraints:

Fluctuating raw material prices pose a significant restraint on the Global Organic Acid Market. Organic acids are often produced from agricultural feedstocks such as corn, sugarcane, and molasses, whose costs are affected by weather conditions, crop yields, and global commodity prices. Price volatility increases production costs and affects profitability, particularly for smaller manufacturers. Additionally, dependence on imports in certain regions exposes producers to supply chain disruptions and currency fluctuations. These challenges may limit investment in capacity expansion and R&D. As a result, inconsistent raw material availability and cost instability can hinder market growth despite rising demand across food, beverage, pharmaceutical, and industrial sectors.

The Global Organic Acid Market has notable socioeconomic impacts by supporting employment, industrial growth, and public health. Production and distribution activities create jobs in manufacturing, logistics, and research sectors worldwide. Organic acids enhance food safety and shelf life, contributing to improved nutrition and reduced waste. In pharmaceuticals and personal care, organic acids support the development of safer, effective products, improving healthcare outcomes. Emerging economies benefit from increased local production and technological transfer, strengthening industrial infrastructure. Additionally, bio-based organic acids reduce reliance on petrochemicals, promoting environmental sustainability. Thus, the market contributes to economic development, innovation, and enhanced quality of life globally.

Segmental Analysis:

The citric acid segment is expected to witness the highest growth over the forecast period due to its widespread applications across food and beverages, pharmaceuticals, personal care, and industrial products. Citric acid is widely used as a flavoring agent, preservative, and pH regulator, making it essential for processed foods, beverages, dairy products, and confectionery. Increasing consumer preference for natural and clean-label ingredients is driving demand for citric acid derived from fermentation processes. Additionally, its role in effervescent tablets, nutritional supplements, and cosmetic formulations further contributes to adoption. Rising industrial applications, coupled with expanding global food processing and pharmaceutical sectors, are expected to sustain strong growth for citric acid.

The food and beverages segment is expected to witness the highest growth over the forecast period, driven by rising consumer demand for processed, packaged, and functional foods. Organic acids, including citric, lactic, and acetic acid, are extensively used as preservatives, flavor enhancers, acidulants, and pH regulators in beverages, dairy products, bakery items, and confectionery. Growing awareness of food safety, shelf-life extension, and clean-label requirements is further boosting adoption. Additionally, the increasing consumption of ready-to-drink beverages, energy drinks, and functional foods in developed and emerging economies is stimulating market growth. Expansion of modern retail channels and e-commerce platforms is also contributing to higher sales in this segment.

The natural or bio-based segment is expected to witness the highest growth over the forecast period as manufacturers and consumers increasingly favor sustainable and environmentally friendly solutions. Bio-based organic acids, produced via fermentation from renewable feedstocks like corn, sugarcane, and molasses, offer advantages such as lower environmental impact, non-toxicity, and clean-label compliance. Rising consumer preference for natural ingredients in food, beverages, and personal care products is accelerating adoption. Additionally, government regulations promoting green chemistry and sustainable industrial practices are encouraging manufacturers to shift from synthetic to bio-based production. Expansion of the pharmaceutical and cosmetic industries also drives demand, making bio-based organic acids a key growth segment globally.

The food and beverage industry segment is expected to witness the highest growth over the forecast period due to the increasing consumption of processed, packaged, and functional foods worldwide. Organic acids, including citric, lactic, and malic acids, are widely used as preservatives, acidulants, flavor enhancers, and pH stabilizers in beverages, dairy products, bakery items, and confectionery. Rising consumer awareness regarding food safety, natural ingredients, and clean-label products has further accelerated adoption. Expansion of retail channels, including supermarkets, hypermarkets, and e-commerce platforms, is also driving demand. Additionally, the growing popularity of ready-to-eat meals, functional beverages, and fortified foods continues to contribute to the rapid growth of organic acid use in the food and beverage industry.

The Asia-Pacific region is expected to witness the highest growth over the forecast period, driven by rapid industrialization, increasing urbanization, and rising disposable incomes.

Countries such as China, India, Japan, and Southeast Asian nations are witnessing strong demand for organic acids in food and beverages, pharmaceuticals, personal care, and industrial applications. For instance, in October 2024, Evonik’s restructuring of its keto and pharma amino acid business to focus on core growth areas and optimize production sites in France and China reflects a strategic move to enhance operational efficiency. This initiative is expected to strengthen Evonik’s market position and improve its organic acid product portfolio, thereby positively influencing competitive dynamics and growth prospects in the global organic acid market.

Similarly, In November 2024, BASF’s partnership with Acies Bio to enhance sustainable fatty alcohol production using fermentation technology and renewable methanol reinforces BASF’s leadership in bio-based chemicals. This collaboration drives innovation and sustainability in organic acid production, bolstering the global organic acid market’s shift towards greener processes and expanding the adoption of renewable, bio-derived ingredients.

Expanding food processing and pharmaceutical sectors, coupled with growing consumer awareness of natural and clean-label products, are further supporting market growth. Additionally, government initiatives promoting sustainable and bio-based products, along with investment in production facilities and R&D, are expected to drive rapid adoption of organic acids across the Asia-Pacific region.

| Report Matrics | Details |

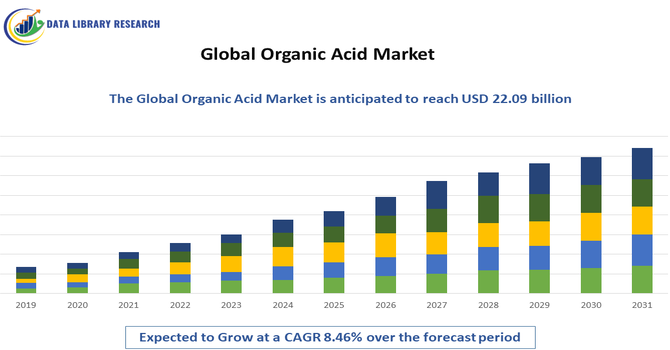

| Market Size Value | USD 22.09 billion |

| Growth Rate | CAGR of 8.46% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The Global Organic Acid Market is highly competitive, comprising multinational chemical manufacturers, specialty chemical companies, and regional producers. Market players compete on product quality, pricing, innovation, and sustainable manufacturing practices. Companies are investing in bio-fermentation technologies, eco-friendly production, and expanding capacities to meet rising global demand. Strategic partnerships, mergers, and acquisitions are common to enhance product portfolios and geographic reach. Established players leverage brand recognition, technological expertise, and distribution networks to maintain market leadership. Meanwhile, smaller regional producers focus on niche applications and cost-effective solutions. Innovation in bio-based acids, cleaner production methods, and regulatory compliance continues to define competitive dynamics in this market.

The major players are:

Recent Development

Q1. What is the main growth-driving factors for this market?

Market growth is primarily driven by the rising demand for natural preservatives and clean-label ingredients in the food and beverage industry. Increasing adoption of feed acidifiers in antibiotic-free livestock production and the shift toward bio-based intermediates for bioplastics (like PLA) are major catalysts. Technological advancements in microbial fermentation further enhance production efficiency.

Q2. What are the main restraining factors for this market?

The market is hindered by volatile raw material prices, specifically for agricultural feedstocks like corn and sugar. High energy costs for downstream processing and stringent environmental regulations regarding synthetic acid production also pose challenges. Additionally, price compression in certain segments due to global overcapacity can limit profit margins for manufacturers.

Q3. Which segment is expected to witness high growth?

The Natural/Bio-based segment is expected to witness the highest growth over the forecast period due to increasing demand for sustainable and eco-friendly products. Bio-based organic acids, produced from renewable resources, appeal to environmentally conscious consumers and industries, driving adoption in food, pharmaceuticals, and personal care, while supporting green manufacturing trends globally.

Q4. Who are the top major players for this market?

The competitive landscape is led by global agricultural and chemical giants, including Cargill, Inc., Archer Daniels Midland (ADM), and BASF SE. Other influential players driving innovation in fermentation and bio-based solutions include Corbion N.V., Dow Chemical Company, Celanese Corporation, Eastman Chemical, and Henan Jindan Lactic Acid Technology.

Q5. Which country is the largest player?

China is the largest market player, serving as the world’s primary production and export hub for organic acids like citric and lactic acid. Its dominance is supported by massive manufacturing scale and a robust bio-manufacturing ecosystem. The United States follows closely, remaining a top player due to high demand for high-purity pharmaceutical-grade acids.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model