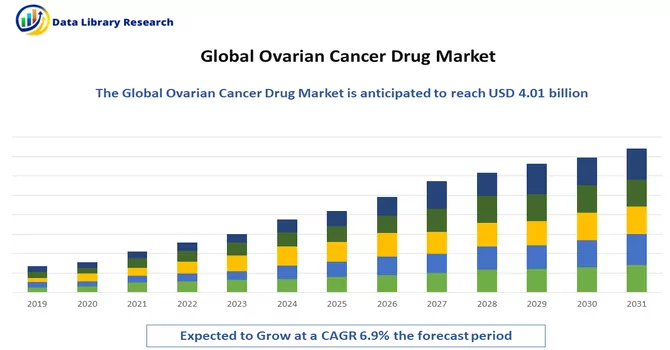

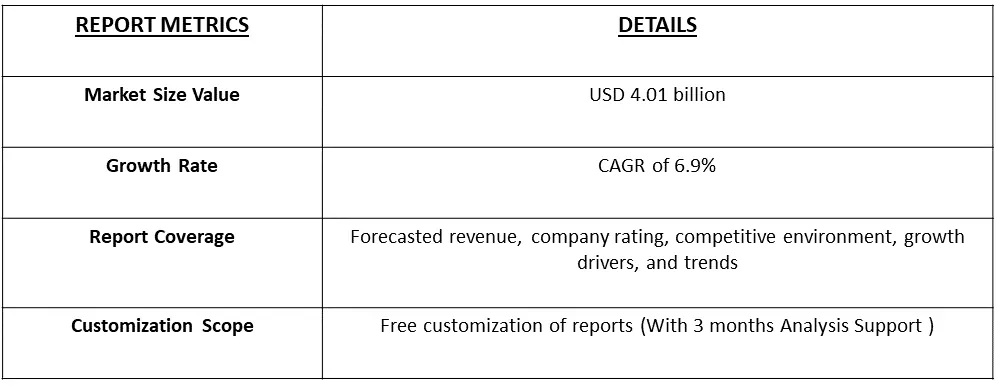

The global ovarian cancer drugs market size was estimated at USD 4.01 billion in 2023 and is anticipated to grow at a compound annual growth rate (CAGR) of 6.9% from 2024 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

Ovarian cancer drugs refer to pharmaceutical agents designed for the prevention, treatment, or management of ovarian cancer. Ovarian cancer is a type of cancer that originates in the ovaries, which are part of the female reproductive system. These drugs are developed to target and inhibit the growth of cancer cells, alleviate symptoms, and improve the overall prognosis and quality of life for individuals diagnosed with ovarian cancer. The drugs may include chemotherapy agents, targeted therapies, immunotherapies, and hormonal therapies, among others. The selection of specific drugs depends on factors such as the type and stage of ovarian cancer, as well as individual patient characteristics. Ovarian cancer drugs play a crucial role in various treatment modalities, either as standalone therapies or in combination regimens, and ongoing research aims to discover new and more effective treatments for this challenging disease.

The increasing prevalence of ovarian cancer, attributed to the rise in unhealthy lifestyles, stands out as a primary driver for the ovarian cancer drug market's growth. Unhealthy lifestyle factors, such as poor dietary habits and lack of physical activity, contribute to the escalating incidence of ovarian cancer. Moreover, the market is anticipated to benefit from the growing adoption of innovative drugs and a robust product pipeline. Ongoing advancements in drug development and therapeutic approaches are expected to positively impact the ovarian cancer treatment landscape, offering new and improved options for patients.

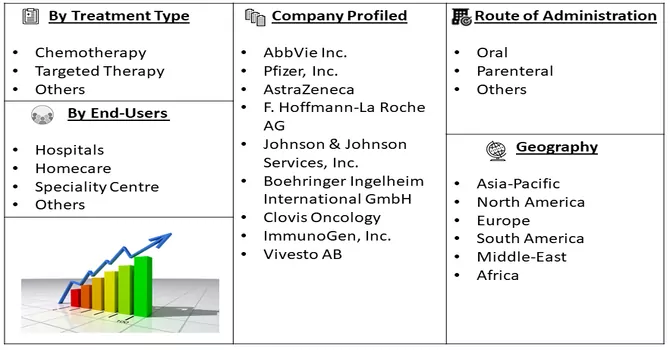

Market Segmentation: The Ovarian Cancer Drug Market is Segmented by Treatment Type (Chemotherapy, Targeted Therapy, and Others), Route of Administration (Oral, Parenteral, Others), End-Users (Hospitals, Homecare, Speciality Centres, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market values are provided in terms of (USD million) for all the above segments.

For Detailed Market Segmentation - Download Free Sample PDF

Emerging trends in the ovarian cancer drug market include a heightened focus on precision medicine and targeted therapies, reflecting a shift towards more personalized treatment approaches. Advancements in genomics and molecular diagnostics have enabled the identification of specific biomarkers associated with ovarian cancer, facilitating the development of drugs tailored to individual patient profiles. Immunotherapy is gaining prominence as a promising avenue, with ongoing research exploring novel immune checkpoint inhibitors and other immunotherapeutic strategies for ovarian cancer treatment. Additionally, collaborative efforts between pharmaceutical companies and research institutions are fostering the exploration of combination therapies to enhance treatment efficacy. The market is witnessing a trend towards the integration of innovative technologies and data-driven approaches to optimize drug discovery and development processes. Overall, these trends underscore a dynamic and evolving landscape aimed at improving treatment outcomes for ovarian cancer patients.

Market Drivers:

Increase in Elderly Population

The anticipated rise in the geriatric population is poised to contribute significantly to the global hematuria treatment market during the forecast period. As per the World Health Organization (WHO), the global elderly population is projected to surge to approximately 2 billion by 2050, a substantial increase from 617 million in 2015. The heightened prevalence of ovarian cancer is also linked to this ageing demographic. This demographic shift is expected to fuel market growth, highlighting the increasing importance of effective hematuria treatment strategies to address the healthcare needs of an ageing population.

Technological Advancement

Market participants employ various key strategies such as securing product approvals, launching new products, and establishing strategic partnerships to sustain and expand their market presence. A noteworthy example is the announcement made by ImmunoGen Inc. in November 2022, indicating that the Food and Drug Administration (FDA) granted accelerated approval for ELAHERE in treating platinum-resistant ovarian cancer. Additionally, in March 2020, Vivesto AB and Elevar Therapeutics Inc. entered into a global strategic partnership aimed at commercializing Vivesto AB’s ovarian cancer drug Apealea. These strategic moves underscore the dynamic landscape of the ovarian cancer drug market, reflecting the importance of regulatory milestones and collaborative efforts to drive advancements and provide effective treatments for patients.

Market Restraints:

Lack of Skilled Professionals and High Cost

The potential hindrance to the growth of the global ovarian cancer market over the forecast period may stem from a shortage of trained professionals who lack knowledge about the treatment methods for this disease. Additionally, the substantial costs associated with the treatment methods are likely to impede market growth.

The ovarian cancer drug market experienced a notable impact from the COVID-19 pandemic. The outbreak led to disruptions in healthcare systems, affecting both patient access to treatments and the development of new drugs. During the initial phases of the pandemic, there were challenges in the supply chain, and healthcare resources were redirected to address the urgent needs arising from the virus. Additionally, clinical trials faced delays or interruptions, impacting the progress of potential ovarian cancer drugs. The focus on managing the pandemic shifted priorities, and patients may have encountered obstacles in seeking timely cancer care. As the healthcare sector adapted to new norms and the situation improved, efforts were made to resume regular oncology services. Despite the challenges, ongoing research and development in the field aim to address the needs of ovarian cancer patients, reflecting a resilient outlook for the market post-pandemic.

Segmental Analysis:

Chemotherapy Segment is Expected to Witness Significant Growth over the Forecast Period

Chemotherapy is a widely utilized treatment modality in the field of oncology, encompassing the use of potent drugs to combat and eradicate cancer cells. This therapeutic approach involves administering medications, commonly referred to as cancer drugs, to target and disrupt the rapid growth of cancerous cells. The drugs used in chemotherapy may vary, and their selection depends on factors such as the type and stage of cancer, the patient's overall health, and the treatment goals. These drugs work by interfering with the cell division process, preventing the cancer cells from proliferating. While chemotherapy is a cornerstone in cancer treatment, its application may be accompanied by side effects due to the impact on healthy cells. Despite potential challenges, chemotherapy plays a pivotal role in managing various cancers, contributing significantly to the comprehensive approach to cancer care.

Parenteral Segment is Expected to Witness Significant Growth over the Forecast Period

Parenteral administration refers to the delivery of medications directly into the body through routes other than the digestive system. In the context of cancer treatment, parenteral administration is a common and crucial method for delivering cancer drugs. This approach ensures the direct entry of medications into the bloodstream, facilitating their rapid distribution throughout the body to target cancer cells. Parenteral routes include intravenous (IV) injections, intramuscular (IM) injections, and subcutaneous (SC) injections. IV chemotherapy, in particular, allows for precise dosage control and immediate access to the circulatory system. The utilization of parenteral administration in cancer drug delivery offers several advantages. It allows for the efficient and direct delivery of potent medications, ensuring they reach the systemic circulation quickly. This method is especially valuable when treating cancers that have metastasized or spread to different parts of the body. Additionally, parenteral routes enhance the bioavailability of cancer drugs, maximizing their therapeutic impact. However, it's essential to acknowledge that parenteral administration of cancer drugs may also pose challenges, including the risk of infection, potential adverse reactions, and the need for skilled healthcare professionals for proper administration. Despite these considerations, the strategic use of parenteral routes plays a pivotal role in the effective management of cancer, contributing to comprehensive and targeted treatment strategies.

Hospitals Segment is Expected to Witness Significant Growth over the Forecast Period

Hospitals play a pivotal role in the comprehensive care and treatment of patients diagnosed with ovarian cancer, and they serve as central hubs for the administration of ovarian cancer drugs. Ovarian cancer, being a complex and potentially aggressive disease, often requires a multi-modal approach, including surgery, chemotherapy, and other therapeutic interventions. In the hospital setting, specialized oncology departments and infusion centers are equipped to deliver various ovarian cancer drugs through intravenous (IV) infusions. Chemotherapy, a commonly employed treatment for ovarian cancer, is frequently administered in hospitals. Oncologists and healthcare teams in hospitals closely monitor patients during chemotherapy sessions to manage potential side effects and ensure optimal treatment outcomes. The hospital environment provides a controlled and sterile setting for the administration of potent ovarian cancer drugs, enhancing patient safety and treatment efficacy. Moreover, hospitals serve as hubs for collaborative and multidisciplinary care. Oncologists, surgeons, radiologists, and other healthcare professionals work together to create personalized treatment plans for ovarian cancer patients. This collaborative approach ensures that patients receive a comprehensive and tailored treatment strategy that may include surgery to remove tumors followed by chemotherapy or other targeted therapies. In addition to treatment, hospitals offer supportive services such as counselling, rehabilitation, and palliative care to enhance the overall well-being of ovarian cancer patients. As advancements in ovarian cancer research continue, hospitals remain at the forefront of implementing innovative treatment protocols and clinical trials, contributing to ongoing efforts to improve outcomes for individuals affected by ovarian cancer.

North America Region is Expected to Witness Significant Growth over the Forecast Period

North America emerged as the dominant force in the ovarian cancer drug market, commanding the largest revenue as this region boasts a robust healthcare infrastructure and advanced medical facilities that facilitate the early diagnosis and treatment of ovarian cancer. The heightened awareness among patients has contributed to increased screening and detection rates. Furthermore, North America is a hub for numerous pharmaceutical companies, research institutions, and academic centers dedicated to advancing innovative cancer treatments.

According to the American Cancer Society, ovarian cancer holds the grim distinction of being the fifth leading cause of cancer-related deaths among women and stands as the deadliest among all gynecologic malignancies. In 2023, the U.S. reported 19,710 new cases of ovarian cancer, with 13,270 recorded deaths. The prevalence of ovarian cancer underscores the pressing need for effective treatments and ongoing research initiatives in North America, where the convergence of medical expertise and research capabilities continues to drive advancements in the fight against this formidable disease.

In June 2023, Physicians specializing in gynecologic cancer at USask, in collaboration with pathology experts, are set to conduct comprehensive tumor testing for ovarian cancer patients. This testing will encompass a variety of mutations that are indicative of the potential response to a novel class of drugs. Notably, this approach combines multiple tumor testing methods simultaneously, providing patients with more precise and personalized genomic insights into their tumors than ever before. The enhanced information derived from these tests will empower patients to make more informed decisions about their healthcare, offering more accurate assessments of the potential benefits associated with these drugs. Thus, such factors are expected to witness significant growth over the forecast period in the region.

Get Complete Analysis Of The Report - Download Free Sample PDF

The market is characterized by a multitude of participants, with a significant portion of the market share distributed among them. Key players in the industry employ various business strategies such as obtaining product approvals, introducing new products to the market, and forming strategic partnerships. These strategies are crucial for market participants to sustain their existing market share and foster further growth. Some prominent players in the global ovarian cancer drugs market include:

Recent Development:

1) In Jan 2024, Shorla Oncology's New Drug Application (NDA) for SH-105, intended for the treatment of breast and ovarian cancers, has been accepted by the FDA. The NDA is scheduled for a Prescription Drug User Fee Act action date set on June 29, 2024. Orlaith Ryan, Chief Technical Officer and Co-founder of Shorla Oncology expressed optimism about the innovative drug, highlighting its attributes as a ready-to-administer injectable product with unique characteristics, anticipating swift adoption upon approval.

2) In November 2023, AbbVie Inc. declared its acquisition of ImmunoGen, Inc., including its groundbreaking antibody-drug conjugate (ADC) mirvetuximab soravtansine-gynx (Elahere). This ADC has received FDA approval for the treatment of platinum-resistant ovarian cancer.

Q1. What was the Ovarian Cancer Drug Market size in 2023?

As per Data Library Research the global ovarian cancer drugs market size was estimated at USD 4.01 billion in 2023.

Q2. At what CAGR is the Ovarian Cancer Drug market projected to grow within the forecast period?

Ovarian Cancer Drug Market is anticipated to grow at a compound annual growth rate (CAGR) of 6.9% over the forecast period.

Q3. What are the factors driving the Ovarian Cancer Drug market?

Key factors that are driving the growth include the Increase in Elderly Population and Technological Advancement.

Q4. Who are the key players in Ovarian Cancer Drug market?

Some key players operating in the market include

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model