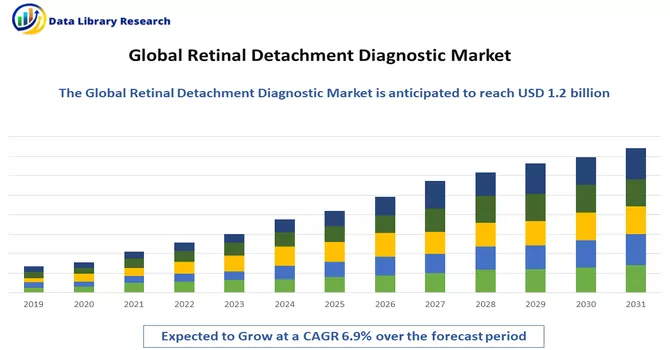

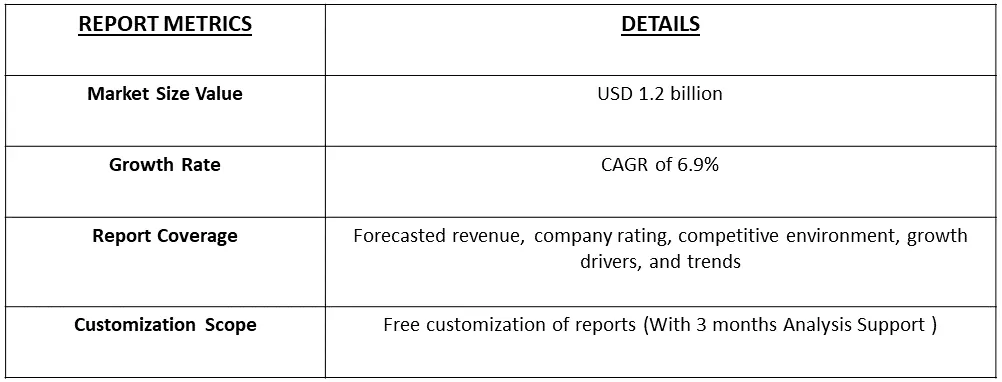

The Retinal Detachment Diagnostic Market size is estimated at USD 1.2 billion in 2023 and is expected to register a CAGR of 6.9% during the forecast period (2024-2031).

Get Complete Analysis Of The Report - Download Free Sample PDF

Retinal detachment diagnostic refers to the process of identifying and confirming the detachment of the retina from its normal position within the eye. Retinal detachment is a serious medical condition where the light-sensitive tissue at the back of the eye (the retina) becomes separated from its underlying supportive layers. Early and accurate diagnosis of retinal detachment is critical as it is considered a medical emergency requiring prompt intervention to prevent vision loss. Diagnostic methods for retinal detachment include a comprehensive eye examination, often involving the use of specialized instruments such as ophthalmoscopes, slit lamps, or imaging techniques like ultrasound or optical coherence tomography (OCT). These diagnostic tools allow healthcare professionals, particularly ophthalmologists, to visualize and assess the condition of the retina, identify any signs of detachment, and determine the appropriate course of treatment. Timely diagnosis and intervention are essential in preserving vision and preventing complications associated with retinal detachment.

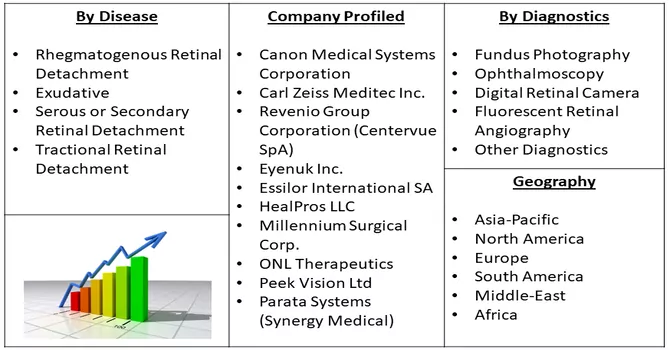

Market Segmentation: The Retinal Detachment Diagnostic Market is segmented by Disease (Rhegmatogenous Retinal Detachment, Exudative, Serous or Secondary Retinal Detachment, Tractional Retinal Detachment), Diagnostics (Fundus Photography, Ophthalmoscopy, Digital Retinal Camera, Fluorescent Retinal Angiography, Other Diagnostics) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The report offers the value in USD million for the above segments.

For Detailed Market Segmentation - Download Free Sample PDF

Market trends for the global retinal detachment diagnostic market include a surge in demand for advanced imaging technologies such as optical coherence tomography (OCT) and ultrasound, which offer high-resolution and detailed visualization of the retina, aiding in accurate diagnosis. The integration of artificial intelligence (AI) in retinal diagnostics is gaining momentum, enhancing the efficiency and accuracy of image analysis, and leading to quicker and more reliable detection of retinal detachment. Increasing awareness about eye health and routine screenings, especially in ageing populations, is driving the demand for retinal examinations and diagnostics. Collaborations and strategic partnerships between healthcare organizations and diagnostic equipment manufacturers are fostering the development of innovative diagnostic solutions. Moreover, the rising prevalence of diabetes, a significant risk factor for retinal detachment, is contributing to the market growth as diabetic retinopathy screenings become more critical. Overall, these trends reflect a dynamic landscape where technological advancements, awareness initiatives, and strategic collaborations converge to shape the trajectory of the retinal detachment diagnostic market.

Market Drivers:

Increase in the Demand of Minimally Invasive Procedures

The global retinal detachment diagnostic market is experiencing a significant upswing in demand, driven notably by the increasing preference for minimally invasive procedures. As healthcare trends evolve, there is a growing shift towards less invasive interventions for various eye conditions, including retinal detachment. Minimally invasive procedures offer advantages such as shorter recovery times, reduced postoperative complications, and improved patient comfort. In the realm of retinal detachment diagnostics, this trend is reflected in the adoption of advanced imaging technologies and surgical techniques. Optical coherence tomography (OCT), for instance, has gained prominence for its non-invasive and high-resolution imaging capabilities, allowing for detailed examinations of the retina without invasive procedures. The demand for such diagnostic tools aligns with the broader healthcare paradigm emphasizing patient-centric approaches and improved outcomes. Additionally, advancements in minimally invasive surgical procedures, such as vitrectomy and retinal laser surgery, contribute to the overall growth of the retinal detachment diagnostic market. These techniques, characterized by smaller incisions and reduced trauma to ocular tissues, are becoming increasingly favored by both healthcare providers and patients. The rise in demand for minimally invasive procedures in retinal detachment diagnostics is further fueled by factors like quicker recovery periods, reduced hospital stays, and a shift towards outpatient care. Patients are increasingly seeking diagnostic and treatment options that offer effective results with minimized invasiveness, driving the market towards innovative solutions. As the global healthcare landscape continues to prioritize minimally invasive approaches, the retinal detachment diagnostic market is poised for expansion, with advanced technologies and techniques playing a pivotal role in meeting the increasing demand for effective yet less invasive solutions in the diagnosis and treatment of retinal detachment.

Technological Developments

The increasing demand for efficient diagnostic devices is driven by rapid technological advancements, although these novel platforms are initially available at high costs. This trend is particularly evident in ophthalmic laser treatment, where the substantial expense of laser devices renders them unaffordable for low- and middle-income groups. The elevated costs are not solely confined to device purchase; rather, installation and service expenses also contribute to the overall financial burden. Ophthalmic lasers, with an average price ranging from USD 20,000 to USD 75,000, exemplify the financial challenges associated with adopting advanced technologies. Moreover, LASIK refractive correction surgery, a common ophthalmic procedure, incurs a significant cost, with treatments priced at over USD 2,077 per eye. These high expenses are anticipated to pose a negative impact on market dynamics throughout the forecast period, limiting accessibility and affordability, particularly for certain socioeconomic groups.

Market Restraints:

High Price of Retinal Surgery Equipment

The global retinal detachment diagnostic market faces a potential impediment to its growth in the form of the high price associated with retinal surgery equipment. While advancements in diagnostic and surgical technologies offer enhanced capabilities, the initial costs of acquiring and implementing these sophisticated devices can be substantial. The elevated expenses extend beyond the purchase of the equipment, encompassing installation and service costs, contributing to the overall financial burden for healthcare facilities. Retinal surgery equipment, including instruments utilized in procedures like vitrectomy and laser surgery, often comes with a significant price tag. This poses a challenge to accessibility and adoption, particularly for healthcare institutions with budgetary constraints. The average cost of retinal surgery equipment, which can range from specialized laser devices to advanced imaging tools, creates barriers for widespread adoption across diverse healthcare settings. Patients, too, may feel the impact of these high costs, as the expenses associated with retinal surgeries, such as vitrectomy for retinal detachment, can contribute to the overall financial burden on healthcare systems and potentially limit access for certain socioeconomic groups. The industry's response to this challenge involves exploring avenues for cost reduction, encouraging innovative pricing models, and fostering collaborations to make advanced retinal surgery equipment more affordable and accessible. As the global healthcare landscape emphasizes value-based care, addressing the high price of retinal surgery equipment becomes crucial for ensuring equitable access to advanced diagnostic and treatment options for retinal detachment. The industry's ability to navigate and mitigate these cost-related challenges will play a pivotal role in shaping the future growth trajectory of the global retinal detachment diagnostic market.

The COVID-19 pandemic brought about uncertainties, altered short-term planning objectives, and heightened focus on immediate cost management and long-term complexity concerns. According to information from the National Library of Medicine, there was a substantial decrease in the rate of retinal detachment diagnoses in emergent ophthalmology consultations during the pandemic. Patients also delayed seeking ophthalmologic examinations, likely influenced by the fear of contracting COVID-19 in hospital environments. Consequently, these factors indicate a significant impact of the COVID-19 pandemic on the retinal detachment diagnostic market. The shift in patient behaviour and hesitancy to seek medical attention due to pandemic-related concerns has implications for the timely diagnosis and management of retinal detachment, emphasizing the broader consequences of the health crisis on specific healthcare domains.

Segmental Analysis:

Rhegmatogenous Retinal Detachment Segment is Expected to Witness Significant Growth Over the Forecast Period

Rhegmatogenous retinal detachment (RRD) stands as a focal point in the global retinal detachment diagnostic market, driving the demand for advanced diagnostic tools and technologies. As a specific type of retinal detachment characterized by breaks or tears in the retina, RRD necessitates prompt and accurate diagnosis to prevent irreversible vision loss. Imaging modalities such as optical coherence tomography, fundus photography, ultrasound, and fluorescein angiography play a pivotal role in identifying retinal breaks and guiding timely interventions. With the increasing prevalence of RRD associated with factors like ageing and myopia, the market is witnessing a surge in demand for precise diagnostic solutions. The competitive landscape is shaped by ongoing technological innovations, research into early detection methods, and collaborations fostering advancements in retinal detachment diagnostics, ultimately contributing to improved patient outcomes.

Fundus Photography Segment is Expected to Witness Significant Growth Over the Forecast Period

Fundus photography plays a pivotal role in the global retinal detachment diagnostic market, serving as a valuable tool for capturing detailed images of the retina. This diagnostic technique involves photographing the back of the eye, specifically the fundus, which includes the retina, optic disc, macula, and blood vessels. These high-resolution images provide healthcare professionals with crucial information for the diagnosis and monitoring of retinal detachment and other eye conditions. In the retinal detachment diagnostic market, fundus photography is often employed to identify signs such as retinal tears, detachments, or other abnormalities. The images captured enable ophthalmologists and retina specialists to assess the extent of retinal damage, plan appropriate interventions, and monitor the progression of the condition over time. The global adoption of fundus photography in retinal detachment diagnostics is driven by several factors. Firstly, the non-invasive nature of the procedure makes it patient-friendly and allows for repeated examinations without causing discomfort. Additionally, the high-resolution images obtained through fundus photography aid in early detection, contributing to timely interventions and improved patient outcomes. Technological advancements in fundus photography, such as the integration of digital imaging systems and the use of wide-angle retinal cameras, further enhance diagnostic capabilities. These innovations provide a comprehensive view of the retina, allowing for more accurate assessments of retinal health. Fundus photography is particularly valuable in the screening and management of diabetic retinopathy, a condition that can lead to retinal detachment if left untreated. As the global prevalence of diabetes increases, the demand for effective diagnostic tools like fundus photography is expected to rise, positively impacting the retinal detachment diagnostic market. Thus, fundus photography serves as an essential component of the global retinal detachment diagnostic market, contributing to early detection, precise monitoring, and improved management of retinal conditions. The continual evolution of imaging technologies will likely further enhance the role of fundus photography in advancing the field of retinal diagnostics.

North America Region is Expected to Witness Significant Growth Over the Forecast Period

North America is poised to be a dominant force in the retinal detachment diagnostic market, primarily driven by extensive research and development activities that consistently lead to new product approvals. The region's substantial market share is attributed to ongoing research initiatives fostering growth through a continuous influx of approved products. The increasing prevalence of target diseases and a growing geriatric population are key factors supporting market growth in North America. The significance of the region is underscored by statistics from the Centers for Disease Control and Prevention (CDC), revealing that approximately 17% of Americans over 40 had cataracts in at least one eye in May 2020, affecting about 20.5 million people. The CDC further predicts that cataracts will impact around 30 million Americans by 2028. Moreover, the CDC estimates that 4.1 million Americans had diabetic retinopathy in 2020, with nearly 900,000 at risk of vision-damaging retinopathy. The escalating incidence of vision disorders, coupled with a rise in cataract cases and an increasing prevalence of diabetic retinopathy, contributes significantly to the growth of this segment. In addition to the high burden of eye-related conditions, the presence of numerous key players in the healthcare sector further propels North America's leadership in the retinal detachment diagnostic market. The collaborative efforts of these key players, coupled with a robust infrastructure for research and development, position the region at the forefront of advancements in retinal diagnostic technologies. Overall, North America emerges as a powerhouse in the retinal detachment diagnostic market, driven by a combination of research excellence, disease prevalence, and the strategic presence of key industry players.

Get Complete Analysis Of The Report - Download Free Sample PDF

The analyzed market exhibits a high degree of fragmentation, primarily attributable to the presence of numerous players operating on both a global and regional scale. The competitive landscape is characterized by a diverse array of companies, each contributing to the overall market dynamics. This fragmentation arises from the existence of specialized solution providers, established industry players, and emerging entrants, all vying for market share. The diversity in market participants is underscored by the adoption of various strategies aimed at expanding the company presence. On a global scale, companies within the studied market are strategically positioning themselves through aggressive expansion initiatives. This often involves entering new geographical regions, targeting untapped markets, and establishing a robust global footprint. The pursuit of global expansion is driven by the recognition of diverse market opportunities and the desire to capitalize on emerging trends and demands across different regions. Simultaneously, at the regional level, companies are tailoring their approaches to align with local market dynamics. Regional players are leveraging their understanding of specific market nuances, regulatory environments, and consumer preferences to gain a competitive edge. This regional focus allows companies to cater to the unique needs of local clientele, fostering stronger market penetration. To navigate the complexities of the fragmented market, companies are implementing a range of strategies. These strategies include investments in research and development to stay at the forefront of technological advancements, mergers and acquisitions to consolidate market share, strategic partnerships for synergies, and innovation to differentiate products and services. The adoption of such multifaceted strategies reflects the competitive nature of the market, with participants continually seeking avenues for growth and sustainability. In essence, the high fragmentation in the studied market not only signifies the diversity of players but also underscores the dynamism and competitiveness that drive ongoing strategic manoeuvres. As companies explore various avenues for expansion, the market continues to evolve, presenting both challenges and opportunities for industry stakeholders. Some of the key market players working in this segment are:

Recent Development:

1) In April 2022, Carl Zeiss Meditec revealed its acquisition of two surgical instrument manufacturers, Kogent Surgical LLC and Katalyst Surgical LLC. This strategic move is aimed at fortifying Carl Zeiss Meditec's position as a comprehensive solution provider in the medical technology sector. By integrating the expertise and product portfolios of Kogent Surgical and Katalyst Surgical, Carl Zeiss Meditec aims to enhance its capabilities in delivering innovative surgical solutions.

2) In January 2022, Alcon, a leading eye care company, completed the acquisition of Ivantis, a company known for developing and manufacturing the Hydrus Microstent. The Hydrus Microstent is a groundbreaking minimally-invasive glaucoma surgery (MIGS) device designed to address glaucoma, a prevalent eye condition. Alcon's acquisition of Ivantis aligns with its commitment to advancing eye health solutions, and this strategic move strengthens Alcon's position in the rapidly evolving field of minimally invasive glaucoma surgery. The acquisition underscores the industry's focus on innovation and the pursuit of cutting-edge technologies to address critical healthcare challenges.

Q1. What was the Retinal Detachment Diagnostic Market size in 2023?

As per Data Library Research the Retinal Detachment Diagnostic Market size is estimated at USD 1.2 billion in 2023

Q2. At what CAGR is the market projected to grow within the forecast period?

Retinal Detachment Diagnostic Market is expected to register a CAGR of 6.9% during the forecast period.

Q3. What are the factors on which the Retinal Detachment Diagnostic market research is based on?

By Disease, By Diagnostics and Geography are the factors on which the Retinal Detachment Diagnostic market research is based.

Q4. Which region has the largest share of the Retinal Detachment Diagnostic market? What are the largest region's market size and growth rate?

North America has the largest share of the market. For detailed insights on the largest region's market size and growth rate request a sample here.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model