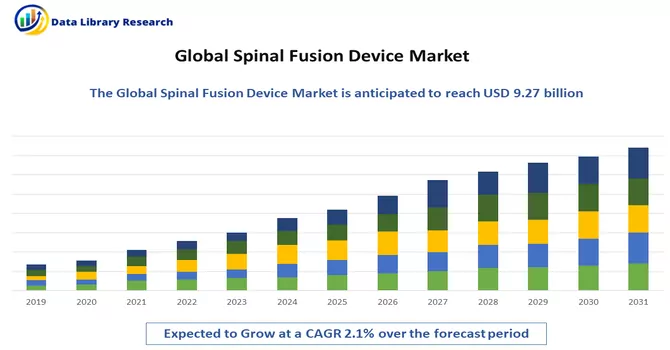

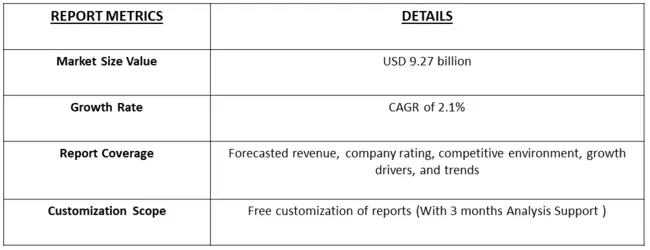

The Spinal Fusion market size was valued at USD 9.27 billion in 2024 and is forecast to grow at a CAGR of approximately 2.1% during 2024 and 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The spinal fusion device market encompasses a range of medical devices used in spinal fusion procedures aimed at stabilizing and treating spinal conditions such as degenerative disc disease, spinal stenosis, and spinal fractures. These devices include spinal fusion implants, instrumentation, bone grafts, and biologics. The market is driven by the increasing prevalence of spinal disorders due to factors such as aging populations, sedentary lifestyles, and rising obesity rates.

Additionally, advancements in surgical techniques, minimally invasive procedures, and implant materials contribute to the growth of the spinal fusion device market. Technological innovations such as 3D printing, robotics, and navigation systems are also reshaping the landscape by enhancing surgical precision and patient outcomes. However, market growth may be hindered by challenges such as regulatory complexities, reimbursement issues, and the high cost associated with spinal fusion procedures. Factors such as aging populations, sedentary lifestyles, and rising obesity rates contribute to the growing incidence of conditions like degenerative disc disease, spinal stenosis, and spinal fractures. As these spinal disorders become more prevalent, there is a corresponding rise in the demand for spinal fusion procedures to stabilize the spine and alleviate symptoms. Moreover, advancements in surgical techniques, implant materials, and minimally invasive procedures have improved patient outcomes and expanded the range of patients eligible for spinal fusion surgery. Additionally, the growing adoption of advanced technologies like 3D printing, robotics, and navigation systems further enhance surgical precision and patient outcomes, driving the growth of the spinal fusion device market.

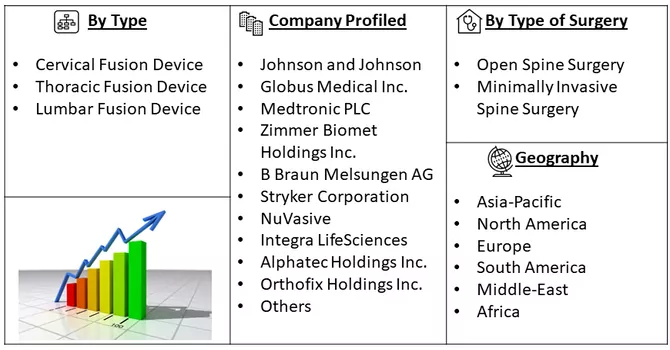

Market Segmentation: The Spinal Fusion Devices Market is Segmented by Type (Cervical Fusion Device, Thoracic Fusion Device, and Lumbar Fusion Device), Type of Surgery (Open Spine Surgery and Minimally Invasive Spine Surgery), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The market provides the value (in USD million) for the above-mentioned segments.

For Detailed Market Segmentation - Download Free Sample PDF

In the spinal fusion device market, several notable trends are shaping the industry landscape. Firstly, there is a growing preference for minimally invasive spinal fusion procedures among patients and surgeons alike. These techniques offer benefits such as reduced tissue trauma, faster recovery times, and shorter hospital stays, driving their adoption. Secondly, there is a rising focus on developing and commercializing innovative spinal fusion devices that offer improved biomechanical stability and better fusion rates. Manufacturers are investing in research and development to introduce novel materials, designs, and technologies to address unmet clinical needs and enhance patient outcomes. Additionally, there is an increasing emphasis on patient-specific implants and personalized treatment approaches, driven by advancements in imaging modalities and computer-aided design tools. Moreover, the market is witnessing a trend towards outpatient spinal fusion procedures, facilitated by advancements in anesthesia, surgical techniques, and post-operative care protocols, enabling patients to return to normal activities sooner and reducing healthcare costs. Lastly, there is a growing trend towards value-based healthcare models, encouraging healthcare providers and payers to seek cost-effective spinal fusion solutions that deliver optimal clinical outcomes and patient satisfaction.

Market Drivers:

Aging Population and Increasing Prevalence of Spinal Disorders:

The aging population worldwide is experiencing a rise in age-related spinal conditions such as degenerative disc disease, spinal stenosis, and spondylolisthesis. As individuals age, the risk of developing these conditions increases, leading to a higher demand for spinal fusion procedures. Additionally, lifestyle factors such as sedentary behavior and obesity contribute to the prevalence of spinal disorders among younger populations. Consequently, the growing patient pool requiring spinal fusion surgery is driving the demand for spinal fusion devices.

Technological Advancements and Innovation in Spinal Fusion Devices:

Continuous innovation in spinal fusion devices, including implants, instrumentation, and surgical techniques, is driving market growth. Manufacturers are introducing advanced materials, such as titanium alloys and bioresorbable polymers, to enhance the durability, biocompatibility, and fusion rates of spinal implants. Furthermore, advancements in surgical navigation systems, robotics, and minimally invasive techniques are improving surgical accuracy, reducing complications, and shortening recovery times, thereby increasing the adoption of spinal fusion procedures. These technological advancements are catering to the evolving needs of surgeons and patients, driving market expansion.

Market Restraints:

One of the primary market restraints for the spinal fusion device market is the high cost associated with spinal fusion procedures and devices. The expenses related to spinal fusion surgery, including hospitalization, surgical fees, and post-operative care, can be substantial, especially for patients without adequate insurance coverage. Additionally, the cost of spinal fusion implants and instrumentation can significantly contribute to the overall healthcare expenditure. This financial burden may deter patients from seeking or undergoing spinal fusion surgery, particularly in regions with limited healthcare resources or where out-of-pocket expenses are high. Moreover, healthcare providers and payers may face challenges in reimbursing the high costs associated with spinal fusion procedures, leading to constraints in market growth. Furthermore, stringent regulatory requirements and approval processes for spinal fusion devices can pose barriers to market entry for manufacturers, limiting competition and innovation in the market. These factors collectively contribute to the market restraint for spinal fusion devices.

The COVID-19 pandemic has had a significant impact on the spinal fusion device market, primarily due to disruptions in elective surgeries and healthcare services. During the peak of the pandemic, many hospitals and healthcare facilities postponed non-urgent procedures, including spinal fusion surgeries, to prioritize resources for treating COVID-19 patients and to minimize the risk of virus transmission among patients and healthcare workers. This temporary halt in elective surgeries led to a decline in the number of spinal fusion procedures performed, resulting in reduced demand for spinal fusion devices. Additionally, supply chain disruptions caused by lockdowns and travel restrictions hindered the manufacturing and distribution of spinal fusion implants and instrumentation, leading to delays in product availability and delivery. Moreover, economic uncertainties and financial strains on healthcare systems and patients further impacted the spinal fusion device market, as healthcare budgets were reallocated towards pandemic response efforts and patients postponed elective procedures due to financial constraints. However, as healthcare systems gradually resume elective surgeries and address backlogs, coupled with the growing prevalence of spinal disorders and aging populations, the demand for spinal fusion devices is expected to rebound in the post-pandemic period. Additionally, innovations in minimally invasive surgical techniques and advancements in implant materials may further drive market growth, as healthcare providers seek to enhance patient outcomes and reduce healthcare costs amidst the ongoing challenges posed by the pandemic.

Segmental Analysis:

Thoracic Fusion Device Segment is Expected to Witness Significant Growth over the Forecast Period

Thoracic fusion devices are medical implants used in spinal fusion surgeries to stabilize and fuse the thoracic spine (the middle segment of the vertebral column) to treat various spinal conditions. Spinal fusion devices are designed to provide structural support to the spine, alleviate pain, and improve spinal stability and alignment. The thoracic spine consists of 12 vertebrae (T1-T12) and is a critical part of the spine that plays a crucial role in supporting the upper body and protecting the spinal cord. Thoracic fusion devices are used to treat conditions such as spinal fractures, deformities (such as scoliosis and kyphosis), tumors, and degenerative disc disease that affect the thoracic spine. Spinal fusion is a surgical procedure that involves joining two or more vertebrae together to eliminate motion between them. This is achieved by placing bone graft material between the affected vertebrae, which eventually fuses the vertebrae together. Thoracic fusion devices are used to provide additional support and stability during the fusion process. There are several types of thoracic fusion devices, including rods, screws, plates, and cages, which are made from biocompatible materials such as titanium or stainless steel. These devices are implanted during surgery to stabilize the spine and facilitate the fusion process. In some cases, bone graft substitutes or biologics (such as growth factors) may also be used to promote bone growth and fusion. Spinal fusion devices have undergone significant advancements in recent years, including the development of minimally invasive techniques and the use of advanced imaging technologies to improve surgical outcomes and reduce complications. These advancements have made spinal fusion surgery a more effective and safer treatment option for patients with thoracic spine disorders. Thus, the segment is expected to witness significant growth over the forecast period.

Minimally Invasive Spine Surgery Segment is Expected to Witness Significant Growth over the Forecast Period

Minimally invasive spine surgery (MISS) is a surgical technique used to treat spinal disorders with less disruption to the surrounding tissues compared to traditional open surgery. This approach involves smaller incisions, specialized instruments, and advanced imaging techniques to access the spine and perform the necessary procedures. One of the key aspects of MISS is the use of specialized spinal fusion devices designed for minimally invasive procedures. These devices are typically smaller in size and are inserted through the small incisions used in MISS. Despite their smaller size, these devices provide the necessary support and stability to facilitate spinal fusion. One common type of spinal fusion device used in minimally invasive surgery is the pedicle screw system. Pedicle screws are inserted into the pedicles of the vertebrae and are used to stabilize the spine during fusion. In minimally invasive procedures, pedicle screws are often placed using specialized instruments and imaging guidance to ensure accuracy and minimize tissue damage. Another type of spinal fusion device used in MISS is the interbody cage. Interbody cages are placed between the vertebrae to restore disc height and promote fusion. In minimally invasive procedures, interbody cages are inserted through small incisions and are often filled with bone graft material to promote fusion. Thus, minimally invasive spine surgery and the use of specialized spinal fusion devices have revolutionized the treatment of spinal disorders, offering patients a safer, more effective, and less invasive alternative to traditional open surgery.

North America Region is Expected to Witness Significant Growth over the Forecast Period

North America is a key region for the spinal fusion devices market, driven by factors such as a high prevalence of spinal disorders, a growing elderly population, and technological advancements in healthcare. The region comprises the United States, Canada, and Mexico, with the United States accounting for the largest share of the market. The prevalence of spinal disorders, such as degenerative disc disease, spinal stenosis, and spinal fractures, is high in North America, particularly among the aging population. This has led to a growing demand for spinal fusion surgeries and devices to treat these conditions. Technological advancements in healthcare, including the development of minimally invasive surgical techniques and advanced implant materials, have also contributed to the growth of the spinal fusion devices market in North America. These advancements have led to improved surgical outcomes, reduced complications, and faster recovery times, driving the adoption of spinal fusion procedures in the region. Additionally, the presence of key market players, research institutions, and healthcare infrastructure in North America has supported the development and commercialization of innovative spinal fusion devices. These factors have further boosted the growth of the market in the region. However, the market in North America also faces challenges such as stringent regulatory requirements, pricing pressures, and competition from alternative treatments. Despite these challenges, the North American spinal fusion devices market is expected to continue its growth trajectory, driven by the increasing prevalence of spinal disorders and the growing adoption of advanced surgical techniques and implant materials.

Get Complete Analysis Of The Report - Download Free Sample PDF

The analyzed market exhibits a high degree of fragmentation, primarily attributable to the presence of numerous players operating on both a global and regional scale. The competitive landscape is characterized by a diverse array of companies, each contributing to the overall market dynamics. This fragmentation arises from the existence of specialized solution providers, established industry players, and emerging entrants, all vying for market share. The diversity in market participants is underscored by the adoption of various strategies aimed at expanding the company presence. On a global scale, companies within the studied market are strategically positioning themselves through aggressive expansion initiatives. This often involves entering new geographical regions, targeting untapped markets, and establishing a robust global footprint. The pursuit of global expansion is driven by the recognition of diverse market opportunities and the desire to capitalize on emerging trends and demands across different regions. Simultaneously, at the regional level, companies are tailoring their approaches to align with local market dynamics. Regional players are leveraging their understanding of specific market nuances, regulatory environments, and consumer preferences to gain a competitive edge. This regional focus allows companies to cater to the unique needs of local clientele, fostering stronger market penetration. To navigate the complexities of the fragmented market, companies are implementing a range of strategies. These strategies include investments in research and development to stay at the forefront of technological advancements, mergers and acquisitions to consolidate market share, strategic partnerships for synergies, and innovation to differentiate products and services. The adoption of such multifaceted strategies reflects the competitive nature of the market, with participants continually seeking avenues for growth and sustainability. In essence, the high fragmentation in the studied market not only signifies the diversity of players but also underscores the dynamism and competitiveness that drive ongoing strategic maneuvers. As companies explore various avenues for expansion, the market continues to evolve, presenting both challenges and opportunities for industry stakeholders.

Some of the key market players working in this domain are:

Recent Development:

1) In June 2022, Camber Spine announced the continuation of its national launch for the SPIRA-P posterior lumbar spacer, marking the next phase in its market introduction. Additionally, the company has successfully commercialized its SPIRA-T oblique posterior lumbar spacer, further expanding its product offerings in the spinal fusion market.

2) In June 2022, the United States Food and Drug Administration (FDA) granted 510K clearance for Aurora Spine's DEXA SOLO-L anterior lumbar interbody fusion device (ALIF). This clearance signifies regulatory approval for the device, allowing Aurora Spine to market and sell the DEXA SOLO-L for use in anterior lumbar interbody fusion procedures. These developments reflect the ongoing innovation and advancement in the spinal fusion device market, with companies like Camber Spine and Aurora Spine introducing new products to address the needs of patients and surgeons. The FDA clearance for the DEXA SOLO-L underscores the device's safety and efficacy, paving the way for its adoption in surgical procedures. Overall, these advancements are expected to contribute to the growth and evolution of the spinal fusion device market, benefiting patients and healthcare providers alike.

Q1. What was the Spinal Fusion Device Market size in 2024?

As per Data Library Research the Spinal Fusion Device size was valued at USD 9.27 billion in 2024.

Q2. At what CAGR is the Spinal Fusion Device market projected to grow within the forecast period?

Spinal Fusion Device market is forecast to grow at a CAGR of approximately 2.1 % over the forecast period.

Q3. Which region has the largest share of the Spinal Fusion Device market? What are the largest region's market size and growth rate?

North America has the largest share of the market. For detailed insights on the largest region's market size and growth rate request a sample here.

Q4. Who are the key players in Spinal Fusion Device market?

Some key players operating in the market include

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model