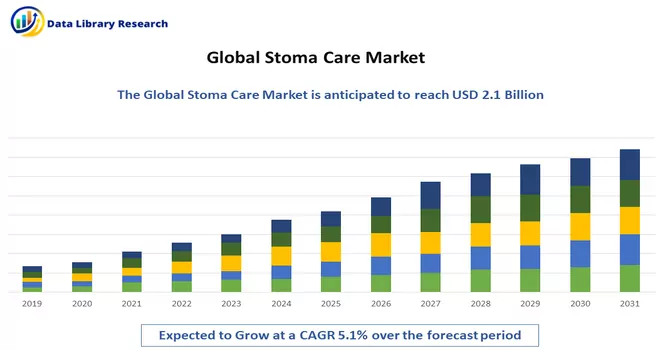

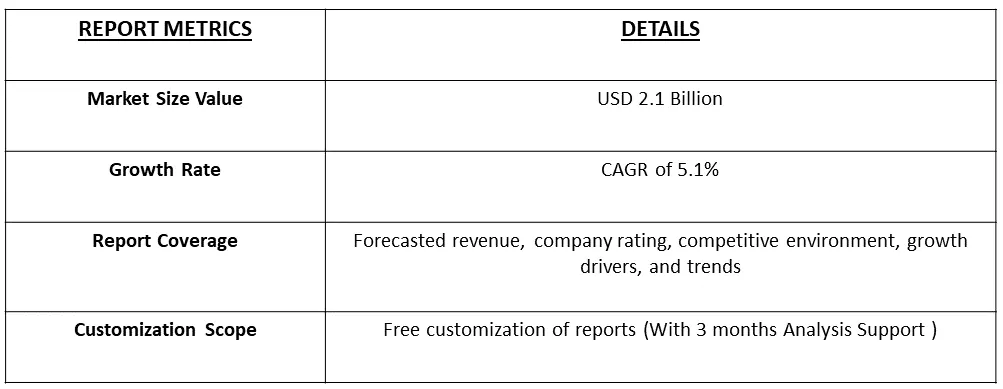

Stoma/ostomy care market is expected to reach USD 2.1 Billion in the year 2023, with sales revenue expected to register 5.1% CAGR over the forecast duration, 2024-2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The Stoma/Ostomy care market plays a pivotal role in providing comprehensive healthcare solutions for individuals with stomas, necessitating specialized care due to surgeries such as colostomy, ileostomy, or urostomy. This market encompasses a range of products and services designed to support stoma patients in managing their unique needs, including ostomy bags, accessories, and skin care products. With a growing prevalence of conditions requiring ostomy procedures, such as colorectal cancer and inflammatory bowel diseases, the demand for effective and patient-centric stoma care solutions is on the rise. Notably, technological advancements and innovations in ostomy products are contributing to improved quality of life for individuals living with stomas. As the global population ages and awareness about stoma care increases, the Stoma/Ostomy care market is expected to witness continuous growth, driven by a commitment to enhancing the well-being and comfort of individuals undergoing ostomy procedures. A primary growth driving factor for the Stoma/Ostomy care market is the increasing prevalence of conditions necessitating ostomy procedures, coupled with a growing aging population. Conditions such as colorectal cancer, inflammatory bowel diseases, and other gastrointestinal disorders that require ostomy surgeries are becoming more prevalent globally. As life expectancy rises, particularly in developed regions, the aging population contributes significantly to the demand for stoma care products and services. Moreover, advancements in medical technology and innovations in ostomy care products, including more discreet and user-friendly pouching systems, are enhancing the quality of life for individuals with stomas, further fueling market growth. The evolving landscape of healthcare, with an emphasis on patient-centric care and improved access to stoma care education, also contributes to the market's expansion. Overall, the intersection of demographic trends, medical advancements, and a commitment to enhancing patient well-being positions the Stoma/Ostomy care market for sustained growth.

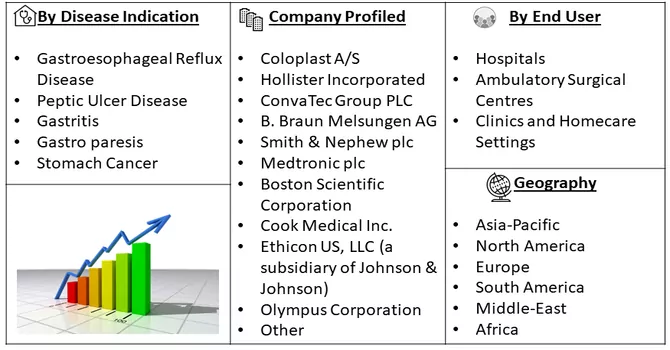

Market Segmentation: The stoma care market can be segmented by Disease Indication: (Gastroesophageal Reflux Disease, Peptic Ulcer Disease, Gastritis, Gastro paresis and Stomach Cancer End User: (Hospitals, Ambulatory Surgical Centres, Clinics and Homecare Settings) and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The market provides the value (in USD million) for the above-mentioned segments.

For Detailed Market Segmentation - Download Free Sample PDF

The Stoma/Ostomy care market is characterized by several notable trends that are shaping the landscape of care for individuals with stomas. A key trend is the increasing focus on patient-centered solutions, with a growing emphasis on comfort, discretion, and lifestyle compatibility in ostomy products. Technological innovations, such as smart ostomy devices and remote monitoring, are gaining traction, providing patients and healthcare providers with real-time data and improving overall management. Additionally, there is a trend towards sustainable and eco-friendly ostomy products, aligning with broader environmental consciousness. The integration of telehealth and digital platforms for ostomy support and education is fostering greater accessibility to resources for patients. As awareness about stoma care grows, the market is witnessing a shift towards comprehensive, holistic solutions that address the diverse needs of individuals living with stomas, reflecting an evolving and patient-centric approach in the Stoma/Ostomy care market.

Market Drivers:

The rising incidence of conditions such as colorectal cancer

The rising incidence of conditions such as colorectal cancer stands as a pivotal driver for the Stoma/Ostomy care market. Colorectal cancer, along with other gastrointestinal disorders, often necessitates ostomy procedures, creating an increased demand for specialized care and products designed to support individuals with stomas. As these conditions become more prevalent globally, particularly with factors like aging populations and changing lifestyles, the market for Stoma/Ostomy care experiences a corresponding surge. The imperative need for effective and tailored solutions to manage ostomies underscores the growing significance of the market, positioning it to address the evolving healthcare needs associated with colorectal cancer and other gastrointestinal disorders requiring ostomy interventions.

Continuous advancements in ostomy care products

Continuous advancements in ostomy care products represent a significant driving force in the Stoma/Ostomy care market. The ongoing evolution of ostomy care is characterized by innovative technologies and product enhancements that prioritize comfort, convenience, and improved quality of life for individuals with stomas. Technological innovations have led to the development of discreet and user-friendly pouching systems, advanced skin barrier technologies, and odor-control solutions. These advancements not only address practical challenges associated with stoma care but also contribute to enhanced patient satisfaction. The continuous refinement of ostomy care products reflects a commitment to improving the overall experience for individuals undergoing ostomy procedures, fostering market growth as consumers increasingly seek sophisticated and effective solutions to meet their diverse needs.

Market Restraints:

The Stoma/Ostomy care market encounters several market restraints that impact its trajectory. One significant challenge is the stigma associated with ostomies, leading to social and psychological barriers that may deter individuals from seeking or adhering to proper stoma care. Limited awareness and education about ostomy care among patients and healthcare professionals contribute to these challenges. Additionally, economic constraints and high out-of-pocket costs for ostomy products can hinder accessibility, particularly in lower-income regions. Regulatory hurdles and reimbursement issues further complicate market dynamics, influencing the availability and affordability of advanced ostomy care products. Furthermore, disparities in healthcare infrastructure and support services across different geographical areas pose obstacles to consistent and optimal stoma care. Addressing these multifaceted restraints requires collaborative efforts from healthcare stakeholders, industry participants, and advocacy groups to reduce stigma, enhance education, and improve accessibility to comprehensive Stoma/Ostomy care.

The Stoma/Ostomy care market has felt the impact of the COVID-19 pandemic, introducing a set of challenges that have influenced both patient care and market dynamics. The disruption in healthcare services, delayed elective surgeries, and restrictions on in-person consultations have affected the timely initiation of ostomy care for patients. Supply chain disruptions and increased demand for medical resources during the pandemic have led to shortages of ostomy products, causing concerns for patients in need of continuous care. Moreover, the psychological impact of the pandemic, coupled with social isolation, has heightened the challenges for individuals living with ostomies. However, the pandemic has accelerated the adoption of telehealth and virtual support services for ostomy care, providing alternative means of assistance. As the world strives towards recovery, the Stoma/Ostomy care market is poised to adapt to the evolving healthcare landscape, emphasizing resilience, digital innovation, and patient-centric solutions in the post-COVID-19 era.

Segmental Analysis:

Peptic Ulcer Disease is Expected to Witness Significant Growth Over the Forecast Period

Peptic ulcer disease (PUD) is a prevalent gastrointestinal disorder characterized by painful sores or ulcers in the lining of the stomach or the upper part of the small intestine. The management and treatment of PUD represent a significant segment of the stomach care market. This includes various therapeutic interventions such as medications (antacids, proton pump inhibitors, H2 receptor antagonists), dietary modifications, and sometimes surgical procedures in severe cases. The demand for stomach care products and services related to peptic ulcer disease is driven by factors such as the increasing prevalence of PUD, growing awareness about gastrointestinal health, and advancements in medical technology for diagnosis and treatment. Additionally, lifestyle changes, stress, and dietary habits also influence the incidence and management of peptic ulcers, thereby impacting the market dynamics of stomach care products and services.

Ambulatory Surgical Centres to Witness Significant Growth Over the Forecast Period

Ambulatory surgical centers (ASCs) play a crucial role in providing efficient and cost-effective healthcare services, including various procedures related to stomach care. These centers offer outpatient surgical procedures, including endoscopic examinations, biopsies, and minor surgical interventions for stomach-related conditions such as peptic ulcers, gastritis, and gastrointestinal cancers. The inclusion of stomach care services in ASCs contributes significantly to the overall market for stomach care, as it provides patients with convenient access to specialized care outside traditional hospital settings. The growth of ASCs in the healthcare landscape, driven by factors such as patient preference for outpatient procedures, cost-effectiveness, and technological advancements, further influences the dynamics of the stomach care market. Additionally, the emphasis on value-based care models and the increasing adoption of minimally invasive techniques in stomach care procedures are expected to propel the demand for stomach care services offered in ambulatory surgical centers.

North America Region is Expected to Witness Significant Growth Over the Forecast Period

The North American stomacare market encompasses a broad spectrum of healthcare services, devices, and pharmaceuticals aimed at addressing various stomach-related conditions and diseases. This region is characterized by a well-established healthcare infrastructure, advanced medical technologies, and a high prevalence of stomach-related ailments such as peptic ulcers, gastroesophageal reflux disease (GERD), and gastric cancers. With a growing aging population and increasing awareness about digestive health, the demand for stomacare solutions in North America is on the rise. Moreover, the presence of key market players, extensive research and development activities, and favorable reimbursement policies contribute to the growth of the stomacare market in this region. Additionally, initiatives focused on preventive care, early detection, and advanced treatment options further drive the expansion of the North American stomacare market.

Get Complete Analysis Of The Report - Download Free Sample PDF

The analyzed market exhibits a high degree of fragmentation, primarily attributable to the presence of numerous players operating on both a global and regional scale. The competitive landscape is characterized by a diverse array of companies, each contributing to the overall market dynamics. This fragmentation arises from the existence of specialized solution providers, established industry players, and emerging entrants, all vying for market share. The diversity in market participants is underscored by the adoption of various strategies aimed at expanding the company presence. On a global scale, companies within the studied market are strategically positioning themselves through aggressive expansion initiatives. This often involves entering new geographical regions, targeting untapped markets, and establishing a robust global footprint. The pursuit of global expansion is driven by the recognition of diverse market opportunities and the desire to capitalize on emerging trends and demands across different regions. Simultaneously, at the regional level, companies are tailoring their approaches to align with local market dynamics. Regional players are leveraging their understanding of specific market nuances, regulatory environments, and consumer preferences to gain a competitive edge. This regional focus allows companies to cater to the unique needs of local clientele, fostering stronger market penetration. To navigate the complexities of the fragmented market, companies are implementing a range of strategies. These strategies include investments in research and development to stay at the forefront of technological advancements, mergers and acquisitions to consolidate market share, strategic partnerships for synergies, and innovation to differentiate products and services. The adoption of such multifaceted strategies reflects the competitive nature of the market, with participants continually seeking avenues for growth and sustainability. In essence, the high fragmentation in the studied market not only signifies the diversity of players but also underscores the dynamism and competitiveness that drive ongoing strategic maneuvers. As companies explore various avenues for expansion, the market continues to evolve, presenting both challenges and opportunities for industry stakeholders.

Some of the key market players are:

Recent Development:

1) In June 2023, Swift Medical Inc. and Corstrata announced a strategic collaboration to enhance and expand access to high-quality wound care. Through this partnership, customers will benefit from Swift Medical Inc.'s AI-powered wound treatment platform, which offers comprehensive documentation, wound imaging, collaboration, and decision-making tools. Additionally, customers will have access to Corstrata's team of registered WOC (Wound, Ostomy, Continence) nurses, further enhancing the quality of care available.

2) In February 2022, HR Pharmaceuticals, Inc. introduced its latest product line, Vitus Ostomy Care. This comprehensive range of ostomy accessories is specifically crafted to enhance stoma and skin protection, while also ensuring a secure seal.

Q1. What was the Stoma Care Market size in 2023?

As per Data Library Research the Stoma/ostomy care market is expected to reach USD 2.1 Billion in the year 2023.

Q2. At what CAGR is the Stoma Care market projected to grow within the forecast period?

Stoma Care Market expected to register 5.1% CAGR over the forecast Period.

Q3. Which Region is expected to hold the highest Stoma Care Market share?

North America region is expected to hold the highest Stoma Care Market share.

Q4. Who are the key players in Stoma Care Market ?

Some key players operating in the market include

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model