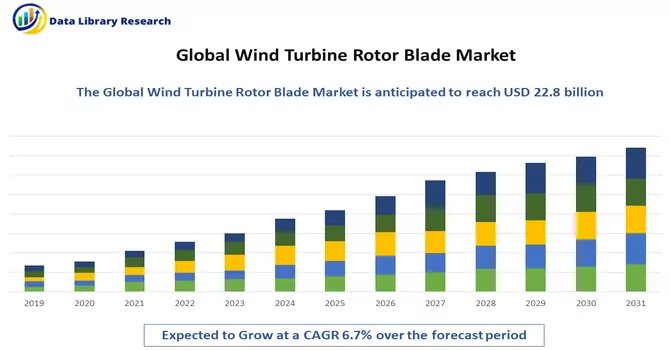

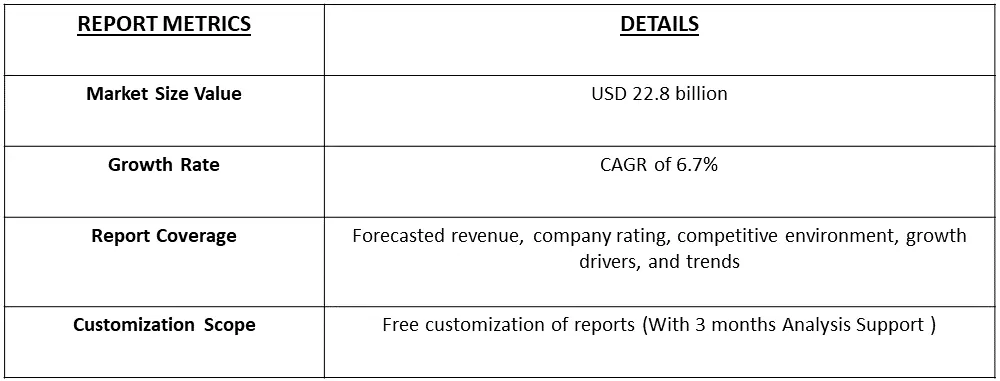

The Global Wind Turbine Rotor Blade Market size was estimated at about USD 22.8 billion in the current year, 2023 and is projected to register at a CAGR of about 6.7% during the forecast period, 2024-2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

A wind turbine rotor blade is a crucial component of a wind energy system designed to capture and convert the kinetic energy of the wind into mechanical energy, ultimately generating electricity. Typically constructed from lightweight and durable materials such as fiberglass or carbon fiber composites, these blades are aerodynamically shaped to efficiently harness wind energy. Their length and design impact the turbine's overall performance, with longer blades capturing more wind and generating higher power outputs. The rotation of the blades drives the turbine's generator, facilitating the conversion of wind energy into electrical power for use in homes, businesses, or the broader electricity grid.

The wind turbine rotor blade market experiences robust growth driven by a convergence of factors shaping the renewable energy sector. The increasing global commitment to sustainability, driven by climate change concerns, propels the demand for wind energy, positioning rotor blades as critical components for harnessing wind power. Supportive government policies, ongoing technological advancements enhancing blade efficiency, and a decreasing cost trend in wind energy contribute to a favorable market environment. The market is buoyed by the continual global expansion of wind power capacity, heightened environmental consciousness, and corporate initiatives towards sustainability. Moreover, the surge in global energy consumption and the imperative to reduce reliance on traditional fossil fuels further amplify the market's growth trajectory, establishing wind turbine rotor blades as integral in meeting the escalating demand for clean and efficient energy solutions in the business landscape.

The wind turbine rotor blade market is witnessing several key trends that are shaping its trajectory. One prominent trend is the increasing demand for larger and technologically advanced blades, driven by the pursuit of higher energy yields and enhanced turbine efficiency. Innovations in materials, such as carbon fiber composites, are gaining prominence, enabling lighter yet more durable blades. Additionally, a shift towards modular and segmented blade designs is emerging, facilitating easier transportation and assembly, particularly in regions with logistical challenges. Sustainability considerations are influencing a growing preference for recyclable and eco-friendly materials in blade manufacturing. Furthermore, digitalization and data analytics are being increasingly integrated into blade monitoring and maintenance practices, contributing to improved performance and lifespan. As the industry continues to evolve, these trends underscore a focus on efficiency, sustainability, and technological innovation in the wind turbine rotor blade market.

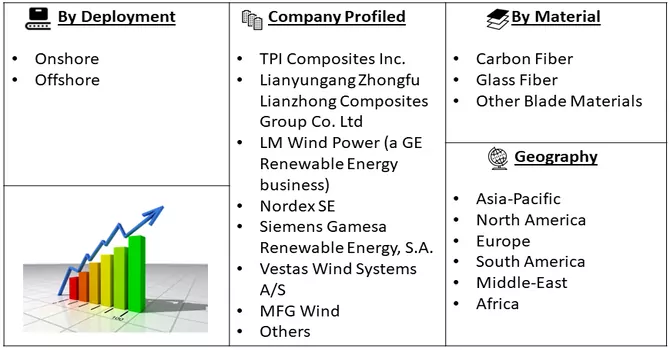

Market Segmentation: The Global Wind Turbine Rotor Blade Market is segmented by Location of Deployment (Onshore and Offshore), Blade Material (Carbon Fiber, Glass Fiber, and Other Blade Materials), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The report offers the market size and forecasts in revenue (USD billion) for all the above segments.

For Detailed Market Segmentation - Download Free Sample PDF

Market Drivers:

Environmental Awareness and Corporate Sustainability Goals

A heightened consciousness of environmental concerns and the concerted efforts of corporations to attain sustainability objectives are fostering a substantial uptick in the embrace of renewable energy sources. Numerous businesses are strategically integrating wind power into their energy portfolios, a move that significantly propels the demand for wind turbine rotor blades. This growing trend reflects a broader industry shift towards cleaner and more eco-friendly energy alternatives. As companies prioritize environmental responsibility, the adoption of wind energy stands out as a pivotal component in achieving both corporate sustainability goals and contributing to the overall demand for advanced wind turbine rotor blade technologies. This shift not only underscores a commitment to greener practices but also signifies a fundamental transformation in the way businesses approach and source their energy needs.

Rising Energy Consumption

The increasing worldwide demand for electricity, coupled with an imperative for cleaner and more sustainable energy solutions, is expediting the widespread deployment of wind turbines. At the heart of this energy transition, wind turbine rotor blades assume a pivotal role, serving as essential components in the capture and conversion of wind energy into electricity. Their significance lies in their ability to harness the kinetic power of the wind, ultimately contributing significantly to the fulfillment of the escalating global power demand. As societies strive for greener and more environmentally conscious energy practices, the integral role of wind turbine rotor blades becomes even more pronounced in meeting the evolving needs of a power-hungry world while prioritizing ecological sustainability.

Market Restraints:

The inconsistency of wind speeds and the intermittent nature of wind resources can lead to fluctuations in power generation, affecting the reliability and stability of wind energy systems. This variability necessitates the integration of energy storage solutions or backup power sources to ensure a continuous and reliable electricity supply, adding complexity and cost to wind energy projects. Additionally, the geographical limitations of optimal wind sites and potential environmental concerns related to the visual and noise impact of wind turbines can pose regulatory and public acceptance challenges, constraining the widespread adoption of wind energy solutions.

The COVID-19 pandemic has significantly impacted the wind turbines market, causing disruptions in the supply chain, project delays, and economic uncertainties. Lockdowns, travel restrictions, and labor shortages have impeded manufacturing and construction activities, affecting the production and deployment of wind turbines. Supply chain interruptions have led to delays in component deliveries, hindering project timelines and increasing costs. Financing challenges and economic uncertainties have also posed obstacles to new wind energy investments. However, the pandemic has underscored the importance of resilient and sustainable energy systems, potentially driving increased focus on renewable energy solutions, including wind power, in post-pandemic recovery plans. The long-term impact on the wind turbines market depends on the duration and severity of the pandemic, global economic recovery, and policy support for renewable energy initiatives.

Segmental Analysis:

Onshore segment is Expected to Witness Significant Growth Over the Forecast Period

The onshore wind turbine rotor blade market plays a pivotal role in the onshore wind energy sector, where the emphasis is on harnessing wind power in terrestrial environments. Onshore wind farms have become a prominent source of renewable energy, contributing significantly to global efforts to transition away from traditional fossil fuels. Rotor blades are crucial components in onshore wind turbines, capturing and converting wind energy into mechanical power that drives electricity generation. As the demand for onshore wind energy continues to grow due to its cost-effectiveness and widespread availability of suitable sites, the market for rotor blades experiences a parallel surge. Manufacturers in this segment focus on developing blades that balance efficiency, durability, and cost-effectiveness, catering to the specific requirements of onshore wind projects. Innovations in blade design, materials, and manufacturing processes are vital in optimizing the performance of onshore wind turbines, making the onshore wind turbine rotor blade market a key contributor to the overall expansion of onshore wind energy capacity.

Glass Fibers segment is Expected to Witness Significant Growth Over the Forecast Period

Glass fibers are fundamental to the turbine rotor blade market, serving as a critical material for wind turbine blade construction. Embedded in composite materials, these fibers provide structural strength, durability, and performance to rotor blades, addressing the unique challenges posed by varying wind speeds and environmental conditions. With high tensile strength and corrosion resistance, glass fiber-reinforced composites are widely adopted in the wind energy sector. Ongoing innovations in glass fiber technology by manufacturers enhance the aerodynamic efficiency and longevity of blades. The utilization of high-performance glass fabrics from leading suppliers has become integral to the design and production of rotor blades, meeting the increasing demand for advanced materials, thereby driving the studied segments; growth.

Asia-Pacific Region is Expected to Witness Significant Growth Over the Forecast Period

The Asia-Pacific region reigns supreme in the global wind turbine rotor blade market, with China acting as the undisputed leader. This dominance stems from several factors. Firstly, China recognized the potential of wind energy early on, leveraging it to power rural areas since 1991. This focus, coupled with supportive policies, R&D investments, and ambitious goals, propelled China's wind capacity to a staggering 338.30 GW in 2021, dwarfing the global competition. Experts predict China's dominance to continue, with estimates suggesting it will hold over 50% of global onshore wind installations by 2050. This growth is fueled by a surging population demanding more electricity, a growing focus on clean energy to combat pollution, and significant investments from both domestic and multinational corporations.

While China takes the lead, India is not far behind, holding the fourth-largest wind power capacity globally in 2021 with 40.08 GW. With ambitious plans to reach 140 GW by 2030, India's wind sector is poised for significant expansion, driving demand for rotor blades and other wind power equipment. This expansion is crucial to meet India's climate commitments and diversify its energy mix.

In conclusion, the Asia-Pacific region, particularly China and India, represent a massive and rapidly growing market for wind turbine rotor blades. This growth is driven by a confluence of factors, including early adoption, supportive policies, ambitious targets, and a growing focus on clean energy. As these trends continue, the region is poised to solidify its position as the global leader in wind energy.

Get Complete Analysis Of The Report - Download Free Sample PDF

The wind turbine rotor blade market is characterized by a fragmented nature, with multiple players operating in diverse segments of the industry. This fragmentation arises from the presence of numerous manufacturers, both established and emerging, offering a range of rotor blade solutions. Various companies contribute to the market, supplying blades of different sizes, materials, and designs to cater to the evolving needs of wind turbine projects worldwide. The competitive landscape is marked by a mix of global leaders, regional players, and niche specialists, each vying for market share. This fragmentation can be attributed to the dynamic and rapidly expanding nature of the wind energy sector, where technological advancements and shifting market demands drive continuous innovation and entrance of new participants. While this diversity fosters innovation, it also poses challenges in terms of standardization and market consolidation, requiring industry participants to navigate a competitive and ever-changing landscape.

Recent Development:

1) In March 2022, a groundbreaking development in the wind energy sector took place with the establishment of the ZEBRA (Zero Waste Blade Research) consortium, marking a pivotal stride toward a circular economy. This initiative unveiled a noteworthy achievement - a 100% recyclable prototype wind turbine blade measuring 62 meters. Crafted with Arkema's Elium resin, renowned for its recyclable properties, and incorporating cutting-edge Glass Fabrics from Owens Corning, the blade exemplifies a sustainable approach in wind turbine production.

2) In March 2022, Hitachi Power Solutions introduced a revolutionary service named "Blade Total Service." This advanced service leverages artificial intelligence, digital technologies, and state-of-the-art drone technology to address various risks faced by wind power facilities, including wear and tear of rotating blades, stress from typhoon winds, and damage caused by lightning. The integration of these innovative technologies is poised to enhance the resilience and longevity of wind power infrastructure.

Q1. What is the current Wind Turbine Rotor Blade Market size?

The Global Wind Turbine Rotor Blade Market size was estimated at about USD 22.8 billion in the current year.

Q2. At what CAGR is the Wind Turbine Rotor Blade market projected to grow within the forecast period?

Wind Turbine Rotor Blade Market is projected to register at a CAGR of about 6.7% during the forecast period.

Q3. What are the factors driving the Wind Turbine Rotor Blade market?

Key factors that are driving the growth include the Environmental Awareness and Corporate Sustainability Goals and Rising Energy Consumption.

Q4. Which Region is expected to hold the highest Market share?

Asia-Pacific region is expected to hold the highest Market share.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model