Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global AI Training and Reasoning Chips Market refers to the industry focused on producing specialized computer chips designed to power artificial intelligence (AI) systems. These chips help machines learn from data (training) and make decisions or solve problems (reasoning) quickly and efficiently. They are used in many fields like robotics, autonomous vehicles, healthcare, and smart devices. As AI technology grows, the demand for these powerful chips increases because they make AI applications faster, smarter, and more reliable. This market includes chip manufacturers, technology developers, and industries adopting AI solutions worldwide, driving innovation and transforming how we live and work.

The Global AI Training and Reasoning Chips Market is witnessing rapid growth driven by increasing adoption of AI across industries like healthcare, automotive, and finance. There is a strong trend toward developing more energy-efficient and high-performance chips that can handle complex AI algorithms with lower latency. Edge computing is gaining traction, pushing demand for AI chips capable of processing data locally without relying on cloud infrastructure. Additionally, advancements in neural network architectures and AI frameworks are encouraging chip manufacturers to innovate and optimize designs specifically for AI workloads. Collaborations between chipmakers and AI software developers are becoming more common to create integrated solutions, fueling faster AI deployment and expanding market opportunities globally.

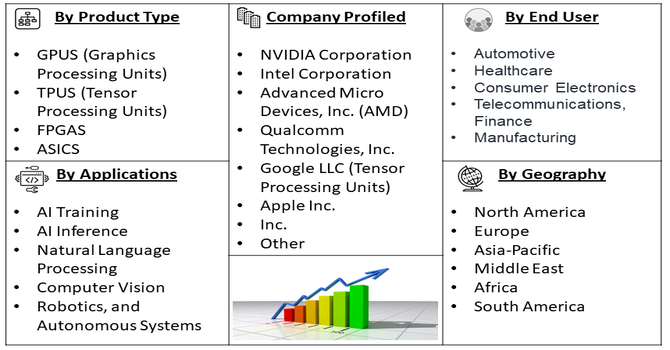

Segmentation: The Global AI Training and Reasoning Chips Market can be segmented by Chip Type (GPUS (Graphics Processing Units), TPUS (Tensor Processing Units), FPGAS (Field-Programmable Gate Arrays), and ASICS (Application-Specific Integrated Circuits)), Applications (AI Training, AI Inference, Natural Language Processing, Computer Vision, Robotics, and Autonomous Systems), End-User Industries (Automotive, Healthcare, Consumer Electronics, Telecommunications, Finance, and Manufacturing) and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The growing adoption of artificial intelligence across various industries is a key driver for the Global AI Training and Reasoning Chips Market. Businesses in healthcare, automotive, finance, and manufacturing increasingly rely on AI technologies to improve efficiency, accuracy, and decision-making. AI training and reasoning chips enable faster processing of complex algorithms, making it possible to handle large datasets and real-time analytics efficiently. As AI applications become more sophisticated, the demand for powerful, specialized chips that can support deep learning, natural language processing, and computer vision continues to rise. This trend fuels investments in research and development, pushing chip manufacturers to innovate and produce higher-performing, energy-efficient solutions that can meet the evolving needs of AI systems globally.

The rapid growth of edge computing is another significant driver of the AI training and reasoning chips market. With more devices generating data locally—such as IoT sensors, smart cameras, and autonomous vehicles—there is an increasing need to process data at the edge rather than relying solely on cloud computing.

AI chips designed for edge devices must be compact, energy-efficient, and capable of performing real-time reasoning tasks. For instance, in July 2024, Qualcomm announced that its Snapdragon 8 Gen 3 processor would power Samsung’s premium smartphones, the Galaxy Z Flip6 and Galaxy Z Fold6. The new chipset features advanced capabilities designed to support Galaxy AI, enabling enhanced gaming performance, improved camera functions, and smarter productivity features, positioning it as a key enabler of next-gen mobile experiences. This demand is encouraging manufacturers to develop specialized chips optimized for edge AI workloads, enhancing latency, security, and privacy by reducing the need to transmit sensitive data to centralized servers. As edge computing expands, it will continue to drive growth and innovation in the AI chip market worldwide.

Market Restraints:

The major restraint for the Global AI Training and Reasoning Chips Market is the high cost associated with developing and manufacturing advanced AI chips. Designing chips capable of supporting complex AI models requires significant investment in research, sophisticated fabrication technologies, and skilled talent. Additionally, manufacturing these chips often involves expensive semiconductor fabrication facilities and cutting-edge materials, which increases production costs. These high expenses can limit accessibility for smaller businesses or startups, potentially slowing overall market adoption. Furthermore, the complexity of integrating AI chips into existing infrastructure can lead to longer deployment times and higher operational costs. These factors combined may restrict market growth, especially in regions with limited technological infrastructure or lower financial resources.

The AI Training and Reasoning Chips Market significantly impacts society and the economy by enabling smarter technologies that improve daily life and drive economic growth. These chips power AI systems that enhance medical diagnoses, autonomous driving, personalized education, and efficient manufacturing, boosting productivity and innovation. The market also creates high-skilled jobs in chip design, AI research, and software development. However, it raises challenges such as workforce displacement and data privacy concerns, which require thoughtful policy responses. Overall, the widespread adoption of AI chips supports economic competitiveness by fostering technological advancements and driving digital transformation across sectors, contributing to improved quality of life and global economic development.

Segmental Analysis:

The TPUs segment is projected to see significant growth as these specialized processors are designed specifically to accelerate machine learning tasks, especially deep learning and neural network workloads. TPUs offer higher performance and energy efficiency compared to traditional CPUs and GPUs, making them ideal for AI training and inference. With growing demand for faster and more efficient AI computation in industries such as healthcare, automotive, and finance, TPUs are becoming the preferred choice for developers and enterprises. Cloud service providers are increasingly integrating TPUs into their infrastructure, further driving adoption. As AI applications continue to evolve in complexity and scale, TPUs’ ability to handle large-scale data processing will fuel strong growth in this segment over the forecast period.

The AI training segment is expected to experience robust growth due to the rising need for powerful hardware capable of processing vast datasets and complex algorithms. Training AI models requires significant computational resources, driving demand for high-performance AI training chips like GPUs, TPUs, and ASICs. Organizations across industries are investing heavily in AI research and development, leading to increased spending on training infrastructure. Moreover, the expansion of cloud-based AI services and platforms has made training more accessible and scalable. As AI adoption grows, the need to build more accurate, sophisticated models will continue to push demand for advanced training chips, making this segment one of the fastest-growing areas in the AI chip market.

The telecommunications segment is poised for significant growth as telecom companies increasingly integrate AI technologies to enhance network management, improve customer service, and optimize operations. AI chips are critical in enabling real-time data processing and decision-making for 5G networks, network security, and predictive maintenance. With the rollout of 5G and the growing number of connected devices, telecom providers require efficient AI chips to handle vast amounts of data at high speeds and low latency. This drives demand for specialized AI training and reasoning chips that support complex analytics and automation. As telecom networks become smarter and more automated, the adoption of AI chips in this sector is expected to rise substantially over the forecast period.

North America is anticipated to lead significant growth in the AI training and reasoning chips market due to its well-established semiconductor industry, strong presence of major technology companies, and high AI adoption rates. The region benefits from substantial investments in AI research and infrastructure by both public and private sectors. Additionally, the presence of key chip manufacturers and AI startups fosters innovation and rapid deployment of advanced AI hardware solutions. Government initiatives supporting AI development and digital transformation further boost market expansion.

With increasing demand across industries like healthcare, automotive, finance, and telecommunications, North America is expected to remain a dominant market, driving growth in AI chip production and adoption during the forecast period. For instance, in August 2024, AMD acquired Silo AI, a European AI lab, as part of its strategy to strengthen its AI model offerings. By bringing in Silo AI’s team of experienced engineers and scientists—known for developing open-source, multilingual large language models like Viking and Poro on AMD platforms—AMD aims to boost its capabilities and accelerate innovation in the AI space. Thus, such developments are fueling the market growth.

| Report Matrics | Details |

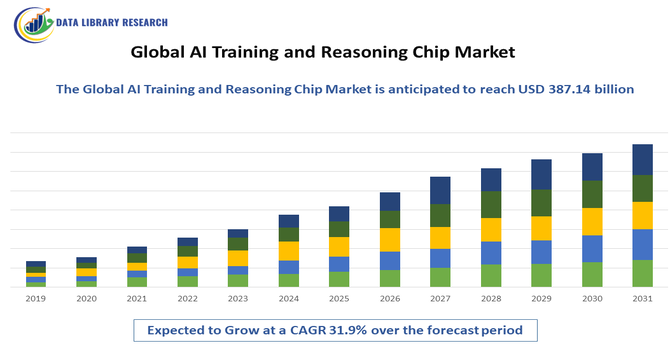

| Market Size Value | USD 387.14 billion |

| Growth Rate | CAGR of 31.9 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global AI Training and Reasoning Chips Market is dominated by a mix of established semiconductor giants and innovative startups. Major players like NVIDIA, Intel, AMD, and Qualcomm lead the market with advanced GPU and AI-specific chip technologies. At the same time, emerging companies focus on specialized AI accelerators and edge AI chips, driving innovation and market diversification. Collaborations and strategic partnerships between chip manufacturers, AI software firms, and cloud service providers are common to deliver optimized AI solutions. Intense competition encourages continuous R&D investment to enhance chip performance, reduce power consumption, and lower costs. This dynamic environment pushes companies to differentiate through technological advances and tailored applications for various industries worldwide.

Here are 20 major players in the Global AI Training and Reasoning Chips Market:

Recent News:

Q1. What are the main growth driving factors for this market?

The main growth drivers are the exponential demand for high-performance computing to handle complex AI models like Large Language Models (LLMs) and deep neural networks, especially in data centers. This is further fueled by the massive adoption of AI across key sectors such as automotive for autonomous vehicles, healthcare for diagnostics, and finance for risk management, all of which require specialized, low-latency, and energy-efficient training and reasoning silicon. The continuous advancement in AI and ML algorithms necessitates more powerful dedicated hardware.

Q2. What are the main restraining factors for this market?

Key restraining factors include the extremely high initial capital expenditure and R&D costs required for designing and manufacturing cutting-edge chips (ASICs/GPUs) at advanced process nodes. Additionally, the market is severely impacted by global supply chain volatility, raw material shortages, and geopolitical tensions, particularly US export controls and tariffs, which limit the availability of the most advanced chips in certain regions, escalating production costs and operational complexity.

Q3. Which segment is expected to witness high growth?

The Edge AI Computing segment, which focuses on reasoning/inference chips for local processing on devices, is expected to witness the highest growth rate. This is driven by the rising proliferation of smart, connected devices like smartphones, IoT sensors, and autonomous vehicles that require real-time, low-latency decision-making capabilities without relying on the cloud. Concurrently, the ASIC (Application-Specific Integrated Circuit) chip segment is also anticipated to grow rapidly due to its superior power efficiency and performance-per-watt for specific AI workloads.

Q4. Who are the top major players for this market?

The competitive landscape is dominated by a few global technology giants. The top major players include NVIDIA, which holds an overwhelming market share in the training chip segment with its high-performance GPUs, followed by AMD, which is rapidly gaining ground with its Instinct accelerators, and hyperscalers like Google (with its custom TPUs), Intel, and AWS (with Trainium and Inferentia). Emerging AI chip startups like Groq and Cerebras are also disrupting the inference and large model space.

Q5. Which country is the largest player?

The United States is the largest country player, dominating the global AI Training and Reasoning Chips Market. This leadership is secured by the presence of all the major chip design leaders (NVIDIA, AMD, Intel, Google, AWS) and a robust ecosystem of substantial R&D investments, advanced semiconductor technology infrastructure, and early, widespread adoption of AI technologies across defense, healthcare, and hyperscale cloud data centers, solidifying its dominant revenue share.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model