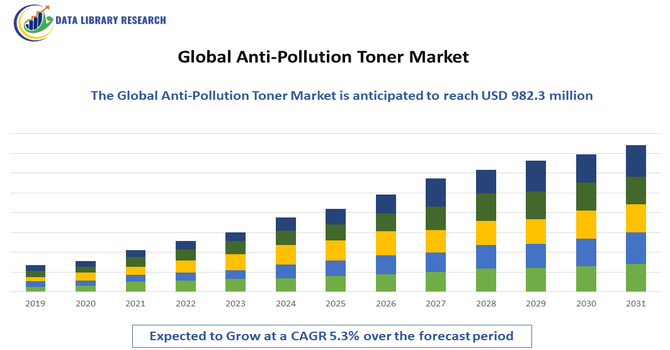

The Global Anti Pollution Toner Market was worth USD 586.1 million in 2025, and is predicted to grow to USD 982.3 million by 2035, with a CAGR of 5.3% from 2026-2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Anti Pollution Toner Market refers to the worldwide industry segment dedicated to toners formulated to help protect skin against environmental pollutants such as particulate matter (PM2.5), urban smog, UV radiation, and oxidative stress. These toners often contain antioxidants, botanical extracts, and barrier strengthening actives designed to detoxify, balance pH, and reinforce skin defense mechanisms. Anti pollution toners are increasingly integrated into daily skincare routines to mitigate pollution induced concerns like premature aging, sensitivity, and dullness. The market serves a broad demographic with products targeted by age, skin type, and gender, sold through online and traditional retail channels. The growth is fueled by rising pollution awareness, urbanization, and skincare adoption globally.

Key trends shaping the Global Anti Pollution Toner Market include formulation innovation with multifunctional actives and barrier boosting ingredients that defend against urban aggressors. There is a growing preference for natural, organic, and alcohol free toners catering to sensitive skin and clean beauty segments. Digital and social media influence, including beauty bloggers and K Beauty routines, is driving consumer education and product adoption. E commerce platforms have become dominant sales channels, offering wide choice and convenience. Brands are also leveraging eco friendly packaging and sustainable practices to appeal to environmentally conscious consumers. Personalized and targeted toners addressing specific concerns, such as blue light protection and PM2.5 defense, are gaining traction as consumer expectations evolve.

Segmentation: The Global Anti Pollution Toner Market is segmented by Product Type (Alcohol Free Toners, Hydrating Toners, Astringent Toners, Exfoliating Toners, and Botanical/Herbal Toners), Ingredient Type (Antioxidants, Botanical Extracts, Hyaluronic Acid, Niacinamide and Others), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores/Beauty Retailers, Pharmacies/Drugstores, Online Retail and Direct Sales), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing adoption of online retail platforms and digital beauty channels, which have expanded product accessibility and consumer reach. E commerce offers broad selection, detailed product information, reviews, and personalized recommendations that accelerate purchasing decisions. Social media influencers and beauty communities educate consumers on the benefits of anti pollution toners, elevating product visibility.

Online channels also support direct to consumer models, enabling niche and indie brands to compete with established players. For instance, in 2023, L'Oréal’s acquisition of Aesop enhances its luxury portfolio, accelerating digital beauty channel growth and online retail adoption. This expansion drives broader access to premium anti-pollution toners, boosting the Global Anti-Pollution Toner Market by meeting rising consumer demand for convenient, high-end skincare. The trend of digital skincare consultations, AR virtual try ons, and customized routines further enhances engagement and drives demand across demographic groups, particularly among younger consumers seeking targeted skincare solutions.

The rising environmental pollution and urban exposure, which increases consumer awareness of pollution induced skin damage, such as premature aging, sensitivity, and inflammation. Rapid urbanization and industrialization in developing economies have heightened demand for skincare products that offer protective benefits against airborne pollutants and oxidative stress. As more people live in megacities with poor air quality, the role of anti pollution toners as a daily shield has become increasingly recognized. This concern is amplified by social media and beauty education, making pollution defense a staple within skincare routines and fostering continuous market growth.

Market Restraints:

Different regions have varying regulations governing cosmetic claims related to anti pollution efficacy, requiring clinical substantiation and compliance documentation. This increases development costs and extends time to market, particularly for smaller brands with limited resources. Additionally, skepticism over efficacy and concerns about “greenwashing” can dampen consumer trust, especially when claims are not backed by recognized scientific validation. Ingredient restrictions and safety testing requirements further increase compliance burdens on manufacturers, potentially slowing product launches and affecting market expansion in regulatory sensitive countries.

The anti pollution toner market influences socioeconomic trends by responding to heightened public concern over environmental health and skin wellbeing, particularly in urban regions where pollution levels are high. Increased disposable income and beautification trends have boosted skincare spending, especially among millennials and Gen Z. Growth of online retail platforms has expanded employment and entrepreneurship opportunities in beauty and personal care. Heightened demand encourages ingredient research, sustainable sourcing, and manufacturing in multiple regions, creating jobs and economic activity. Educational campaigns on pollution impacts also raise public health awareness. As air quality concerns persist globally, anti pollution skincare adoption supports broader consumer priorities around preventive health and wellness.

Segmental Analysis:

The hydrating toners segment is expected to experience the highest growth over the forecast period as consumers increasingly prioritize multifunctional skincare that delivers both pollution protection and deep hydration. With growing awareness of environmental stressors that deplete skin moisture and cause irritation, hydrating toners infused with humectants and barrier strengthening ingredients have become essential in daily routines. Urban populations exposed to harsh air quality conditions seek products that restore moisture balance while reinforcing skin defenses. Innovations incorporating soothing and replenishing agents have further bolstered demand. As beauty trends continue to emphasize hydration and skin health, this segment’s comprehensive benefits and broad consumer appeal will drive robust market expansion.

The hyaluronic acid segment is expected to witness the highest growth over the forecast period due to its strong appeal as a potent hydrating and anti aging ingredient in anti pollution toners. Hyaluronic acid’s ability to attract and retain moisture supports skin barrier resilience against environmental aggressors like pollution, UV exposure, and oxidative stress. Consumers increasingly seek science backed skincare with visible, immediate results, and hyaluronic acid’s proven efficacy resonates across age groups. Its compatibility with diverse formulations and suitability for all skin types further accelerates adoption. As brands continue to spotlight hyaluronic acid in marketing and product development, demand for toners featuring this ingredient is projected to surge globally.

The specialty stores/beauty retailers segment is anticipated to witness the highest growth in the Global Anti Pollution Toner Market over the forecast period due to their curated product offerings, expert guidance, and experiential shopping environments. Consumers seeking premium and targeted skincare solutions increasingly prefer beauty retail destinations that provide personalized recommendations and opportunities to trial products before purchase. These channels attract brand conscious customers drawn to innovative anti pollution toners, including clean beauty, luxury, and dermatologist endorsed options. Specialty retailers also often host exclusive launches and brand activations, boosting visibility and consumer engagement. As competition intensifies and beauty expertise becomes a key differentiator, specialty stores and beauty retail channels will drive significant market growth.

The Asia Pacific region is expected to witness the highest growth in the Global Anti Pollution Toner Market over the forecast period, fueled by rapid urbanization, increasing pollution levels, and a booming beauty and personal care sector.

Consumers in countries such as China, India, South Korea, and Japan are increasingly adopting anti pollution skincare as part of daily routines, driven by heightened awareness of environmental skin damage and social media influence. For instance, in 2020, Yuhan-Kimberly’s launched RED TO RAD anti-pollution skincare product strengthens its presence in South Korea’s adult cosmetics segment, targeting women aged 25–34. With features that resist particulate matter and reduce fine dust adhesion, the product is expected to boost demand for anti-pollution toners, expanding the market for protective, everyday skincare solutions in the country.

Rising disposable incomes, expanding middle class populations, and aggressive e commerce penetration further support market expansion. Additionally, strong demand for innovative, multifunctional beauty products and localized formulations that address diverse skin concerns positions the Asia Pacific region as the fastest growing market globally.

| Report Matrics | Details |

| Market Size Value | USD 982.3 million |

| Growth Rate | CAGR of 5.3% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The Global Anti Pollution Toner Market features competition between major multinational beauty brands and niche players innovating specialized formulations. Established companies leverage extensive R&D, global distribution networks, and strong marketing to maintain market share, while smaller brands differentiate through natural, organic, or customizable products. Mergers, partnerships, and product line expansions drive portfolio diversity. Online retail channels and influencer led promotions intensify competition for visibility and consumer loyalty. Geographical strategies vary, with Western brands emphasizing clinical efficacy and sustainability, and Asian producers focusing on multifunctional and traditional ingredient blends. Barriers to entry include formulation expertise, regulatory compliance, and distribution scale, yet growing consumer demand continues to attract new entrants.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The increasing urbanization and rising environmental pollution levels are primary drivers, as consumers seek products to shield skin from particulate matter and toxins. Growing awareness of "inflammaging"—premature aging caused by pollutants—fuels demand. Additionally, the shift toward natural, antioxidant-rich formulations and high-performance skincare routines in emerging economies significantly boosts market expansion.

Q2. What are the main restraining factors for this market?

The high price point of premium anti-pollution formulations often limits accessibility for middle-income consumers, acting as a major restraint. Furthermore, a lack of standardized testing protocols to verify "anti-pollution" claims can lead to consumer skepticism. Competition from multi-functional products, like sunscreens or moisturizers that already include protective barriers, also hinders growth.

Q3. Which segment is expected to witness high growth?

The hyaluronic acid segment is projected to witness the highest growth over the forecast period, driven by rising consumer demand for anti-aging and skin hydration products. Increasing awareness of its benefits in skincare, joint health, and medical applications, along with expanding use in cosmetic procedures, is fueling market expansion. Innovations in formulation and rising disposable incomes further support its rapid adoption globally.

Q4. Who are the top major players for this market?

Top major players include global beauty giants such as L'Oréal S.A., The Estée Lauder Companies Inc., and Beiersdorf AG. Specialized brands like Clarins, Unilever (via Dermalogica), and Shiseido Company, Limited also hold significant shares. These companies focus on R&D to develop proprietary complexes that neutralize free radicals and strengthen skin barriers.

Q5. Which country is the largest player?

China is the largest player in the anti-pollution toner market. This dominance is driven by high pollution levels in major industrial hubs and a sophisticated consumer base that prioritizes preventative skincare. The country’s massive e-commerce ecosystem and the rapid rise of domestic "C-Beauty" brands further solidify its leading global position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model