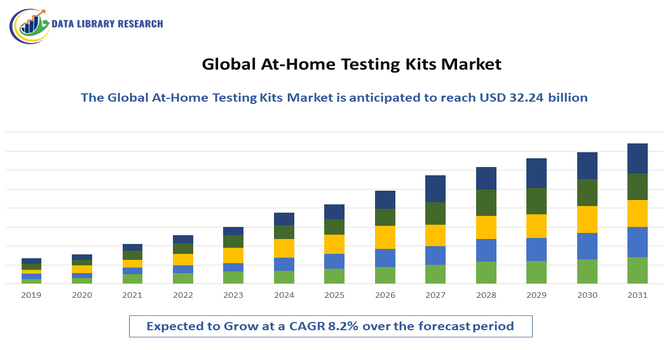

The Global At-Home Testing Kits Market, is valued at USD 17 billion in 2025, is projected to grow to 32.24 billion by 2035, growing with a CAGR of 8.2% from 2025-2032.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global At-Home Testing Kits Market refers to the industry focused on the development, production, and distribution of diagnostic kits that allow individuals to test for various health conditions from the comfort of their homes without needing clinical supervision. These kits cover a broad range of applications, including infectious diseases (e.g., COVID-19, HIV), chronic conditions (e.g., diabetes), fertility and pregnancy, genetic testing, and general wellness. Market growth is driven by increasing consumer demand for convenience, privacy, faster results, and cost-effective healthcare solutions. Technological advancements, rising health awareness, and the expansion of telehealth services are further propelling adoption. Regulatory support and growing interest in preventive healthcare are also key factors contributing to the rapid global expansion of this market.

The Global At-Home Testing Kits Market is experiencing rapid growth, driven by rising consumer demand for accessible, private, and time-saving health diagnostics. A major trend is the increasing integration of digital technologies, such as app-based result tracking, telehealth integration, and AI-powered interpretations. Post-COVID-19, consumers have become more proactive about health monitoring, boosting demand for self-administered tests for infectious diseases, fertility, hormone levels, and chronic condition management. Subscription-based testing models and DTC (direct-to-consumer) channels are gaining traction, offering recurring test kits with personalized health insights. Additionally, growing investment in biotechnology and molecular diagnostics is fueling innovation in accuracy, ease-of-use, and regulatory-compliant solutions, reshaping consumer expectations and setting new benchmarks for home-based healthcare diagnostics.

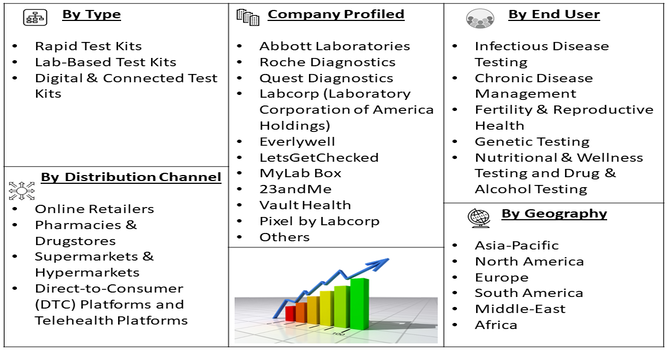

Segmentation: The Global At-Home Testing Kits Market is Segmented by Type (Rapid Test Kits, Lab-Based Test Kits and Digital & Connected Test Kits), Sample Type (Blood, Urine, Saliva, Nasal or Throat Swab and Stool), Test Type (Diagnostic Tests, Monitoring Tests, Screening Tests, and Predictive & Preventive Tests), Application (Infectious Disease Testing, Chronic Disease Management, Fertility & Reproductive Health, Genetic Testing, Nutritional & Wellness Testing and Drug & Alcohol Testing), Distribution Channel (Online Retailers, Pharmacies & Drugstores, Supermarkets & Hypermarkets, Direct-to-Consumer (DTC) Platforms and Telehealth Platforms), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

People today are looking for more control over their health, especially after the COVID-19 pandemic. At-home testing kits let individuals check for everything from infections to fertility and vitamin levels — all without needing to visit a clinic or lab. This convenience, privacy, and ability to test anytime is a big reason why more people are choosing at-home options. It saves time, avoids waiting rooms, and gives quick results. As healthcare becomes more consumer-focused, these kits are becoming part of regular health habits, just like wearable fitness trackers. This shift in behavior is driving strong demand and growth in the at-home testing market around the world.

Digital health tools like health apps, online consultations, and telemedicine are making it easier than ever to use at-home testing kits. Many companies now offer kits that work alongside smartphone apps or online platforms, helping users track results, consult doctors, or even receive prescriptions without visiting a clinic.

This digital integration makes home testing more reliable and user-friendly. It’s especially helpful for people in remote areas or those who prefer managing their health from home. For instance, in August 2024, Pfizer Inc. launched PfizerForAll, a user-friendly digital platform designed to simplify healthcare access and management for millions of Americans. The platform integrated resources for managing common illnesses like migraines, COVID-19, flu, and adult vaccinations, streamlining care, prescriptions, and cost savings. This innovation enhanced patient convenience and engagement in health management. By advancing digital health solutions, PfizerForAll contributed to the growth of digital health and telemedicine, indirectly boosting demand for connected at-home testing kits and related healthcare technologies. As telehealth services continue to grow and become more accepted by both doctors and patients, the demand for smart, connected testing kits is also rising, helping push the overall market forward.

Market Restraints:

The one challenge in the at-home testing kits market is that some users worry about how accurate the results are. Unlike tests done in professional labs, home tests may be affected by how well the person follows the instructions or handles the sample. Misuse, unclear directions, or poor sample collection can lead to wrong results, which might cause stress or false reassurance. Also, some people may not fully understand what their test results mean or when to seek medical advice. These concerns can make both users and healthcare professionals cautious about relying too heavily on at-home tests, which could slow down adoption in certain parts of the market.

The growth of the at-home testing kits market is significantly transforming access to healthcare, especially in underserved or remote areas with limited clinical infrastructure. By empowering individuals to monitor their health privately and conveniently, these kits are reducing the burden on healthcare systems and enabling early detection of diseases, which can lead to better outcomes and cost savings. They also promote health equity by offering lower-cost alternatives to traditional lab testing. However, socioeconomic disparities still exist in terms of digital access, health literacy, and affordability, which may limit adoption in certain populations. Overall, the market is playing a vital role in democratizing healthcare and promoting a shift toward personalized and preventive medicine.

Segmental Analysis:

The Lab-Based Test Kits segment is poised for the highest growth due to a converging set of factors emphasizing convenience and clinical depth. These kits allow for at-home sample collection (like blood or saliva) with subsequent professional analysis in a certified lab, offering a high degree of accuracy and reliability for complex diagnostics such as genetic screening, comprehensive wellness panels, and advanced infectious disease testing. This model is perfectly positioned to cater to the rising consumer interest in proactive, personalized healthcare. For instance, in May 2025, US FDA approved the first at-home test for cervical cancer screening, marking a significant milestone in accessible healthcare. This approval allowed women to conveniently screen for cervical cancer from home, improving early detection rates. The development supported the shift toward preventive care and empowered individuals with more control over their health. It also expanded the at-home testing kits market by introducing a critical diagnostic option for women’s health.

Furthermore, the integration of these services with digital platforms for result delivery and remote consultation enhances the user experience, driving broader consumer adoption across various demographics who value both ease of use and clinically validated results.

The blood segment is expected to lead growth, primarily driven by the crucial role blood samples play in monitoring a wide array of chronic diseases and assessing overall health markers with high accuracy. Blood-based at-home tests for vital metrics like glucose, cholesterol, and various hormone levels are essential for managing prevalent conditions such as diabetes and cardiovascular diseases. Innovations in sample collection, particularly user-friendly finger-prick technologies and dried blood spot (DBS) collection kits, have significantly reduced the invasiveness and intimidation associated with at-home blood draws. This convenience, combined with the clinically accepted reliability of blood analysis, makes the segment indispensable for continuous and routine health management.

Highest growth in the Monitoring Tests segment is anticipated, fundamentally fueled by the escalating global prevalence of chronic conditions requiring routine and long-term oversight. Conditions like hypertension, diabetes, and certain thyroid disorders necessitate frequent testing to track disease progression, adjust medication, and prevent acute complications. At-home monitoring tests offer patients the essential convenience and autonomy to perform checks on their own schedule, avoiding frequent clinic visits. This empowerment, coupled with the integration of smart devices and telemedicine platforms that allow real-time data sharing with healthcare providers, transforms intermittent testing into continuous, proactive patient care, solidifying the segment's rapid expansion.

The Chronic Disease Management segment is projected to exhibit the highest growth, intrinsically linked to the increasing global burden of non-communicable diseases. As populations age and lifestyle-related diseases become more common, the necessity for cost-effective, continuous patient management solutions grows. At-home testing kits for chronic care, such as continuous glucose monitors or at-home blood pressure monitors, are key enablers of decentralized healthcare. They improve patient adherence to treatment, facilitate early detection of issues, and lower overall healthcare costs by reducing emergency room visits. This transition towards remote patient monitoring and value-based care is a primary driver for the sustained, rapid growth of this application segment.

The Pharmacies & Drugstores segment is expected to dominate distribution growth due to its established infrastructure, accessibility, and high consumer trust. These retail points are often the first and most convenient stop for consumers seeking immediate health solutions, including over-the-counter diagnostic kits like pregnancy, COVID-19, and basic wellness tests. The presence of licensed pharmacists provides a crucial layer of professional guidance and credibility, which is vital for consumer confidence in self-testing products. Their wide geographical reach and existing role as community healthcare hubs make them an essential, trusted, and high-volume channel for the immediate availability and purchase of at-home test kits.

High growth for Supermarkets & Hypermarkets as a distribution channel is anticipated due to the unparalleled convenience and foot traffic they command. These large retail formats offer at-home testing kits alongside regular household shopping, normalizing the purchase of such products as part of a routine weekly shop. Their broad reach, extended operating hours, and competitive pricing strategy make basic and over-the-counter health tests highly accessible and affordable to a vast consumer base. The sheer volume of transactions and the consumer preference for a single-stop solution for diverse needs drive the market penetration and subsequent rapid growth of the at-home testing market through this channel.

North America is anticipated to lead regional growth, primarily driven by its sophisticated healthcare infrastructure, high consumer adoption of advanced technologies, and robust purchasing power. The region benefits from favorable regulatory frameworks and high awareness regarding preventive and personalized healthcare. For instance, in April 2025, The U.S. FDA granted marketing authorization to Visby Medical for the first at-home, prescription-free test for three common STIs: chlamydia, gonorrhea, and trichomoniasis. Designed for women with or without symptoms, the single-use kit provided results within 30 minutes via the Visby Medical App. This innovation improved access to rapid, private sexual health testing. It significantly boosted consumer trust and demand in the at-home testing kits market, especially in the sexual health segment.

A strong presence of key market players, significant investment in research and development, and the widespread integration of telehealth and remote patient monitoring services further accelerate market expansion. For instance, in March 2022, Walgreens and Labcorp announced the nationwide availability of the Pixel by Labcorp COVID-19 at-home PCR collection kit through Labcorp OnDemand, offered at no cost to eligible individuals. The kits, launched in partnership with the U.S. Department of Health and Human Services (HHS), aimed to expand access to reliable and convenient testing. This initiative brought testing directly into communities, enhancing public health response. It also reinforced consumer trust in self-testing and drove growth in the at-home testing kits market.

The high prevalence of chronic diseases and established insurance coverage for diagnostic services also ensure sustained demand, positioning North America as the dominant and fastest-growing market.

| Report Matrics | Details |

| Market Size Value | USD 32.24 billion |

| Growth Rate | CAGR of 8.2% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The at-home testing kits market is highly competitive, with key players including Abbott, Roche, Everlywell, LetsGetChecked, MyLab Box, and 23andMe leading the way. These companies compete on technology, regulatory compliance, test variety, and user experience. Startups and digital health companies are rapidly entering the space, introducing innovative, niche-specific tests and expanding into wellness and preventive care. Larger diagnostics firms are leveraging brand trust, scalability, and global distribution to maintain market dominance. Strategic partnerships with telehealth providers and pharmacies are also shaping the landscape, enabling end-to-end healthcare solutions. The market is also seeing increased M&A activity and R&D investments as players aim to diversify offerings and improve test accuracy, affordability, and digital integration.

The 20 major players for above market are:

Recent Development

Q1. What the main growth driving factors for this market?

The main growth drivers are increasing consumer demand for convenience, privacy, and rapid results in healthcare. The rising global prevalence of chronic diseases, a heightened focus on preventive health management post-pandemic, and technological advancements that make kits more accurate and user-friendly, all contribute significantly. Furthermore, the ease of purchasing kits through online and retail pharmacies fuels market expansion by making diagnostics more accessible outside of traditional clinical settings.

Q2. What are the main restraining factors for this market?

The market's expansion is primarily restrained by concerns over test accuracy and reliability for self-administered kits, which can lead to user error and subsequent false results or unnecessary anxiety. Other significant hurdles include the stringent and often delayed regulatory approval processes for new kits and the high cost associated with some advanced testing kits, which can limit their accessibility, especially in developing regions or for populations without adequate insurance coverage.

Q3. Which segment is expected to witness high growth?

The infectious disease testing segment, particularly for emerging and prevalent diseases, is expected to witness high growth, driven by continuous public health awareness and the ongoing need for rapid diagnostics. Also, the segment related to chronic disease monitoring, such as for diabetes and cardiovascular health, is projected for substantial growth due to the rising burden of these conditions and the convenience of at-home, regular self-monitoring.

Q4. Who are the top major players for this market?

The market is characterized by a mix of established global healthcare giants and specialized direct-to-consumer diagnostics companies. Top major players include leading firms like Abbott Laboratories, F. Hoffmann-La Roche AG, Becton, Dickinson and Company (BD), and Danaher Corporation. Additionally, companies focused on consumer diagnostics, such as Everly Health (Everlywell), are also considered dominant forces due to their direct-to-consumer reach and innovative offerings.

Q5. Which country is the largest player?

The United States is consistently reported as the largest and most dominant player in the global at-home testing kits market, particularly within the North American region. This dominance is driven by a combination of factors including advanced healthcare infrastructure, high consumer spending on health and wellness, a strong presence of key diagnostics and biotech companies, and the widespread adoption of digital health and telehealth platforms.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model