Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Bispecific Antibody Molecular Drug Market refers to the worldwide industry focused on developing, manufacturing, and commercializing bispecific antibody drugs—therapeutic molecules engineered to bind two different antigens or epitopes simultaneously. These innovative biologics enhance targeted treatment efficacy, especially in oncology and autoimmune diseases. Fueled by advancements in biologics engineering and clinical validation, this market is expanding rapidly as pharmaceutical companies and research institutions develop next-generation therapies for complex diseases.

The bispecific antibody market is driven by increased R&D investment and clinical successes in cancer immunotherapy, particularly in hematologic malignancies and solid tumors. Advancements in engineering platforms, such as BiTEs (bispecific T cell engagers) and dual affinity retargeting (DART) technologies, are enabling more effective and safer drug candidates. Strategic collaborations between biotech firms and large pharmaceutical companies are accelerating pipeline development and regulatory approvals. Additionally, expansion into non oncology indications, such as inflammatory and neurological diseases, is broadening market potential. Regulatory agencies are also providing accelerated pathways for breakthrough therapies, further encouraging innovation and adoption of bispecific antibody drugs globally.

Segmentation: The Global Bispecific Antibody Molecular Drug Market is segmented by Therapeutic Area (Oncology, Autoimmune & Inflammatory Diseases, Hematology and Infectious Diseases & Others), Molecule Type (IgG-like Molecules and Fragment-based), Mechanism of Action (Immune Cell Redirectors and Dual Pathway Blockers), Technology Platform (BiTE (Amgen), DART (MacroGenics), DuoBody (Genmab) and CrossMAb (Roche)), End-User (Hospital Pharmacies, Specialty Clinics and Online & Retail Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing global prevalence of cancer and other chronic diseases is a key driver for the bispecific antibody molecular drug market. Bispecific antibodies offer targeted therapy by simultaneously binding to two distinct antigens, enhancing therapeutic efficacy and reducing off-target effects compared to traditional monoclonal antibodies.

With cancer incidence rising and many patients developing resistance to conventional therapies, demand for innovative treatments is accelerating. For instance, The Lancet reported that by 2050, 30.5 million new diagnoses , with over half of cases and two-thirds of deaths occurring in low- and middle-income countries, highlighting a critical need for urgent action and targeted funding.

Governments and healthcare providers are prioritizing advanced biologics to improve patient outcomes. This rising disease burden, coupled with awareness of bispecific antibodies’ potential to treat complex conditions, is driving research, development, and market adoption globally.

Technological advancements in antibody engineering, including BiTEs (bispecific T-cell engagers), DART (dual affinity retargeting), and other platforms, are significantly driving the bispecific antibody market. Innovations allow the creation of antibodies with higher specificity, improved stability, and reduced immunogenicity, enabling effective targeting of tumors and immune modulation. Integration of AI-driven drug design and high-throughput screening accelerates candidate identification and preclinical development.

In October 2025, Alphamab Oncology announced the first patient dosing in a Phase I trial of JSKN022, an innovative bispecific antibody-drug conjugate targeting PD-L1 and integrin αvβ6, marking the world’s first PD-L1/αvβ6 bispecific ADC to enter clinical development. These technological advancements empower pharmaceutical companies to produce safer, more effective bispecific antibodies, expanding clinical applications and strengthening global market growth.

Market Restraints:

High development costs and complex manufacturing processes remain significant restraints for the bispecific antibody molecular drug market. Producing bispecific antibodies involves intricate protein engineering, quality control, and scaling challenges, leading to substantial R&D and production expenses. Regulatory compliance, clinical trial requirements, and stringent safety standards further increase costs and development timelines. These factors limit the ability of smaller companies to compete and slow the introduction of new therapies. Additionally, high treatment costs for patients can restrict market penetration in price-sensitive regions. Consequently, despite strong demand and technological advances, financial and operational barriers continue to constrain widespread adoption of bispecific antibody drugs globally.

Bispecific antibody drugs significantly impact healthcare by offering more effective treatments for conditions with unmet medical needs, improving patient survival and quality of life, particularly in oncology. These therapies can reduce long term healthcare costs by enhancing treatment specificity and reducing adverse effects. However, high development and treatment costs raise affordability and access challenges, especially in low and middle income regions. The demand for specialized manufacturing and skilled professionals creates high value jobs and stimulates biotech innovation. Policymakers and healthcare systems must balance encouraging innovation with ensuring equitable access. Ultimately, bispecific antibodies represent a transformative class of therapeutics that influence clinical outcomes and healthcare economics globally.

Segmental Analysis:

The oncology segment is projected to witness the highest growth over the forecast period due to the rising global incidence of cancer and the urgent need for targeted therapies. Bispecific antibodies can simultaneously engage tumor antigens and immune effector cells, enhancing antitumor activity and improving patient outcomes. Clinical successes in hematologic malignancies and solid tumors have demonstrated efficacy, encouraging adoption in cancer treatment protocols. Strategic collaborations between pharmaceutical companies and oncology research centers are accelerating the development of novel bispecific therapies. With growing investment in oncology R&D and increasing regulatory approvals, bispecific antibodies are poised to become a central component of cancer therapy.

The IgG-like molecules segment is expected to experience the highest growth due to their structural similarity to natural antibodies, which provides favorable pharmacokinetics, stability, and reduced immunogenicity. These molecules are versatile, allowing for dual targeting of tumor antigens and immune cells, making them suitable for multiple therapeutic applications. Advances in protein engineering and high-throughput screening have enhanced the efficiency of IgG-like bispecific antibodies, supporting large-scale production and clinical translation. Their proven safety profiles and adaptability across oncology and autoimmune indications increase market demand. As pharmaceutical companies prioritize effective and reliable antibody formats, the IgG-like segment is projected to dominate growth in the bispecific antibody market.

The immune cell redirectors segment is anticipated to witness the highest growth as these bispecific antibodies actively engage and redirect immune effector cells, such as T-cells, to target diseased cells. This approach enhances the body’s natural immune response against cancer and other conditions with high precision. Successes in T-cell engager therapies and ongoing clinical trials highlight their efficacy in hematologic and solid tumors. Increasing investment in immuno-oncology and advancements in safety and specificity further drive adoption. As healthcare providers seek therapies that combine high efficacy with reduced systemic toxicity, immune cell redirectors are becoming a focal point of bispecific antibody development and commercialization.

The DART (Dual-Affinity Re-Targeting) segment by MacroGenics is expected to witness significant growth due to its innovative platform for creating bispecific antibodies with enhanced stability, potency, and dual-targeting capabilities. DART molecules efficiently redirect immune cells to target tumor cells, improving therapeutic efficacy and reducing off-target effects. Ongoing clinical trials and early approvals in oncology and immunology validate the platform’s potential. Strategic partnerships and licensing agreements expand global access and pipeline development. With increasing demand for next-generation bispecific therapies, the DART platform offers a reliable and scalable solution, positioning it as a leading technology in the global bispecific antibody market.

North America is projected to witness the highest growth in the bispecific antibody molecular drug market due to advanced healthcare infrastructure, high R&D investment, and early adoption of innovative biologics.

The region hosts leading pharmaceutical companies, biotech startups, and research institutions driving pipeline development and clinical trials. For instance, in January 2023, the FDA approved Genentech’s bispecific antibodies for lymphoma treatment, marking a significant milestone in North America’s bispecific antibody market. This approval validated the clinical efficacy and safety of bispecific therapies, accelerating adoption in oncology treatment protocols. It strengthened the region’s position as a leader in innovative biologics, encouraged further R&D investment, and enhanced market confidence. Consequently, it boosted demand for next-generation bispecific antibodies, driving growth and reinforcing North America’s dominance in the global bispecific antibody molecular drug market.

Rising cancer prevalence, favorable reimbursement policies, and strong regulatory support for breakthrough therapies further accelerate adoption. For instance, the American Cancer Society reported that, cancer incidence increased from around 805 cases per 100,000 in 1998 to 832 cases per 100,000 in 2021. The incidence rate for women younger than 50 has increased from 51% higher than men in 2002 to 82% higher in 2021. Rising cancer incidence, as reported by the American Cancer Society, highlights the growing demand for targeted therapies. The increasing prevalence, especially among younger women, is expected to drive the adoption and growth of bispecific antibody molecular drugs globally.

Technological advancements in antibody engineering, combined with robust funding and collaborations, enhance the region’s capacity to develop and commercialize bispecific antibodies. Consequently, North America remains a dominant hub for market growth and innovation in bispecific antibody therapeutics.

| Report Matrics | Details |

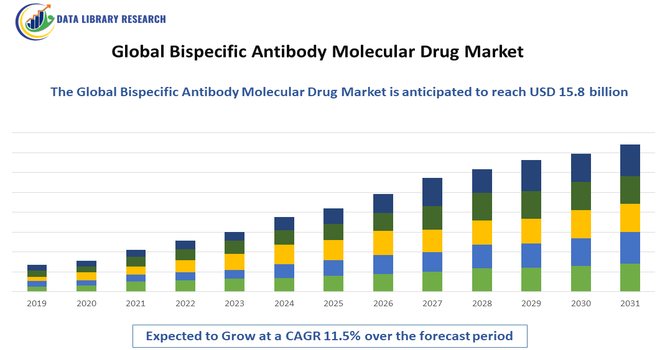

| Market Size Value | USD 15.8 billion |

| Growth Rate | CAGR of 11.5 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months' analysis support) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape features established pharmaceutical giants and agile biotech innovators developing diverse bispecific antibody platforms. Leading companies differentiate through proprietary technologies, extensive clinical pipelines, and strategic partnerships that enhance scale and market reach. Many firms focus on niche indications and novel mechanisms of action to gain competitive advantage. Licensing agreements, mergers, and acquisitions are common as larger players seek access to cutting edge platforms developed by smaller biotechs. Regulatory experience and manufacturing capabilities also influence competitive positioning, as biologics production demands high quality and scalability. Overall, competition revolves around clinical efficacy, safety profiles, and the ability to navigate complex regulatory environments efficiently.

The major players for above market:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the rising global prevalence of cancer and autoimmune diseases. Unlike standard antibodies that hit one target, bispecific antibodies can bind to two different targets at once—for example, grabbing a cancer cell and an immune cell simultaneously. This superior clinical effectiveness is fueling massive investment and regulatory approvals.

Q2. What are the main restraining factors for this market?

Growth is hindered by the extreme complexity and high cost of manufacturing these drugs. Designing a stable molecule that binds to two targets without falling apart is a significant technical challenge. Additionally, strict regulatory requirements and the potential for severe side effects, like cytokine release syndrome, can delay market entry.

Q3. Which segment is expected to witness high growth?

The Oncology segment is expected to witness the highest growth. Bispecific antibodies are proving to be game-changers in treating blood cancers and solid tumors that have become resistant to traditional therapies. Their ability to "redirect" the body’s own immune system to attack specific tumors makes them a dominant force in cancer research.

Q4. Who are the top major players for this market?

The market is led by global pharmaceutical giants with advanced biotechnology platforms. Key players include Amgen, Roche (Genentech), Johnson & Johnson (Janssen), and Regeneron Pharmaceuticals. These companies have successfully launched pioneering drugs like Blincyto and Hemlibra, setting the standard for the next generation of immunotherapy.

Q5. Which country is the largest player?

The United States is the largest player in this market. This dominance is due to its world-leading biotechnology research infrastructure, high healthcare spending, and the presence of major pharmaceutical headquarters. The U.S. FDA also provides specialized pathways that accelerate the approval of these breakthrough "orphan" and "fast-track" drugs.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model