Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Blood Alcohol Test Market includes devices and kits used to measure alcohol levels in the blood, helping monitor intoxication for medical, legal, or workplace purposes. It covers breathalyzers, enzymatic tests, and laboratory analyzers. Growth is driven by stricter DUI regulations, workplace safety initiatives, and increasing public awareness of alcohol-related health risks worldwide.

The growth of the global blood alcohol test market is driven by rising enforcement of drunk-driving laws, increasing workplace safety regulations, and growing public awareness of alcohol-related health risks. Technological advancements in rapid, accurate testing devices, the adoption of portable breathalyzers, and expanding use in hospitals, law enforcement, and rehabilitation centers further fuel market expansion globally.

The global blood alcohol test market is increasingly driven by demand for portable, rapid, and accurate testing devices. Advanced technologies such as fuel-cell sensors, infrared spectroscopy, and IoT-enabled breathalyzers are making testing faster and more reliable. Governments worldwide are enforcing stricter drunk-driving and workplace alcohol regulations, encouraging adoption across transportation, industrial, healthcare, and corporate sectors. Personal-use devices are also gaining popularity as consumers seek convenient self-monitoring tools.

Segmentation: The Global Blood Alcohol Test Market is Segmented by Product Type (Breathalyzers (Breath Testers), Consumable Products, and Blood Testing Devices (Kits & Reagents)), Technology (Fuel Cell Technology, Semiconductor Technology, Gas Chromatography, and Infrared Spectroscopy), End-User (Law Enforcement Agencies, Hospitals and Healthcare Facilities, Workplace Safety & Compliance, Personal Use/Individual Consumers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The primary drivers of the global blood alcohol test market is the enforcement of strict drunk-driving and traffic safety regulations worldwide. Governments are increasingly implementing zero-tolerance policies and mandatory alcohol testing for drivers to reduce road accidents and fatalities. Law enforcement agencies rely on accurate and portable blood alcohol testing devices to ensure compliance.

In April 2024, The Madras High Court noted that while surprise checks were ongoing, mandatory blood alcohol testing in accident cases was essential for accurately determining negligence in motor claims. This emphasis on stricter DUI enforcement strengthened regulatory support, increased demand for testing, and positively impacted growth in the global blood alcohol test market. This has led to higher demand for professional-grade breathalyzers and blood testing equipment. Public awareness campaigns highlighting the dangers of drunk driving have further strengthened adoption. As a result, regulatory pressure and safety concerns continue to expand the market steadily.

Another key driver is the growing focus on workplace safety and corporate alcohol policies. Companies in high-risk industries, such as transportation, construction, and manufacturing, are required to monitor employee alcohol levels to prevent accidents and ensure productivity. Organizations invest in blood and breath alcohol testing devices for regular screening and compliance with occupational safety regulations. Additionally, the rise of wellness initiatives encourages employees to monitor personal alcohol consumption. These factors have increased demand for both stationary and portable testing solutions. The combination of regulatory compliance and workplace safety awareness is therefore driving consistent growth in the global market.

Market Restraints:

A significant restraint in the global blood alcohol test market is the high cost and maintenance requirements of professional testing equipment. Advanced breathalyzers and blood testing devices can be expensive to purchase, calibrate, and maintain, which limits adoption, especially among small businesses and individual consumers. Ongoing expenses for calibration, consumables, and technical support add to the financial burden. In regions with limited budgets or lower regulatory enforcement, affordability becomes a barrier to widespread use. Consequently, high initial and operational costs restrict market penetration and slow adoption in price-sensitive markets, constraining overall growth despite rising awareness and demand.

Expansion of the blood alcohol test market has notable social and economic benefits. Widespread testing reduces alcohol-related accidents, injuries, and fatalities, lowering public health costs and economic losses associated with impaired driving and workplace incidents. Regulatory mandates and workplace safety policies drive investments in testing infrastructure, creating employment in manufacturing, distribution, and compliance services. At the individual level, accessible and affordable devices empower self-monitoring and responsible alcohol consumption. Overall, the market contributes to safer communities, increased public awareness of alcohol risks, and enhanced corporate responsibility, while stimulating growth in supporting industries and technology development.

Segmental Analysis:

The blood testing devices segment — including alcohol testing kits and reagents — is poised for strong growth as demand rises for reliable, lab grade assessments. These devices offer precise measurements beyond breath analysis, making them valuable in medical diagnostics, rehabilitation centers, and forensic labs. As institutions and hospitals push for higher accuracy in alcohol detection especially when breathalyzer results may be challenged — the need for blood based testing increases. This shift toward clinical-grade testing strengthens demand for kits and reagents, driving growth in this segment over the forecast period.

Fuel cell technology for alcohol testing is expected to dominate growth because of its superior accuracy, reliability, and consistency compared with older sensor types. Fuel cell breathalyzers show fewer false positives and maintain stability even under varying environmental conditions — which makes them the go-to choice for law enforcement, workplaces, and professional screening. As regulations tighten and demand rises for legally admissible, high-precision testing, fuel cell devices become preferred. Their reputation for dependable results is strengthening adoption, making the fuel cell segment a leading growth driver globally.

The hospitals and healthcare applications segment is forecast to see robust growth, as medical facilities increasingly employ alcohol testing for diagnostics, emergency care, addiction treatment, and patient monitoring. With growing awareness about alcohol related health risks, rehabilitation centers and clinics are investing in both breath and blood alcohol testing equipment. The expanded use in healthcare — beyond traffic enforcement or workplace safety — broadens the market base and adds a stable, recurring demand stream. As a result, the healthcare end use segment will emerge as one of the fastest growing in the industry.

The North America region is expected to maintain leadership and record the highest growth in the global alcohol testing market. This dominance stems from stringent drunk driving laws, proactive enforcement, widespread workplace safety regulations, and high public awareness about alcohol related risks. For instance, Following a 2021 California crash that killed nine, the NTSB recommended mandatory in-vehicle alcohol impairment detection and speed-limiting technologies. These measures aimed to prevent impaired driving fatalities, strengthen DUI enforcement, and drove increased adoption and demand for blood alcohol testing systems, positively impacting the U.S. market.

Advanced regulatory frameworks, strong institutional adoption, and robust healthcare infrastructure encourage frequent use of both breath and blood alcohol testing. Additionally, technology adoption is rapid, enabling fuel cell and modern testing solutions to proliferate. For instance, in September 2025, Cannabix Technologies received U.S. NHTSA approval for its BreathLogix “Workplace Series” alcohol breathalyzer, meeting USDOT specifications. The device provided rapid breath alcohol screening with real-time alerts, supporting workplace and road safety. This approval reinforced strict DUI enforcement and boosted demand, positively impacting the U.S. blood alcohol test market. Thus, these factors position North America as the largest and fastest-growing regional segment over the forecast period.

| Report Matrics | Details |

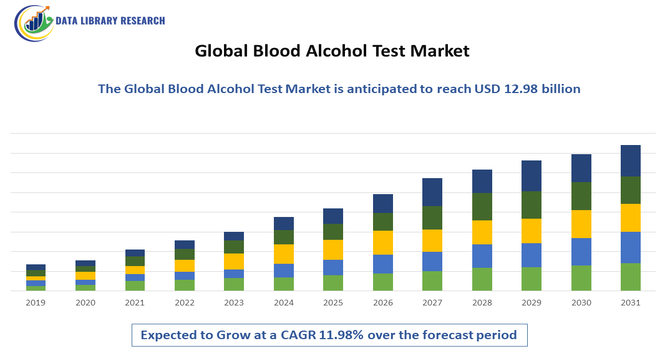

| Market Size Value | USD 12.98 billion |

| Growth Rate | CAGR of 11.98% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months' analysis support) |

| To Learn More About This Report | Request a Free Sample Copy |

The blood alcohol test market is moderately fragmented, with competition between established medical device manufacturers and specialized breathalyzer producers. Leading players focus on professional-grade devices with advanced sensors, regulatory approvals, and reliability. Simultaneously, new and regional entrants offer affordable yet accurate devices for personal and small-scale organizational use. Companies compete through innovation in accuracy, portability, ease of use, connectivity, and integration with digital platforms. Brand reputation, regulatory compliance, and product differentiation remain key competitive strategies. The market also sees collaboration with law enforcement, healthcare providers, and workplace programs to expand adoption, creating a dynamic environment for growth and technological advancement.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary drivers are the increasing number of stringent government regulations and laws targeting drunk driving globally. Furthermore, rising public awareness campaigns about road safety and the associated risks of impaired driving are boosting the adoption of testing devices by both law enforcement and private consumers.

Q2. What are the main restraining factors for this market?

Key restraining factors include the high initial cost of professional-grade testing instruments, which can limit adoption in developing economies. Additionally, challenges regarding the accuracy and reliability of some low-cost, handheld devices, as well as complex regulatory approval processes for new technology, can slow market expansion.

Q3. Which segment is expected to witness high growth?

The segment utilizing fuel cell technology is projected to show the fastest growth rate. These devices are highly favored for their superior accuracy and specificity, making them the standard choice for official use by law enforcement agencies worldwide. The demand for portable, highly reliable professional testers is increasing rapidly.

Q4. Who are the top major players for this market?

The market features several prominent global companies, including Drägerwerk AG & Co. KGaA, which is a major supplier of official breathalyzers, and large diagnostics firms like Abbott Laboratories and Quest Diagnostics. These companies offer a wide range of testing solutions for both law enforcement and healthcare settings.

Q5. Which country is the largest player?

North America, specifically the United States, holds the largest market share globally. This dominance is attributed to the strict enforcement of driving-under-the-influence (DUI) laws, mandatory workplace testing programs, and a high volume of traffic stops involving alcohol screening technology.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model