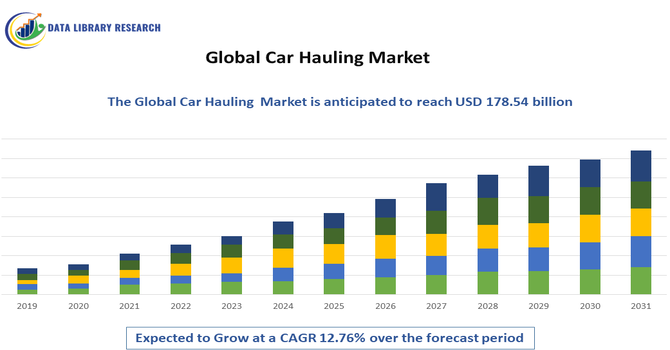

The Global Car Hauling Market size was estimated at USD 444.61 billion in 2026 and is projected to reach USD 178.54 billion by 2033, growing at a CAGR of 12.76% from 2026-2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Car Hauling Market refers to the industry that provides transportation of vehicles, including cars, SUVs, trucks, and motorcycles, between locations using specialized carriers, trailers, and logistics services. This market serves dealerships, auction houses, rental agencies, individual customers, and manufacturers needing safe, reliable movement of vehicles over long distances. Car hauling includes open and enclosed transport, door-to-door services, and terminal-to-terminal shipments. Growth is driven by rising vehicle sales, relocation trends, and e-commerce platforms for auto purchases. Efficient scheduling, tracking technologies, and regulatory compliance for safety and emissions are key to operations. Market players vary from large logistics firms to regional carriers focused on specific routes.

The Global Car Hauling Market is shaped by digital transformation, with online booking platforms, real-time tracking, and automated dispatch systems improving customer experience and operational transparency. There’s an increasing shift toward door-to-door services that reduce customer effort and improve delivery speed. Environmental sustainability trends are encouraging fleets to adopt fuel-efficient carriers and optimized route planning to lower carbon emissions. Partnerships between dealerships, auction sites, and logistics providers are becoming common to streamline supply chains. Additionally, demand for enclosed transport has risen among luxury and collector car segments. Emerging economies are witnessing higher cross-border hauling as vehicle ownership expands, strengthening global connectivity.

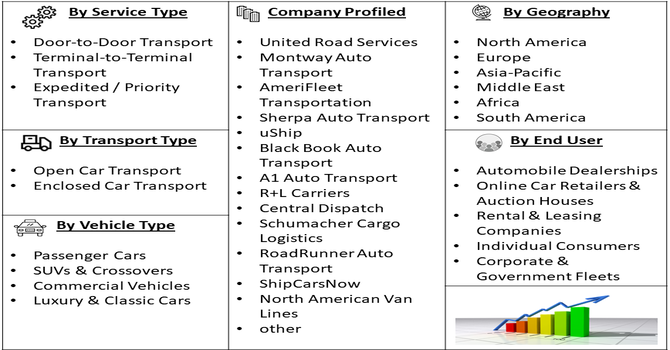

Segmentation: The Global Car Hauling Market is segmented by Transport Type (Open Car Transport and Enclosed Car Transport), Service Type (Door-to-Door Transport, Terminal-to-Terminal Transport and Expedited / Priority Transport), Vehicle Type (Passenger Cars, SUVs & Crossovers, Commercial Vehicles and Luxury & Classic Cars), End User (Automobile Dealerships, Online Car Retailers & Auction Houses, Rental & Leasing Companies, Individual Consumers and Corporate & Government Fleets), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The primary driver of the Global Car Hauling Market is the rapid increase in used vehicle and online car sales. As consumers increasingly purchase vehicles through digital marketplaces and auto auctions, demand for reliable long-distance transport surged. Online platforms often connect buyers and sellers across states or countries, requiring efficient hauling solutions to complete deliveries. Dealers and auction houses partner with car hauling providers to ensure timely, cost-effective movement of vehicles, minimizing delays and damage risk. This trend accelerated during the pandemic and remains strong as convenience and price transparency attract buyers. Consequently, more carriers have expanded capacity and technology to meet growing hauling needs.

Another key driver is the expansion of dealership and rental fleet networks that need frequent vehicle repositioning. As automotive markets grow, dealerships stock and distribute higher volumes of new and used vehicles across regions, relying on hauling services to balance inventory. Rental companies with multi-location operations require regular fleet transfers based on seasonal demand and customer usage patterns. This constant movement increases demand for scheduled and on-demand car hauling solutions. Additionally, global automotive manufacturers outsource transport to specialized carriers to maintain production-to-dealer flow. Increased fleet size and geographic dispersion of customers, dealers, and rental hubs collectively boost the need for professional hauling services worldwide.

Market Restraints

A significant restraint on the Global Car Hauling Market is the shortage of qualified drivers coupled with rising operational costs. Long-distance hauling requires skilled drivers with commercial licenses and experience, but many regions face workforce gaps due to aging drivers, lifestyle challenges, and competition from other logistics sectors. Recruiting and retaining drivers increases labor costs and limits capacity expansion. Rising fuel prices, insurance premiums, and maintenance costs for specialized carriers compound financial pressures. These factors reduce profit margins and may lead to higher customer prices. Regulatory constraints on work hours and emissions standards further strain operations, slowing growth relative to demand.

The Global Car Hauling Market significantly influences economic activity, employment, and mobility trends. It supports jobs in trucking, logistics management, dispatching, and vehicle maintenance, especially in transportation hubs and regional corridors. Reliable vehicle transport enables dealerships, rental companies, and online auto marketplaces to operate efficiently, expanding consumer access to vehicles across regions. Greater hauling capacity also benefits individuals relocating for work or education, fostering geographic mobility. However, heavy reliance on trucking increases infrastructure wear and traffic congestion. The industry contributes to carbon emissions, prompting investments in greener technologies and policy incentives to balance economic benefits with environmental and community impacts.

Segmental Analysis

The open car transport segment is expected to witness the highest growth over the forecast period due to its cost-effectiveness and wide industry acceptance. Most vehicles transported via car hauling services are not luxury or specialty models, making open transport the preferred choice for dealerships, rental companies, and individual customers. Open carriers can move multiple vehicles at once, improving efficiency and reducing per-unit costs. As online vehicle sales and long-distance relocations rise, demand for affordable transport increases, further driving this segment. Additionally, advancements in loading systems and route optimization have enhanced reliability and reduced delivery times, supporting rapid expansion in this segment.

The door-to-door transport segment is expected to witness the highest growth over the forecast period due to rising customer preference for convenience and seamless delivery. This service eliminates the need for customers to drop off or collect vehicles at terminals, saving time and reducing logistical hassles. As online car sales, auctions, and relocation needs increase, more consumers and businesses opt for direct pickup and delivery. Car haulers are investing in route planning and scheduling technology to improve accuracy and reduce delays, enhancing customer satisfaction. The convenience of door-to-door services has made it a popular choice for both individual buyers and fleet operators.

The commercial vehicles segment is expected to witness the highest growth over the forecast period due to increasing demand for efficient transportation in logistics, construction, and industrial sectors. As businesses expand operations and delivery networks, they require frequent movement of trucks, vans, and other commercial fleets between locations. Car hauling providers are increasingly offering specialized carriers and services to handle heavier and larger commercial vehicles safely. Additionally, growth in e-commerce and infrastructure development has accelerated fleet expansion, creating continuous hauling needs. This rising demand for commercial vehicle transport strengthens the segment’s growth potential and encourages service providers to expand capacity and route networks.

The automobile dealerships segment is expected to witness the highest growth over the forecast period due to expanding dealership networks and higher vehicle turnover. Dealerships require regular vehicle transfers between manufacturers, distribution centers, and showrooms to balance inventory and meet customer demand. As online car purchasing and multi-location dealership operations increase, the need for reliable hauling services grows. Dealerships prefer professional carriers that provide insured, trackable transport and timely delivery to avoid sales delays. Additionally, seasonal demand shifts and new model rollouts further drive frequent transportation requirements. This strong reliance on hauling services makes dealerships a major growth engine in the market.

The North American region is expected to witness the highest growth over the forecast period due to high vehicle ownership rates, strong automotive sales, and well-established logistics infrastructure. The region’s large geographic size and extensive highway network support long-distance vehicle transport, while high demand from dealerships, auctions, and rental companies fuels market expansion. The growing popularity of online vehicle purchases and auctions has further increased cross-state and cross-country transportation needs. Advanced digital booking and tracking systems are widely adopted, improving service efficiency and customer experience. Additionally, strong economic activity and rising fleet operations in logistics and mobility services reinforce North America’s leading growth outlook.

| Report Matrics | Details |

| Market Size Value | USD 178.54 billion |

| Growth Rate | CAGR of 12.76% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global Car Hauling Market includes large multinational logistics providers, regional carriers, and specialized auto transport companies. Major global firms leverage advanced tracking, optimized routing, and extensive terminal networks to serve high-volume clients like dealerships, auctions, and rental fleets. Regional players compete by offering tailored services, flexible scheduling, and localized expertise. Strategic partnerships and acquisitions are common as firms seek to expand routes and service capabilities. Technology innovation, such as telematics, mobile booking, and digital freight matching, enhances competitiveness. Differentiators include reliability, transit time, insurance coverage, and customer experience. Cost efficiency and compliance with safety and environmental regulations remain critical factors.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The expansion of e-commerce and online automotive marketplaces is a primary driver, as more consumers purchase vehicles remotely and require long-distance delivery. Additionally, the rebounding global automotive production and the rising demand for Electric Vehicles (EVs) necessitate specialized transport solutions, further boosting the volume of vehicles requiring professional hauling services.

Q2. What are the main restraining factors for this market?

High fuel price volatility and rising labor costs for specialized drivers act as significant restraints. The industry also faces strict regulatory hurdles regarding trailer weight limits and driver "hours of service" (HOS). Furthermore, the substantial capital investment required for modern hauling equipment and maintenance can limit the entry of smaller players.

Q3. Which segment is expected to witness high growth?

The Automobile Dealerships segment grew due to expanding dealership networks, rising vehicle sales, and higher inventory turnover. Online car purchases and multi-location operations increased demand for reliable transport, while seasonal shifts and new model launches required frequent vehicle transfers. Efficient, insured hauling services supported faster delivery and improved dealership logistics.

Q4. Who are the top major players for this market?

The market features prominent logistics giants such as Jack Cooper Transport, United Road Services, and Cassens Transport. Other significant players include Montway Auto Transport and CEVA Logistics. These companies differentiate themselves through advanced tracking technologies, expansive carrier networks, and specialized equipment designed to handle various vehicle sizes and weights efficiently.

Q5. Which country is the largest player?

The United States is the largest player in the car hauling market. Its leadership is sustained by a vast geography requiring long-haul logistics, a massive domestic automotive industry, and a high volume of used car sales across state lines. The presence of major auction houses and sophisticated logistics infrastructure further strengthens its position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model