Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Children’s Health Product Market is experiencing robust growth driven primarily by increasing awareness among parents regarding child nutrition, immunity, and overall well-being. Rising incidences of childhood malnutrition, vitamin deficiencies, and chronic health conditions have intensified demand for fortified foods, dietary supplements, probiotics, and immunity-boosting products. Additionally, growing disposable incomes, urbanization, and the influence of e-commerce platforms are expanding accessibility to health products targeted at children.

The Global Children’s Health Product Market is witnessing several key trends shaping its growth. There is a significant shift toward natural, organic, and plant-based formulations, as parents increasingly prefer products free from artificial additives, preservatives, and synthetic ingredients. Personalized nutrition is also gaining traction, with tailored supplements and fortified foods designed to meet specific age-related nutritional needs, such as immunity boosters, cognitive enhancers, and bone-strengthening products. Additionally, the rise of digital health platforms and e-commerce has made children’s health products more accessible, while brands are focusing on innovative, child-friendly formats like gummies, flavored powders, and fortified snacks to enhance compliance and appeal.

Segmentation: Global Children's Health Product Market is segmented By Product Type (Dietary Supplements, Fortified Foods & Beverages, Probiotics & Prebiotics, Immunity-Boosting Products), By Form (Tablets & Capsules, Powders & Sachets, Gummies & Chewables), By Age Group (Infants, Toddlers, Children, Adolescents), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Stores / E-commerce Platforms, Supermarkets & Hypermarkets), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Growing awareness among parents and caregivers about the importance of proper nutrition and immune health is a major driver for the children’s health product market. With rising concerns about childhood malnutrition, vitamin deficiencies, obesity, and lifestyle-related health issues, parents are proactively seeking products that support overall growth, immunity, and cognitive development. For instance, in January 2024, article published in Clinical and Experimental Pediatrics, reported that, according to the Comprehensive National Nutrition Survey, vitamin B12 deficiency affected 14% of preschool children (1–4 years), 17% of school-age children (5–9 years), and 31% of adolescents (10–19 years), highlighting the critical need for supplementation in at-risk populations.

The surge in health campaigns by governments, pediatricians, and non-profit organizations emphasizing preventive healthcare further motivates the adoption of dietary supplements, fortified foods, and immunity-boosting products for children. This trend is especially strong in urban and high-income households where parents prioritize wellness from an early age.

Rising disposable income, especially in emerging markets, has enabled families to spend more on premium children’s health products, including organic, fortified, and specialized nutritional supplements. At the same time, the proliferation of e-commerce platforms and online pharmacies has made these products more accessible, allowing parents to conveniently purchase a wide range of health-focused items tailored for children. The combination of affordability, accessibility, and convenience encourages higher adoption, enabling brands to reach a larger audience and introduce innovative, child-friendly products like flavored gummies, powders, and ready-to-drink supplements.

Market Restraints:

The children’s health product market is heavily regulated to ensure safety and efficacy, given the vulnerability of the target age group. Compliance with different regulations across countries—covering ingredient approvals, labeling requirements, permissible claims, and quality standards—can pose significant challenges for manufacturers, especially those operating in multiple regions. Delays in regulatory approvals, variability in international standards, and the risk of product recalls due to safety concerns may hinder product launches, increase operational costs, and restrict market expansion. These regulatory barriers act as a restraint, particularly for new entrants and smaller brands.

The global children’s health product market has significant socioeconomic impact by improving pediatric health outcomes and reducing disease burden among children. Widespread access to vaccines, nutritional supplements, and pediatric medications decreases morbidity and mortality, lowering healthcare costs and hospitalizations. Healthier children contribute to better school attendance, cognitive development, and long-term productivity, positively affecting societal growth. The market also generates employment in research, manufacturing, and distribution of pediatric products, fostering economic development. Additionally, government initiatives and NGO programs promoting child health amplify social equity, ensuring vulnerable populations access essential healthcare products, ultimately strengthening public health infrastructure and societal well-being worldwide.

Segmental Analysis:

Dietary supplements dominate the children’s health product market due to their ability to provide essential vitamins, minerals, and nutrients that support growth, immunity, and cognitive development. Parents increasingly rely on supplements to address nutrient deficiencies, picky eating habits, and specific health concerns in children. The availability of child-friendly formulations, including flavored chewables and gummies, enhances adoption and compliance, making dietary supplements a key contributor to market growth.

Gummies and chewables are gaining popularity as they combine convenience with taste, making it easier for children to consume supplements regularly. These formats improve adherence among children who may resist tablets or powders and are available across vitamins, minerals, and probiotics. Their fun shapes, flavors, and easy-to-administer nature are driving market adoption, particularly in urban and high-income households.

The toddler segment is growing rapidly as children in this age group require nutritional support for rapid physical and cognitive development. Parents are increasingly investing in targeted supplements, fortified foods, and immunity-boosting products to ensure toddlers meet developmental milestones and maintain overall health. This age group also responds well to innovative, child-friendly product formats, further fueling demand.

Online channels are witnessing significant growth due to convenience, wide product variety, and doorstep delivery. E-commerce platforms allow parents to compare products, read reviews, and purchase specialized children’s health products, including international and premium brands, which may not be easily available in retail outlets. The COVID-19 pandemic further accelerated the adoption of online shopping for health products globally.

North America is a leading market due to high consumer awareness, increasing healthcare expenditure, and preference for premium, organic, and fortified children’s health products.

The region also benefits from strong e-commerce infrastructure, proactive parental focus on preventive healthcare, and government initiatives promoting child nutrition, driving consistent growth in the market. For instance, December 2025, NUK, trusted for over 70 years, expanded its Perfect Match line in North America with three new products: the Air Pacifier, Learner Cup, and Straw Cup. Building on prior success, these innovations supported babies’ natural development, reinforcing NUK’s market leadership and driving growth in the region’s children’s health product market.

Similarly, in November 2025, the WHO released six target product profiles for child-friendly cancer medicines, guiding manufacturers in developing optimized pediatric formulations. By addressing dosing challenges and treatment risks, this initiative supported improved access and therapeutic outcomes, strengthening North America’s children’s health product market and encouraging innovation in pediatric oncology treatments.

Thus, North America’s strong market position is reinforced by rising consumer awareness, growing healthcare spending, and a shift toward premium, organic, and fortified children’s health products. These factors, combined with ongoing innovation and expanding e-commerce channels, are expected to sustain robust growth and shape the future of the region’s children’s health product market.

| Report Matrics | Details |

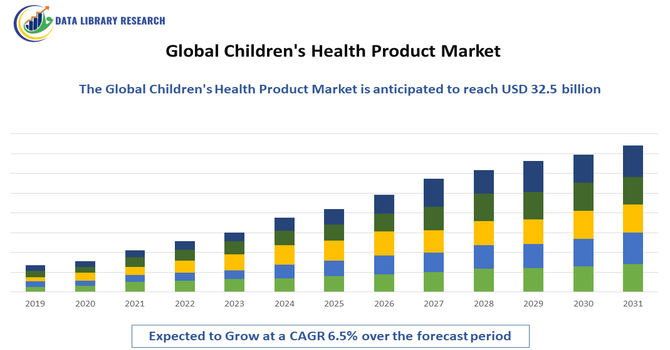

| Market Size Value | USD 32.5 billion |

| Growth Rate | CAGR of 6.5% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months' analysis support) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the global children’s health product market is shaped by a combination of large multinational nutrition and pharmaceutical firms, specialized pediatric supplement brands, and emerging startups focusing on organic, clean-label, and child friendly formulations. The competition centers on product formulation (immunity boosters, vitamins, probiotics), taste and format (gummies, chewables, syrups), regulatory compliance for safety in children, and effective branding and distribution across retail and online channels. Companies differentiate through innovations in ingredients, fortification levels, natural/organic positioning, and pan regional distribution networks to capture market share among parents seeking the best for child health and development.

Key Players:

Recent News

Q1. What are the main growth-driving factors for this market?

Growth is driven by increasing parental awareness about child nutrition, safety, and preventative care. Rising disposable incomes, especially in developing countries, allow families to spend more on high-quality and premium wellness products specifically designed for children.

Q2. What are the main restraining factors for this market?

The high cost of specialized pediatric products and treatments can restrict market growth, particularly in lower-income regions. Furthermore, stringent safety regulations and the widespread availability of cheaper, counterfeit, or low-quality products pose significant challenges to legitimate manufacturers.

Q3. Which segment is expected to witness high growth?

The online stores and e-commerce platforms segment is expected to witness the highest growth, driven by increasing consumer preference for convenient, home-delivered children’s health products, rising digital adoption, and the expansion of online pediatric product offerings worldwide.

Q4. Who are the top major players for this market?

Top market players include leading pharmaceutical and consumer goods corporations. Key companies are Nestlé S.A., Danone S.A., Abbott Laboratories, Reckitt Benckiser Group plc, and GlaxoSmithKline (GSK). These companies focus on pediatric nutrition and specialty care.

Q5. Which country is the largest player?

The United States holds the largest market share in the children's health sector, driving the North American region's dominance. This is attributed to its well-established, advanced healthcare system, high levels of per capita health expenditure, and rapid adoption of new medical technologies.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model