Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Clinical Immunoassays Market encompasses diagnostic tests that detect or measure specific proteins, hormones, or antibodies in patient samples to aid in disease diagnosis, monitoring, and treatment. These assays are widely used in hospitals, laboratories, and research centers for detecting infectious diseases, autoimmune disorders, cancer biomarkers, and hormonal imbalances. The market has grown significantly due to the rising prevalence of chronic diseases, increasing demand for early and accurate diagnostics, technological advancements in immunoassay platforms, and expanding healthcare infrastructure.

The global clinical immunoassays market has witnessed rapid adoption of high-throughput and automated platforms, improving accuracy, speed, and efficiency in diagnostic workflows. Emerging trends include the development of multiplex immunoassays capable of detecting multiple biomarkers simultaneously and integration with point-of-care testing devices for faster, decentralized diagnostics. Additionally, the incorporation of AI and machine learning into immunoassay analysis is enabling predictive diagnostics and personalized medicine.

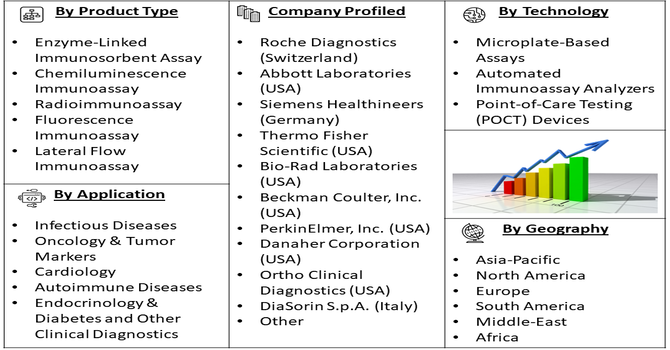

Segmentation: The Global Clinical Immunoassays Market is segmented by Product Type (Enzyme-Linked Immunosorbent Assay (ELISA), Chemiluminescence Immunoassay (CLIA), Radioimmunoassay (RIA), Fluorescence Immunoassay (FIA), and Lateral Flow Immunoassay (LFIA) / Rapid Tests), Technology (Microplate-Based Assays, Automated Immunoassay Analyzers and Point-of-Care Testing (POCT) Devices), Application (Infectious Diseases (HIV, Hepatitis, COVID-19, etc.), Oncology & Tumor Markers, Cardiology, Autoimmune Diseases, Endocrinology & Diabetes and Other Clinical Diagnostics), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The growing prevalence of chronic and infectious diseases globally has been a major driver for the clinical immunoassays market. Rising cases of HIV, hepatitis, COVID-19, and cancer have increased the demand for accurate, sensitive, and rapid diagnostic solutions. For instance, WHO reported that in 2021, noncommunicable diseases (NCDs) caused 43 million deaths, accounting for 75% of global non-pandemic fatalities. Among these, 18 million were premature deaths before age 70, with 82% occurring in low- and middle-income countries.

Immunoassays provide high specificity in detecting biomarkers, enabling early diagnosis, treatment monitoring, and personalized therapy. Additionally, the aging population, lifestyle-related disorders, and expanding awareness of preventive healthcare have further fueled market growth. Hospitals, diagnostic laboratories, and research centers increasingly adopt immunoassays due to their reliability and ability to support high-throughput testing, thereby accelerating market expansion.

Technological advancements and automation in immunoassay platforms have significantly propelled market growth. Innovations such as chemiluminescence, fluorescence, lateral flow assays, and fully automated analyzers have improved sensitivity, accuracy, and turnaround time. Integration with point-of-care testing (POCT) systems and digital health solutions has enhanced accessibility and efficiency, particularly in remote and resource-limited settings. Additionally, the adoption of multiplex immunoassays allows simultaneous detection of multiple analytes, reducing costs and time. The increasing focus of pharmaceutical and biotechnology companies on biomarker research and personalized medicine has also boosted demand, further expanding the global clinical immunoassays market.

Market Restraints:

High costs associated with advanced immunoassay instruments, reagents, and automated platforms have restrained market growth, particularly in low- and middle-income countries. Maintenance, calibration, and training requirements add to operational expenses, limiting adoption in smaller laboratories and healthcare facilities. Additionally, variability in test results due to sample quality, cross-reactivity, and handling errors can affect reliability and clinician confidence. Regulatory hurdles and lengthy approval processes for new assays further slow market penetration. Collectively, these challenges constrain widespread adoption, especially in developing regions, and may limit the pace of global clinical immunoassay market expansion despite rising demand.

The clinical immunoassays market is highly competitive and fragmented, dominated by key players such as Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Thermo Fisher Scientific, and Bio-Rad Laboratories. Companies are leveraging technological innovation, strategic partnerships, mergers, and acquisitions to expand their product portfolios and strengthen their global presence. Innovation in automated platforms, point-of-care solutions, and high-sensitivity immunoassays has become a critical differentiator. Regional expansion into emerging markets, where demand for diagnostics is growing, is also a key strategy. The competitive landscape emphasizes R&D investments, regulatory approvals, and collaborations with healthcare institutions to maintain leadership and capitalize on evolving market opportunities.

Segmental Analysis:

The Chemiluminescence Immunoassay (CLIA) segment was expected to witness the highest growth over the forecast period due to its superior sensitivity, specificity, and rapid turnaround times compared to traditional immunoassays. CLIA enabled accurate detection of low-abundance biomarkers, making it ideal for early disease diagnosis, monitoring, and research applications. Rising prevalence of chronic and infectious diseases, along with increasing adoption in clinical laboratories and research centers, further accelerated its uptake. Technological advancements, automation integration, and expanding applications in oncology, endocrinology, and infectious disease testing reinforced CLIA’s market dominance, driving investments and adoption across diagnostic facilities globally.

Automated immunoassay analyzers were projected to experience the highest growth over the forecast period due to their ability to deliver high-throughput, reproducible, and efficient testing. Automation minimized human error, reduced sample handling time, and enhanced laboratory workflow, supporting the increasing demand for rapid and accurate diagnostics. Rising prevalence of chronic and infectious diseases, coupled with the expansion of hospital laboratories and diagnostic centers, fueled adoption. Technological innovations in analyzer design, integration with laboratory information systems, and compatibility with multiple assay formats strengthened their market position. Automation adoption facilitated scalable diagnostics, cost efficiency, and improved patient outcomes, driving global market expansion.

The infectious diseases segment, including HIV, Hepatitis, and COVID-19, was expected to witness the highest growth over the forecast period due to rising global disease prevalence and the critical need for early detection and monitoring. Increased public health initiatives, government screening programs, and demand for reliable immunoassays accelerated market adoption. Laboratories and hospitals increasingly relied on advanced immunoassay platforms to detect emerging pathogens and manage disease outbreaks. Continuous technological innovations in assay sensitivity, specificity, and multiplexing further enhanced testing capabilities. Growing awareness, preventive strategies, and robust healthcare infrastructure investments contributed to the segment’s rapid expansion in both developed and emerging regions.

The North American market was expected to witness the highest growth over the forecast period, driven by advanced healthcare infrastructure, early adoption of innovative immunoassay technologies, and high healthcare expenditure. The presence of leading diagnostics companies, strong research and development activities, and favorable reimbursement policies accelerated the adoption of automated analyzers, chemiluminescence immunoassays, and infectious disease testing. For instance, iin July 2025, Siemens Healthineers earned My Green Lab ACT Ecolabel Certification for over 150 immunoassay and clinical chemistry reagents worldwide, becoming the first company to certify both reagents and analyzers in its Atellica portfolio. Certified assays include High-Sensitivity Troponin I for heart attack risk and ELF Test for fibrosis progression in MASH patients.

Increasing prevalence of chronic and infectious diseases, along with government-led screening programs, further supported growth. For instance, CDC reported that in the U.S., millions live with Hepatitis C (HCV), with estimates around 2.7-3.9 million chronic cases. Similarly, in 2025, Times of India reported that there have been at least 7.5 million illnesses, 81,000 hospitalizations and 3,100 deaths from flu so far this season in US.

Thus, rapid integration of artificial intelligence, data analytics, and connected laboratory systems enhanced efficiency and accuracy in diagnostics, positioning North America as the leading regional market for clinical immunoassays globally.

| Report Matrics | Details |

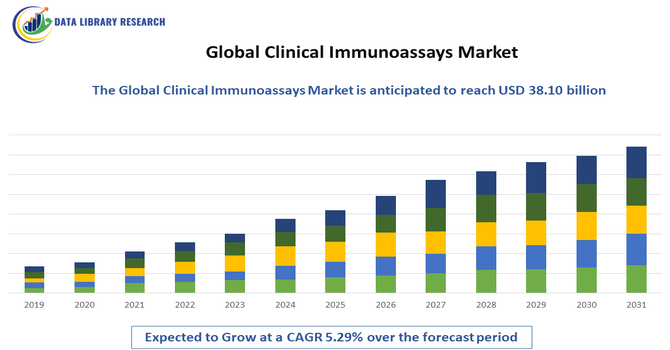

| Market Size Value | USD 38.10 billion |

| Growth Rate | CAGR of 5.29% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months' analysis support) |

| To Learn More About This Report | Request a Free Sample Copy |

Clinical immunoassays have substantially improved public health outcomes by enabling early and accurate detection of diseases such as cancer, infectious diseases, autoimmune disorders, and hormonal imbalances. Their adoption reduces healthcare costs by preventing disease progression and hospitalizations. Widespread availability of automated and point-of-care immunoassays has improved accessibility to diagnostics in underserved and remote regions. Furthermore, reliable immunoassays support research, vaccine development, and epidemiological monitoring, positively impacting societal health infrastructure. By enhancing patient outcomes, reducing treatment costs, and driving healthcare efficiency, clinical immunoassays contribute significantly to the socioeconomic well-being of populations worldwide.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the increasing prevalence of chronic and infectious diseases, such as cancer, heart disease, and hepatitis. As the global population ages, there is a higher demand for early and accurate diagnostic testing. Additionally, the shift toward automated laboratory systems and point-of-care testing is making immunoassays faster and more efficient.

Q2. What are the main restraining factors for this market?

Growth is limited by the high cost of advanced immunoassay instruments and the reagents needed to run them. Many laboratories in developing regions struggle with the significant initial investment required. Furthermore, strict regulatory requirements for new diagnostic tests and a shortage of skilled laboratory technicians to operate complex equipment can slow down adoption.

Q3. Which segment is expected to witness high growth?

The Chemiluminescence Immunoassays (CLIA) segment is expected to see the highest growth. This technology is highly popular because it offers superior sensitivity and accuracy compared to older methods. Its ability to detect very low levels of biomarkers makes it the preferred choice for hospitals and reference labs managing complex disease diagnostics.

Q4. Who are the top major players for this market?

The market is dominated by global leaders in medical diagnostics and laboratory science. Key players include Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Danaher Corporation (Beckman Coulter), and Thermo Fisher Scientific. These companies stay ahead by offering integrated, high-throughput systems that can process thousands of patient samples daily with extreme precision.

Q5. Which country is the largest player?

The United States is the largest player in the clinical immunoassays market. This is due to its highly advanced healthcare infrastructure, significant investment in medical research, and high per capita healthcare spending. The presence of world-leading diagnostic manufacturers and a strong emphasis on preventative health screening keep the U.S. in the lead.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model