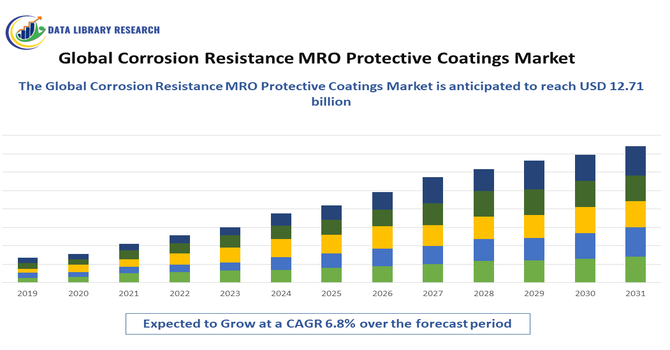

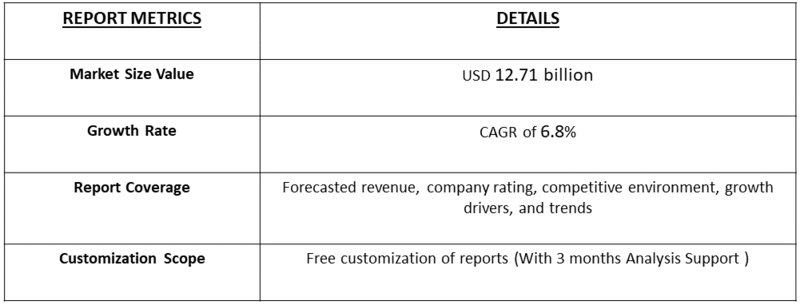

The Corrosion Resistance MRO Protective Coatings Market size is projected to reach USD 8.02 billion in 2025, growing at a CAGR of 6.8% during the forecast period, 2025-2032, reaching approximately USD 12.71 billion.

Get Complete Analysis Of The Report - Download Free Sample PDF

Corrosion resistance MRO (Maintenance, Repair, and Overhaul) protective coatings are specialized surface treatments designed to prevent or slow down the degradation of metals caused by environmental factors such as moisture, chemicals, salt, and oxidation. These coatings form a protective barrier that enhances the durability and lifespan of equipment, machinery, pipelines, and infrastructure exposed to harsh operating conditions. Widely used across industries like aerospace, automotive, marine, oil & gas, and construction, they help reduce maintenance costs, improve operational efficiency, and ensure safety and reliability. Advanced MRO coatings often incorporate technologies such as epoxy, polyurethane, and nanomaterials to deliver superior adhesion, chemical resistance, and long-term corrosion protection.

The corrosion resistance MRO protective coatings market is witnessing steady growth, driven by rising demand for asset protection and extended equipment life across industries such as aerospace, marine, oil & gas, automotive, and infrastructure. A key trend is the shift toward eco-friendly, low-VOC, and high-performance coatings that comply with stringent environmental regulations. Increasing adoption of nanotechnology and advanced polymers is enhancing coating durability, chemical resistance, and sustainability. Additionally, industries are investing in predictive maintenance and smart coatings with self-healing or anti-fouling properties to reduce downtime and repair costs. Growing infrastructure development in emerging economies and the need to protect aging assets in developed regions further fuel market expansion.

Segmentation:

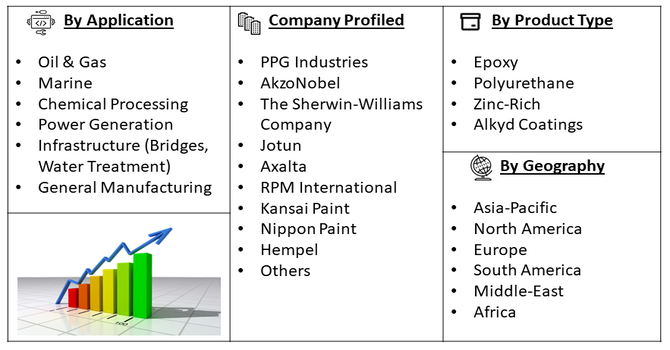

The Corrosion Resistance MRO Protective Coatings market is segmented primarily by Product Type (Epoxy, Polyurethane, Zinc-Rich, and Alkyd Coatings), Substrate (Encompassing Steel, Concrete, Aluminum, and Other Metals), End-Use Industry (Oil & Gas, Marine, Chemical Processing, Power Generation, Infrastructure (Bridges, Water Treatment), and General Manufacturing), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A significant driver for the corrosion resistance MRO protective coatings market is the growing emphasis on extending the lifecycle of industrial assets and optimizing their Total Cost of Ownership (TCO). Businesses are increasingly recognizing that proactive maintenance, including the application of high-performance protective coatings, is more cost-effective in the long run than dealing with the extensive repairs or premature replacement necessitated by corrosion. This shift in strategic thinking drives demand for durable coatings that minimize downtime, reduce maintenance frequency, and prevent catastrophic failures.

Industries across the board, from manufacturing to energy, are investing in coating solutions that offer superior protection, aligning with a broader corporate objective of operational efficiency and long-term financial sustainability. For instance, in 2021, DuPont expanded MOLYKOTE® Specialty Lubricants distribution in EMEA by extending its partnership with Antala Ltd. to the UK and Ireland. Previously limited to Spain and Portugal, this move increased access to advanced lubricants for automotive and industrial use. By strengthening maintenance solutions and asset protection, the expansion supported demand for corrosion resistance MRO protective coatings, as both product lines complement each other in extending equipment life, reducing downtime, and driving operational efficiency.

Continuous technological advancements in coating formulations and application methods are powerful drivers for the corrosion-resistant MRO protective coatings market. Innovations are leading to the development of coatings with enhanced properties such as faster curing times, improved adhesion to a wider range of substrates, superior resistance to specific chemicals and extreme temperatures, and better UV stability.

Furthermore, the introduction of more user-friendly application techniques, including high-pressure spray systems and self-leveling coatings, reduces labor costs and improves application quality. For instance, in April 2023, Vantage Performance Materials, a unit of Vantage Specialty Chemicals, showcased its latest aerospace innovations at MRO Americas 2023 in Atlanta. The company introduced LENIUM FS and LENIUM HT, advanced vapor degreasing solutions designed to replace hazardous solvents such as TCE, PERC, and nPB. These non-flammable, alloy- and plastic-compatible formulations addressed industry demand for safer, high-performance cleaning technologies. By enabling cleaner, more durable surfaces for treatment and coating, these solutions supported stronger adoption of corrosion resistance MRO protective coatings, driving growth in aerospace and defense maintenance markets.

Market Restraints:

A major restraint hindering market growth is the volatility in the prices of key raw materials, such as epoxy resins, polyurethane, titanium dioxide, and other specialty chemicals, which are often derived from petroleum. This price fluctuation creates significant uncertainty in production costs and profit margins for coating manufacturers, making budgeting difficult for end-users. Furthermore, the most effective, high-performance, and environmentally compliant coating systems come with a substantially higher initial cost compared to conventional alternatives. This high upfront investment can deter price-sensitive small and medium-sized enterprises and slow down adoption rates in developing regions, potentially restraining overall market expansion.

The corrosion resistance MRO protective coatings market plays a vital socio-economic role by safeguarding critical infrastructure, reducing repair costs, and ensuring safety in sectors like aerospace, oil & gas, marine, and construction, thereby supporting job creation and industrial sustainability.

Pre-COVID-19, steady industrial growth and infrastructure expansion fueled demand, while the pandemic temporarily slowed projects due to supply chain disruptions and reduced industrial activity. Post-COVID-19, the market rebounded strongly with renewed investments in infrastructure modernization, stricter safety regulations, and a rising focus on sustainable, eco-friendly coatings, reinforcing its importance in extending asset life and reducing long-term operational costs.

Segmental Analysis

The Epoxy product type segment is poised for significant growth in the corrosion resistance MRO protective coatings market. Epoxies are highly valued for their exceptional adhesion, chemical resistance, and mechanical strength, making them ideal for demanding environments. Their versatility allows for formulation into various types, including solvent-based, water-based, and high-solids coatings, catering to diverse application needs and regulatory requirements. The increasing need for durable, long-lasting protection across industries like oil & gas, chemical processing, and infrastructure, where harsh conditions are prevalent, is a key driver. Continuous advancements in epoxy resin technology, leading to improved performance and easier application, further bolster its market dominance and projected expansion.

The Steel Substrate segment is expected to experience substantial growth within the corrosion resistance MRO protective coatings market. Steel's widespread use across critical infrastructure, industrial equipment, automotive, and marine applications makes it highly susceptible to corrosion. Consequently, the demand for effective protective coatings for steel structures and components remains consistently high. The segment's growth is driven by ongoing infrastructure development, the need to maintain aging steel assets, and the industrial sector's focus on extending the service life of machinery and equipment. Advances in coating technologies specifically designed for steel, offering superior adhesion and robust protection against various corrosive elements, further fuel this segment's expansion.

The Power Generation end-user segment is projected for significant growth in the corrosion resistance MRO protective coatings market. Power plants, whether fossil fuel, nuclear, or renewable, house extensive steel and concrete infrastructure exposed to harsh operating conditions, including extreme temperatures, moisture, chemicals, and airborne contaminants. Protecting critical assets like turbines, boilers, pipelines, and cooling towers from corrosion is paramount for operational efficiency, safety, and longevity. The increasing global demand for energy, coupled with the ongoing maintenance and upgrading of existing power facilities, necessitates advanced MRO coatings. Furthermore, the expansion of renewable energy infrastructure, such as wind turbines and solar panel supports, also contributes to this segment's robust growth.

The Asia Pacific segment is anticipated to witness significant growth in the corrosion resistance MRO protective coatings market. This expansion is driven by rapid industrialization, substantial infrastructure development projects, and a burgeoning manufacturing sector across countries like China, India, and Southeast Asian nations. The increasing demand for durable protective coatings in industries such as automotive, marine, oil & gas, and construction, coupled with rising awareness of asset protection and maintenance, fuels market growth.

Favorable government initiatives promoting manufacturing and infrastructure, along with the presence of both multinational players and emerging local manufacturers, further solidify Asia Pacific's position as a key growth region. For instance, in May 2022, The Government of India, through the Department of Science and Technology (DST), supported this development via its autonomous R&D centre, ARCI. Scientists at the Centre for Engineered Coatings (CEC), ARCI, developed low-cost Fe-based intermetallic powders for corrosion-resistant coatings in high-temperature environments such as thermal power plants. Applied through detonation spray coating (DSC), the coatings delivered four times higher corrosion resistance than mild steel, significantly extending the life of components like turbine blades. This innovation enhanced operational efficiency and reduced maintenance costs, contributing directly to the growth of the corrosion resistance MRO protective coatings market by offering scalable, durable, and cost-effective solutions for critical industries.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape for Corrosion Resistance MRO Protective Coatings is characterized by a mix of large, multinational chemical companies and smaller, specialized regional players, all vying for market share by offering diverse product portfolios and technical expertise. Key strategies include product innovation focused on enhanced durability, faster curing times, and reduced environmental impact (e.g., low-VOC or water-based formulations). Companies are also leveraging strategic partnerships, mergers, and acquisitions to expand their geographical reach and product offerings, particularly in rapidly industrializing regions. Furthermore, a strong emphasis on customer service, including technical support for application and maintenance, and the development of customized solutions for specific industrial challenges, are critical differentiators in this highly competitive market.

Here are 10 major players in the corrosion resistance MRO protective coatings market:

Recent Developments:

Q1. What the main growth driving factors for this market?

The rising demand for maintenance, repair, and overhaul (MRO) services in the aviation and industrial sectors, coupled with the need for durable and corrosion-resistant coatings, are the primary growth drivers for the MRO protective coatings market.

Q2. What are the main restraining factors for this market?

The high cost of specialty coatings, stringent environmental regulations, and the availability of substitutes like paints and sealants pose challenges for the growth of the MRO protective coatings market.

Q3. Which segment is expected to witness high growth?

The aerospace segment is expected to witness the highest growth in the MRO protective coatings market, driven by the increasing demand for corrosion protection and surface enhancement of aircraft components.

Q4. Who are the top major players for this market?

The key players in the MRO protective coatings market include Akzo Nobel N.V., PPG Industries, Inc., Hempel A/S, Sherwin-Williams Company, and Jotun A/S.

Q5. Which country is the largest player?

The United States is the largest market for MRO protective coatings, owing to the presence of a well-developed aviation industry and the increasing maintenance and repair requirements in the country.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model