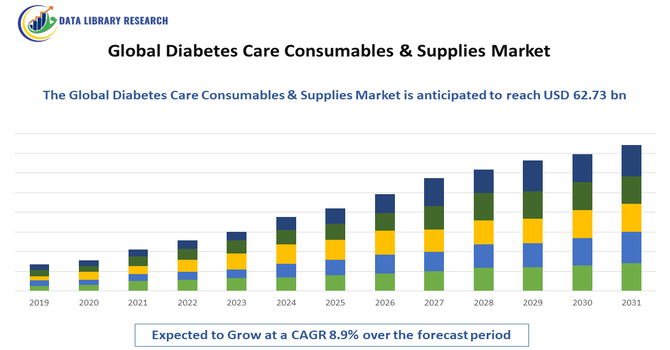

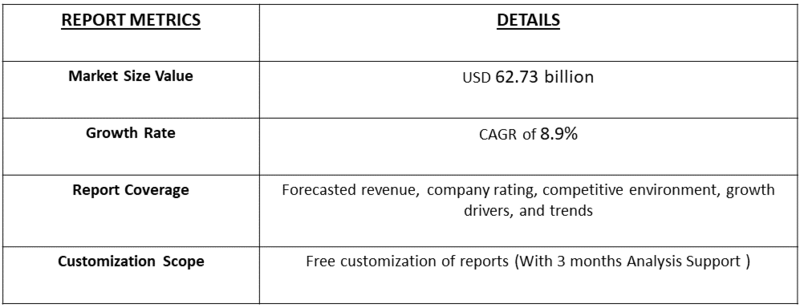

The Global Diabetes Care Consumables & Supplies Market is currently valued as USD 34.51 Billion and expected to reach to USD 62.73 Billion, expected to grow at the rate of 8.9% from 2025-2032.

Get Complete Analysis Of The Report - Download Free Sample PDF

The Global Diabetes Care Consumables & Supplies Market is experiencing steady growth, driven by the rising prevalence of diabetes worldwide, growing awareness of self-monitoring, and increasing demand for affordable and easy-to-use products. This market encompasses essential consumables such as test strips, lancets, syringes, pen needles, and insulin delivery supplies, which are critical for daily diabetes management. The surge in type 2 diabetes cases due to sedentary lifestyles, obesity, and aging populations has significantly fueled demand, particularly in emerging economies where awareness and screening initiatives are expanding. Moreover, advancements in product design aimed at improving patient comfort and accuracy, coupled with government initiatives and reimbursement support in developed regions, are further accelerating market growth. However, strong competition and pricing pressures on consumables remain key challenges shaping the market landscape.

The Global Diabetes Care Consumables & Supplies Market is being reshaped by rapid uptake of continuous glucose monitoring (CGM) technologies and smarter insulin-delivery accessories, with manufacturers shifting from one-off finger-stick supplies toward integrated, data-driven ecosystems. At the same time, the pen-needle and smart-pen segments are growing quickly as patients and payers prefer pen-based insulin delivery and digital dose-tracking, pushing pen-needle demand and prompting rapid product innovation. Remote monitoring and telehealth integration are increasing the value of connected consumables (cloud-linked CGMs, smart-pens) because clinicians can act on continuous data, which is accelerating adoption in health systems and RPM programs.

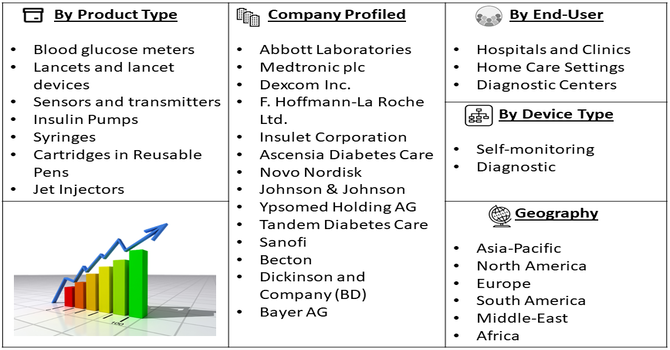

Segmentation: Global Diabetes Care Consumables & Supplies Market is segmented by Product Type (Blood glucose meters, Lancets and lancet devices, Sensors and transmitters, Insulin Pumps, Syringes, Cartridges in Reusable Pens, Jet Injectors), Device Type (Self-monitoring and Diagnostic), End-User (Hospitals and Clinics, Home Care Settings, Diagnostic Centers), Region (North America, Europe, Asia-Pacific, Latin America and Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing incidence of type 1 and type 2 diabetes worldwide is a primary driver for the demand for diabetes care consumables. For instance, the 2025 International Diabetes Federation (IDF) Diabetes Atlas, 11.1% of the global adult population aged 20–79—equivalent to 1 in 9 adults—is living with diabetes, with over 40% unaware they have the condition. More than 90% of these cases are type 2 diabetes, which is primarily driven by socio-economic, demographic, environmental, and genetic factors. The global diabetes burden is expected to rise sharply, with projections indicating that by 2050, approximately 1 in 8 adults—around 853 million people—will be living with diabetes, marking a 46% increase from current figures. Thus, the increasing number of diabetes population indicates that more patients require regular blood glucose monitoring, insulin delivery, and other related supplies, the need for reliable and accessible consumables, such as glucose meters, test strips, lancets, and insulin pens, continues to grow across home care, clinics, and hospitals.

Innovations such as continuous glucose monitoring (CGM) systems, smart insulin pens, and integrated digital platforms are enhancing patient compliance, real-time monitoring, and data-driven disease management. For instance, in August 2025, The FDA has cleared the first-ever glucose monitoring system for weight management, introduced by California startup Signos. This new system pairs a Dexcom glucose biosensor (which tracks blood sugar 24/7) with an AI-powered platform. This technology gives users personalized, real-time feedback on how their diet, exercise, and sleep affect their glucose levels, offering a novel approach to maintaining a healthy weight. The FDA's clearance of Signos' glucose monitoring system for weight management is expected to significantly expand the market for Global Diabetes Care Consumables & Supplies, particularly the Continuous Glucose Monitor (CGM) segment, by extending its use far beyond the traditional diabetic population.

Thus, these technological improvements are boosting the adoption of consumables that are compatible with advanced devices, creating recurring demand and supporting overall market growth.

Market Restraints:

The most immediate impact is the unaffordability for the vast majority of the population in LMICs. CGM sensors, for instance, can cost hundreds of dollars per month—a sum equivalent to several months' wages in many of these regions. This high-cost forces patients to rely on out-of-pocket payments, as national health insurance or public subsidies are often non-existent or inadequate for these premium devices. Consequently, many patients, particularly those with Type 1 Diabetes who require intensive management, are relegated to using older, less effective, and often painful fingerstick blood glucose monitoring (BGM), significantly increasing their risk of severe long-term complications like kidney failure, blindness, and cardiovascular disease.

The socioeconomic landscape profoundly dictates the dynamics of the Global Diabetes Care Consumables & Supplies Market, creating a stark dichotomy between high-income and low- and middle-income countries (LMICs). While the overall market is driven by the escalating global prevalence of diabetes, particularly in emerging economies, this growth is severely constrained by affordability and access barriers. In wealthy nations, robust insurance coverage and disposable income fuel the demand for premium, high-cost technologies like Continuous Glucose Monitors (CGMs) and smart insulin pens, leading to a focus on innovation and sophisticated product launches by manufacturers. Conversely, in LMICs, where the majority of the world's diabetic population resides, low per-capita income, minimal public health funding, and inadequate reimbursement policies render these advanced consumables prohibitively expensive; this financial constraint limits the market to basic, older products like simple blood glucose meters and vial-and-syringe insulin delivery, perpetuating a significant health inequity that stunts market penetration and results in poorer health outcomes for the world's most vulnerable patient populations.

Segmental Analysis:

The Insulin Delivery Devices segment of the Global Diabetes Care Consumables & Supplies Market is expected to witness the highest growth over the forecast period. This growth is driven by the rising prevalence of diabetes globally, increasing preference for patient-friendly and precise insulin administration methods, and the rapid adoption of smart insulin pens and insulin pumps that offer digital dose tracking and improved glycemic control. Additionally, ongoing innovations in pen-needle design, ease of use, and integration with continuous glucose monitoring (CGM) systems are further propelling demand in this segment, particularly in home care settings and developed markets where technological adoption is high.

The diagnostic segment is expected to witness the highest growth over the forecast period, driven by the rising global burden of chronic diseases such as diabetes, cardiovascular conditions, and cancer. Increasing awareness about early disease detection, along with advancements in diagnostic technologies, is fuelling demand for more accurate, accessible, and rapid testing methods. Additionally, the growing adoption of point-of-care testing, home diagnostics, and wearable health monitoring devices is making diagnostics more patient-friendly and efficient. Also, the governments and healthcare organizations are also investing heavily in screening programs and infrastructure development, further boosting this segment. As personalized medicine and preventive healthcare gain momentum, the diagnostic segment is becoming a cornerstone of modern healthcare, playing a critical role in improving outcomes through timely and precise diagnosis.

The home care settings segment is experiencing rapid expansion as more patients prefer self-management of diabetes outside hospital environments. Factors fueling this growth include the convenience of self-monitoring, availability of telehealth services, and rising adoption of user-friendly devices like CGMs, insulin pens, and portable meters. Home care demand also drives recurring consumables usage, making this segment highly attractive for manufacturers and suppliers.

In addition, the growing aging population and the increasing prevalence of type 2 diabetes are further contributing to the shift toward home-based care. Many patients, particularly the elderly and those in remote areas, benefit from the comfort and flexibility of managing their condition at home, reducing the need for frequent hospital visits. This trend is also supported by improved patient education and digital health platforms that enable real-time data sharing with healthcare providers. As healthcare systems continue to focus on cost-effectiveness and patient-centered care, home care settings are becoming an essential part of diabetes management. This evolving landscape presents significant opportunities for innovation in connected devices, remote monitoring tools, and personalized care solutions tailored for home

The North America region is expected to witness the highest growth in the Global Diabetes Care Consumables & Supplies Market over the forecast period. This growth is primarily driven by the region’s advanced healthcare infrastructure, high awareness of diabetes management, and rapid adoption of technologically advanced devices such as continuous glucose monitoring (CGM) systems, smart insulin pens, and insulin pumps. For instance, in April 2025, Abbott announced a groundbreaking agreement to integrate data from its Libre CGM systems directly into Epic’s electronic health record (EHR) systems in the U.S. This first-of-its-kind collaboration, facilitated through Epic’s Aura software, aims to streamline provider workflows by seamlessly connecting health systems with diagnostic labs and medical device data.This integration represents a major step forward in unifying real-time glucose monitoring with clinical decision-making, enhancing the diagnostic segment’s shift toward connected and data-driven care. It also strengthens the home care market by allowing patient-generated CGM data to flow directly into healthcare systems, enabling providers to monitor and adjust treatment plans remotely.

Additionally, supportive reimbursement policies, widespread availability of diabetes care products through retail and online pharmacies, and increasing focus on personalized and home-based diabetes management are contributing to the strong market expansion in North America. For instance, the recent update published by National Institute of Diabetes and Digestive and Kidney Diseases, reported that supportive reimbursement policies in the U.S., particularly under Medicare Part B, are designed to promote early detection and effective management of diabetes. Medicare provides coverage for essential preventive services such as diabetes screening, diabetes self-management training (DSMT), and the Annual Wellness Visit for beneficiaries who are at risk or have been diagnosed with prediabetes. These benefits not only encourage proactive care but also reduce the long-term burden of diabetes by supporting early intervention. @@@@ Thus, overall the presence of major global manufacturers and continuous product innovations further reinforce the region’s leading position in the market.

To Learn More About This Report - Request a Free Sample Copy

The Global Diabetes Care Consumables & Supplies Market is characterized by intense competition among leading multinational corporations and emerging innovators. These companies are engaged in continuous product development, strategic partnerships, and market expansion to cater to the growing demand for diabetes management solutions.

Recent Development:

Q1. What the main growth driving factors for this market?

The main growth drivers are the surging global prevalence of diabetes, propelled by aging populations, sedentary lifestyles, and rising obesity. This heightened disease burden is coupled with rapid technological advancements, especially in Continuous Glucose Monitoring (CGM) systems, smart insulin pens, and automated delivery. Favorable reimbursement policies, particularly in developed regions, also increase patient adoption of these advanced, high-value consumables.

Q2. What are the main restraining factors for this market?

The primary restraining factors are the high cost of advanced diabetes devices and consumables, which limits their adoption, particularly in low and middle-income countries. Additionally, inadequate reimbursement policies in many regions and a general lack of awareness regarding the benefits and proper use of newer technologies in remote or underdeveloped areas significantly restrict market growth potential.

Q3. Which segment is expected to witness high growth?

The Continuous Glucose Monitoring (CGM) and management devices segment is expected to witness the highest growth. Driven by increasing patient preference for less-invasive, real-time monitoring and the expansion of reimbursement coverage globally, CGM sensors and integrated automated insulin delivery systems are rapidly replacing traditional blood glucose testing supplies, thereby accelerating the segment's revenue growth.

Q4. Who are the top major players for this market?

The market is dominated by major medical technology and pharmaceutical corporations. The top major players include Abbott Laboratories (FreeStyle Libre), Medtronic (MiniMed systems), Dexcom (CGM devices), F. Hoffmann-La Roche (Accu-Chek), and Novo Nordisk (insulin and delivery devices), which collectively drive innovation and hold significant market share.

Q5. Which country is the largest player?

The United States, within the North American region, is the largest country market. This dominance is due to the high prevalence of diabetes, high healthcare expenditure per capita, a strong presence of key market players, and widespread insurance and government reimbursement coverage for advanced, high-value consumables like CGMs and insulin pump supplies.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model