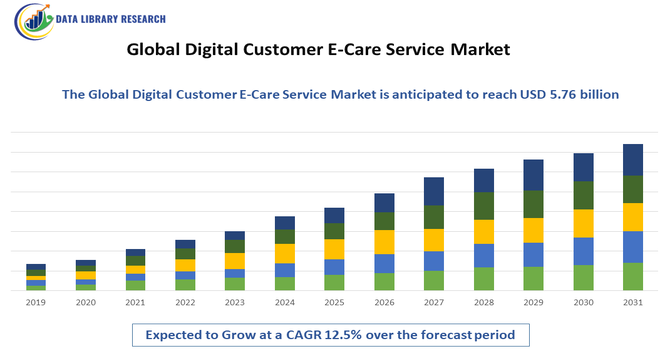

The Global Digital Customer E-Care Service Market size was valued at USD 2.26 billion in 2025 and is forecasted to grow at a CAGR of 12.5% from 2026 to 2033, reaching USD 5.76 billion in 2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Digital Customer E-Care Service Market refers to the worldwide industry of digital solutions designed to manage and enhance customer support through electronic channels, including chat, email, social media, voice, and self-service platforms. It encompasses software tools, platforms, and services that help businesses automate interactions, provide personalized assistance, and resolve inquiries efficiently across digital touch points. This market integrates advanced technologies such as artificial intelligence, machine learning, and analytics to improve response times, customer satisfaction, and loyalty. Digital e-care services support multiple industries including telecom, retail, banking, and healthcare, enabling companies to deliver seamless omnichannel experiences and strengthen customer engagement in an increasingly digital economy.

Major trends in the Global Digital Customer E-Care Service Market include the growing integration of AI and machine learning to power chatbots, virtual assistants, and predictive analytics that improve support efficiency and personalization. Omnichannel support strategies are expanding, enabling seamless customer interactions across voice, email, social media, and messaging apps. Cloud-based deployment solutions are gaining traction due to scalability and reduced infrastructure costs. Businesses are also focusing on proactive service models that anticipate customer needs through data insights. Digital automation and self-service portals are increasingly adopted to handle routine queries, while human agents focus on complex issues. This alignment of technology and customer expectations is reshaping service delivery globally.

Segmentation: The Global Digital Customer E Care Service Market is segmented by Service Type (Chat Support, Email Support, Social Media Support, Phone Support, and Self-Service Portals), End-User/Industry Vertical (Banking, Financial Services, and Insurance (BFSI), Telecommunications and IT, Retail and E-commerce, Healthcare, and Travel and Hospitality), Deployment Mode (Cloud-Based Solutions and On-Premises Solutions), Enterprise Size (Small and Medium Enterprises (SMEs) and Large Enterprises), Technology (Artificial Intelligence (AI) and Chatbots, Customer Relationship Management (CRM) Software, and Data Analytics Tools), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing consumer demand for seamless, omnichannel customer experiences. Customers expect fast, consistent, and personalized support across digital platforms such as live chat, social media, and mobile apps. Businesses across industries recognize customer satisfaction as a critical competitive differentiator and are investing in robust digital e care solutions to improve loyalty and retention.

The proliferation of smartphones and internet penetration fuels digital interaction, while rising expectations for instant service are reshaping support paradigms. Companies that implement flexible digital e care channels can quickly adapt to evolving customer needs, streamline operations, and build stronger relationships, driving sustained growth in this market.

The rapid technological advancements, especially in AI, machine learning, and cloud computing. These technologies enable intelligent automation, personalized interactions, and real-time problem resolution across customer touch points. AI-powered chatbots and virtual assistants reduce manual workload and enhance efficiency. For instance, in 2024, Siemens Healthineers’ local manufacturing of the Multix Impact E in India enhanced digital e-care services by improving timely diagnostics for conditions like TB, COPD, and trauma-related injuries. This move strengthened the Global Digital Customer E-Care Service Market, expanding access, support, and efficiency for healthcare providers and patients worldwide.

Cloud adoption provides scalable, flexible infrastructure that supports hybrid and remote service delivery models. Real-time analytics and data insights help companies better understand consumer behavior, enabling proactive support and tailored solutions. As businesses emphasize digital transformation to meet rising expectations for instant, personalized support, demand for sophisticated digital e care services continues to surge worldwide.

Market Restraints:

A restraint in the Global Digital Customer E Care Service Market is the growing concern over data privacy and security. As digital e care platforms collect and process vast quantities of personal customer data, ensuring confidentiality and compliance with global regulations (e.g., GDPR, CCPA) becomes complex and costly. Security breaches and data misuse risk damaging customer trust and brand reputation, disadvantaging smaller vendors lacking robust cybersecurity capabilities. Stricter regulatory standards require continuous investment in secure infrastructure, encrypted communication channels, and compliance frameworks. Balancing a seamless customer experience with stringent security measures challenges service providers and slows adoption in sensitive sectors like finance and healthcare, where data protection is paramount.

The Global Digital Customer E-Care Service Market significantly impacts economies and societies by improving service accessibility and customer satisfaction. Enhanced digital support reduces wait times, operational costs, and dependency on physical service centers, making customer care more inclusive and efficient. It enables small and medium enterprises to compete with larger firms by offering high-quality digital experiences. AI-driven automation drives job evolution, requiring new skills while improving workforce productivity. Better customer engagement fosters brand loyalty and drives revenue growth across industries. Additionally, digital e care services support remote populations, bridge geographic barriers, and contribute to business continuity during disruptions like pandemics, strengthening resilience in both developed and emerging markets.

Segmental Analysis:

The Social Media Support segment is projected to witness the highest growth as businesses increasingly leverage social platforms to engage with customers in real time. Rising consumer preference for instant responses on platforms like Facebook, Twitter, Instagram, and LinkedIn drives adoption of digital customer e-care services tailored for social interactions. Companies use AI-enabled monitoring and analytics to track sentiment, resolve complaints, and provide personalized support, enhancing brand reputation. Social media support reduces call center loads and improves customer engagement metrics, making it a strategic priority across industries. Its scalability and global reach ensure continued growth in the forecast period.

The BFSI segment is expected to record significant growth due to the increasing complexity of financial products, regulatory requirements, and the need for high-quality customer support. Financial institutions rely on digital e-care solutions to provide 24/7 assistance, fraud monitoring, account management, and policy inquiries, enhancing customer trust and retention. Integration of AI, predictive analytics, and omnichannel support enables personalized service, faster query resolution, and compliance with stringent regulations. With growing fintech adoption, mobile banking, and digital insurance platforms, BFSI providers increasingly invest in scalable digital customer e-care infrastructure, driving robust demand for advanced service solutions during the forecast period.

The Cloud-Based Solutions segment is poised for high growth as organizations seek scalable, flexible, and cost-effective platforms for digital customer e-care. Cloud deployment allows companies to manage multiple channels, streamline workflows, and integrate AI-powered automation without heavy IT infrastructure investment. Remote workforce enablement, real-time updates, and enhanced data analytics improve service efficiency and customer satisfaction. Businesses increasingly prefer cloud solutions to quickly adapt to changing customer expectations, ensure business continuity, and facilitate omnichannel support. Security, compliance, and rapid deployment capabilities make cloud-based e-care platforms an essential growth driver in industries ranging from retail to BFSI globally.

The SMEs segment is projected to witness the highest growth as small and medium businesses increasingly adopt digital customer e-care services to enhance competitiveness and customer engagement. Limited in-house resources, rising customer expectations, and the need for cost-efficient support drive SMEs toward automated, cloud-based, and AI-enabled solutions. These platforms allow SMEs to deliver omnichannel support, monitor customer sentiment, and scale operations without significant infrastructure investment. Flexible subscription-based pricing, ease of implementation, and integration with existing business tools make digital e-care solutions highly attractive for SMEs, boosting adoption rates and overall market growth during the forecast period.

The AI and Chatbots segment is expected to witness the highest growth due to increasing demand for automation, 24/7 support, and personalized customer interactions. AI-powered chatbots and virtual assistants can handle routine queries, provide recommendations, and escalate complex issues to human agents, enhancing operational efficiency. Advanced natural language processing, machine learning algorithms, and predictive analytics enable proactive support and sentiment analysis. Businesses across BFSI, retail, healthcare, and telecom increasingly integrate AI-driven e-care platforms to reduce costs, improve response times, and boost customer satisfaction. The ability to scale rapidly and deliver consistent service worldwide makes AI and chatbots a key growth driver.

The North American region is expected to witness the highest growth in the digital customer e-care service market due to advanced technological infrastructure, high internet penetration, and widespread adoption of AI, cloud, and omnichannel support systems.

Businesses prioritize enhancing customer experience through social media, chatbots, and cloud-based platforms, while BFSI, retail, and healthcare sectors lead digital transformation initiatives. For instance, in 2024, Eli Lilly launched LillyDirect, a digital healthcare platform providing disease management, tailored support, and home delivery of medications for obesity, migraine, and diabetes patients. This initiative enhanced patient convenience, improved engagement, and reinforced demand for Digital Customer E-Care Services by demonstrating the effectiveness of integrated, personalized digital support in managing chronic conditions.

Stringent regulatory frameworks, growing demand for 24/7 service, and increasing smartphone adoption further accelerate market expansion. Additionally, strong investments from key players, focus on customer engagement analytics, and rising consumer expectations make North America the most lucrative region for digital e-care services during the forecast period.

| Report Matrics | Details |

| Market Size Value | USD 5.76 billion |

| Growth Rate | CAGR of 12.5% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global Digital Customer E-Care Service Market is characterized by major technology providers, CRM platforms, and specialized customer support vendors continually innovating to capture market share. Key players deliver platforms that combine AI, analytics, and omnichannel capabilities for seamless customer engagement. Enterprises increasingly integrate advanced digital tools to differentiate service quality and improve customer experience. Competitive strategies include forming strategic partnerships, enhancing AI support capabilities, expanding cloud offerings, and strengthening global footprints.

The major players for this market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary growth drivers include the rapid adoption of AI-powered chatbots and machine learning, which enhance response times and personalization. Increased smartphone penetration and the shift toward omnichannel support allow businesses to engage customers on social media and messaging apps, meeting the rising consumer demand for instant, 24/7 digital support.

Q2. What are the main restraining factors for this market?

Data privacy concerns and stringent regulations, such as GDPR, pose significant challenges to market expansion. The high initial cost of implementing advanced AI infrastructure can deter small businesses. Furthermore, the "human touch" remains difficult to replicate digitally, leading to customer frustration when automated systems fail to resolve complex emotional issues.

Q3. Which segment is expected to witness high growth?

The Financial Services and Insurance (BFSI) sector experienced growth driven by digital transformation, increasing adoption of AI and analytics for risk assessment, and expanding mobile and online banking platforms. Rising demand for personalized financial products, regulatory compliance solutions, and cybersecurity enhancements further fueled market expansion, while greater financial inclusion and fintech collaborations accelerated innovation and customer engagement across banking and insurance services globally.

Q4. Who are the top major players for this market?

The market is dominated by global technology and consulting giants including Salesforce, Oracle Corporation, and SAP SE. Other significant players include Zendesk, Microsoft, and specialized service providers like Teleperformance and TTEC. These companies lead through continuous innovation in cloud-based CRM platforms and integrated AI tools for seamless customer interactions.

Q5. Which country is the largest player?

The United States is currently the largest player in the Global Digital Customer E-Care Service Market. This leadership is sustained by the presence of major tech innovators, early adoption of AI technologies, and a high concentration of multinational corporations that prioritize digital transformation to manage their extensive global customer bases.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model