Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Electric Micro Bus Market refers to the worldwide industry involved in the design, manufacture, and sale of compact, fully electric buses used for urban transport, shuttle services, and last-mile connectivity. These vehicles offer zero-emission mobility, lower operational costs, and reduced noise pollution. Market growth is driven by rising urbanization, government policies promoting sustainable transport, increasing demand for public electric mobility, and advancements in battery technology and electric drivetrains.

The global electric micro bus market is witnessing rapid growth due to increasing urbanization, rising traffic congestion, and growing environmental awareness. Cities are adopting electric microbuses for last-mile connectivity, reducing carbon emissions and noise pollution. Technological advancements in battery efficiency, fast charging infrastructure, and lightweight materials enhance vehicle performance and cost-effectiveness. Government incentives, subsidies, and stricter emission regulations further encourage adoption.

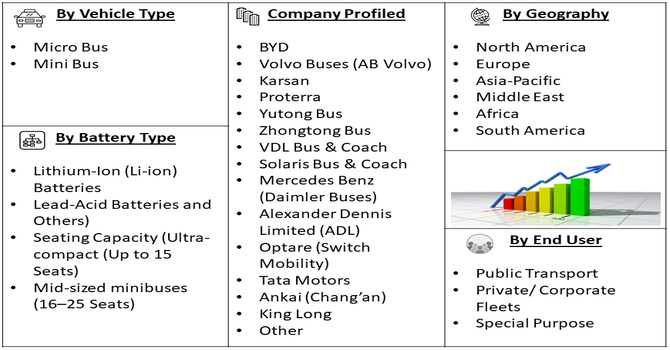

Segmentation: The Global Electric Micro Bus Market is segmented by Vehicle Type (Micro Bus, and Mini Bus), Battery Type (Lithium-Ion (Li-ion) Batteries, Lead-Acid Batteries and Others), Seating Capacity (Ultra-compact (Up to 15 Seats), and Mid-sized minibuses (16–25 Seats)), End-Use (Public Transport, Private/ Corporate Fleets and Special Purpose), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Government initiatives promoting clean energy and sustainable transportation are key drivers for the electric micro bus market. Subsidies, tax incentives, and grants encourage fleet operators and municipalities to adopt electric microbuses, reducing reliance on diesel-powered vehicles. Regulatory pressure to meet emission reduction targets and comply with stringent environmental norms further accelerates adoption. Investments in charging infrastructure and smart city projects create a favorable environment for electric microbuses. These policies not only reduce operational costs for operators but also drive public acceptance of eco-friendly transport, significantly contributing to the market’s global growth trajectory.

Rapid urbanization and increasing population density in cities are driving demand for compact, energy-efficient electric microbuses. These vehicles offer flexible last-mile connectivity, reduce traffic congestion, and provide an eco-friendly alternative to conventional buses and taxis. Growing awareness of environmental sustainability and rising fuel costs further encourage adoption.

In May 2025, GreenCell Mobility reached a milestone by securing an order for over 1,200 electric buses under the PM E-Bus Sewa Scheme to strengthen India’s electric public transport network. The initiative aims to transform urban mobility by providing sustainable, zero-emission transportation solutions and promoting cleaner, eco-friendly city commuting. Fleet operators and private enterprises, including hotels and corporate campuses, are increasingly opting for electric microbuses for shuttles and short-route services. Technological advancements in battery range, fast charging, and vehicle design enhance convenience and performance, boosting market adoption globally and supporting long-term growth of electric urban mobility solutions.

Market Restraints:

The high upfront cost of electric microbuses and associated charging infrastructure poses a significant restraint to market growth. Battery systems, advanced drivetrains, and vehicle electronics make these buses more expensive than traditional diesel counterparts. Limited public charging networks and inadequate fast-charging facilities in some regions hinder fleet adoption, particularly in emerging markets. Maintenance and replacement costs for batteries and specialized components add to operational expenses. Additionally, lack of standardized infrastructure and support for electric fleets can delay deployment. These economic and logistical challenges restrict widespread adoption, slowing the global growth of the electric micro bus market despite increasing demand for sustainable urban mobility.

Electric microbuses significantly influence socioeconomic dynamics by promoting sustainable urban transport and reducing greenhouse gas emissions. Lower operational and maintenance costs compared to conventional diesel buses create economic benefits for fleet operators. Enhanced accessibility improves mobility for urban populations, particularly in densely populated cities. Job creation occurs in vehicle manufacturing, battery production, and charging infrastructure deployment. The shift toward electric fleets supports public health by reducing air pollution and noise, while stimulating investment in clean energy solutions. Thus, electric microbuses contribute to environmental sustainability, cost-efficient transportation, and improved quality of urban life, reflecting a positive socioeconomic impact globally.

Segmental Analysis:

The Mini Bus segment is projected to witness the highest growth due to rising demand for compact and efficient transport solutions in urban areas, tourism, and corporate shuttle services. Mini buses offer flexibility, lower operational costs, and suitability for narrow city roads compared to larger buses. Their ability to provide last-mile connectivity and environmentally friendly mobility aligns with increasing urbanization and sustainability initiatives. Advancements in electric drivetrains, battery range, and vehicle safety features make mini buses an attractive choice for fleet operators, driving significant adoption across public and private transportation networks globally.

The Lead-Acid Batteries segment is expected to grow steadily due to their cost-effectiveness, reliability, and established technology. While lithium-ion batteries dominate high-performance applications, lead-acid batteries remain popular in budget-conscious fleets and emerging markets where affordability is critical. These batteries are simpler to maintain, widely available, and support moderate-range electric microbuses for city and last-mile operations. Operators seeking low-cost entry into electric mobility prefer lead-acid solutions, particularly for private, corporate, and municipal fleets. This widespread adoption positions lead-acid battery-powered electric microbuses as a key segment driving market growth in regions prioritizing cost efficiency over advanced performance.

The 16–25 seat mid-sized minibus segment is projected to experience the highest growth as it balances capacity and efficiency for urban and intercity routes. These minibuses cater to corporate fleets, airport shuttles, and public transport, offering cost-effective, low-emission alternatives to larger buses. Their size enables maneuverability in congested urban roads while maintaining adequate passenger capacity. Electrification of mid-sized minibuses reduces fuel costs and supports environmental goals. Technological advancements in battery range, fast charging, and safety systems further enhance their appeal, driving adoption among fleet operators globally and contributing significantly to market growth.

The Private/Corporate Fleets segment is expected to see substantial growth due to increasing adoption of electric microbuses for employee shuttles, airport transfers, and tourism services. Companies are prioritizing sustainability, cost reduction, and enhanced employee experience, making electric minibuses an attractive solution. Lower operational costs, reduced emissions, and quiet operation align with corporate ESG initiatives. Technological improvements in range, charging speed, and fleet management systems enable efficient deployment. Expanding awareness of eco-friendly mobility and supportive government incentives further encourage corporate adoption, making this segment a key contributor to the growth of the global electric micro bus market.

The Asia-Pacific region is projected to lead the global electric micro bus market due to rapid urbanization, rising population density, and increasing investment in sustainable public transport. Countries such as China, India, Japan, and South Korea are expanding EV infrastructure, offering subsidies, and implementing stringent emission regulations to promote adoption. For instance, In December 2023, Turkish manufacturer Karsan introduced its e-JEST electric minibus in Japan. Originally launched in Europe in 2018, the e-JEST expanded to the U.S. and Canada as the first electric minibus in those markets. The vehicle supports global adoption of compact, sustainable urban mobility solutions.

Simialrly, in March 2024, Volvo Buses launched the Volvo 8900 Electric, a low-entry electric bus for intercity, commuter, and city operations. Available in two- and three-axle configurations, it enables fleet operators to enhance efficiency, sustainability, and profitability while addressing growing demand for environmentally friendly public transportation solutions.

Growing demand for last-mile connectivity, tourism shuttles, and corporate transport solutions drives fleet operators to adopt electric microbuses. Local manufacturers and international collaborations are increasing production capabilities and technological advancements. Consequently, Asia-Pacific is expected to witness the highest growth during the forecast period, becoming a dominant market globally.

| Report Matrics | Details |

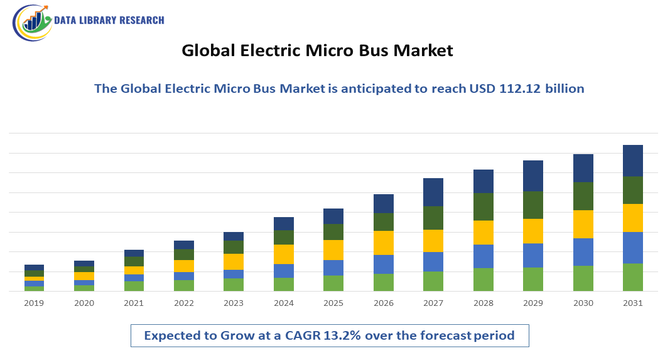

| Market Size Value | USD 88.56 billion |

| Growth Rate | CAGR of 13.2 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months' analysis support) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the global electric microbus market is increasingly dynamic, with manufacturers focusing on innovation, technology integration, and strategic partnerships. Key players include BYD, Proterra, ADL (Alexander Dennis Limited), Yutong, Zhongtong Bus, and VDL Bus & Coach, among others. Companies compete through product differentiation, battery efficiency, vehicle range, and charging infrastructure compatibility. Mergers, collaborations with city transport authorities, and government-backed pilot programs enhance market presence. R&D investments focus on lightweight designs, extended range, and smart fleet management solutions. Price competitiveness, after-sales support, and sustainability commitments are critical factors shaping the global electric microbus market.

The major players for the above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is driven by global efforts to reduce urban air pollution and meet carbon neutrality goals. Governments are offering generous subsidies and "green" incentives for cities to replace diesel fleets. Additionally, the rising demand for efficient "last-mile" connectivity between train stations and residential areas makes these smaller, agile electric buses a perfect solution for modern smart cities.

Q2. What are the main restraining factors for this market?

Growth is limited by the high upfront cost of electric vehicles and the expensive infrastructure required for high-speed charging stations. Limited battery range can also be a concern for longer routes or hilly terrain. Furthermore, the global shortage of lithium and other battery minerals can lead to manufacturing delays and unpredictable pricing for smaller bus manufacturers.

Q3. Which segment is expected to witness high growth?

The Autonomous Electric Micro Bus segment is expected to see the highest growth. These self-driving shuttles are being tested in airports, university campuses, and gated communities to move small groups of people without the need for a driver. Their ability to operate on fixed loops 24/7 makes them highly cost-effective and technologically attractive for future transit.

Q4. Who are the top major players for this market?

The market is led by specialized electric vehicle manufacturers and traditional bus giants. Key players include BYD, Yutong, Proterra, Navya, and Local Motors (Olli). These companies dominate by developing modular platforms that can be customized for different seating capacities while integrating advanced battery management systems to maximize the vehicle's daily operational range.

Q5. Which country is the largest player?

China is the largest player in the electric micro bus market. It has the world's most aggressive electrification policy and is home to the largest manufacturers, such as BYD and Yutong. With massive government-led initiatives to electrify public transit in every major city, China accounts for the vast majority of global production and domestic bus deployment.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model