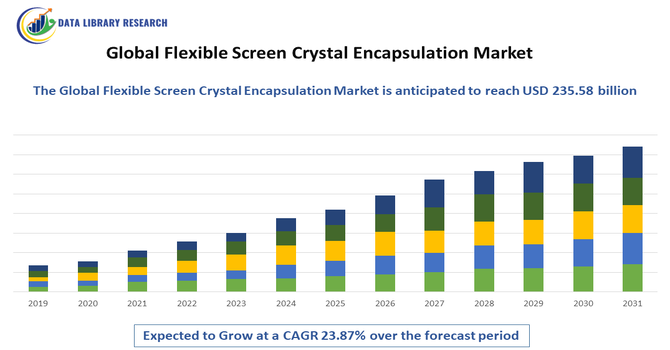

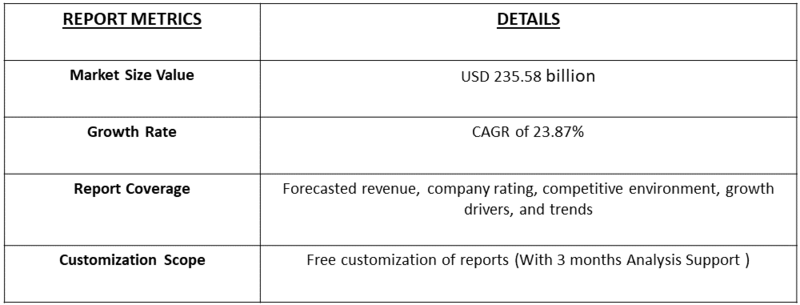

The Global Flexible Screen Crystal Encapsulation Market is approximately USD valued at 29.28 billion in the year 2025, and approximately to reach USD 235.58 billion in the year 2032, growing with a CAGR of 23.87% over the forecast period.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Flexible Screen Crystal Encapsulation Market refers to the industry focused on the development, production, and commercialization of encapsulation materials and technologies used to protect flexible display screens—such as those found in foldable smartphones, wearable devices, and flexible OLED panels—from environmental damage like moisture, oxygen, and mechanical stress. This market encompasses innovations in thin-film encapsulation (TFE), hybrid encapsulation, and barrier coatings that ensure the durability and performance of flexible screens, driven by growing demand in consumer electronics, automotive displays, and emerging tech applications across global markets.

The Global Flexible Screen Crystal Encapsulation Market is witnessing significant trends driven by rapid advancements in display technology and growing adoption of flexible OLED panels across consumer electronics. Key trends include increased use of thin-film encapsulation (TFE) for ultra-thin and lightweight devices, rising integration of hybrid encapsulation methods for improved durability, and a surge in demand for foldable smartphones and wearables. Additionally, manufacturers are focusing on eco-friendly materials, enhanced barrier performance, and scalability of production processes to meet growing global demand, particularly in the Asia-Pacific and North America.

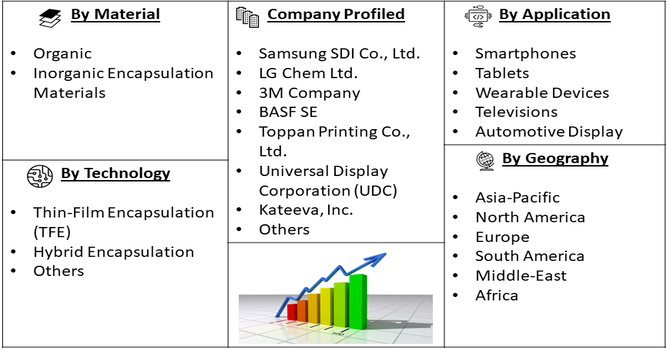

Segmentation: The Global Flexible Screen Crystal Encapsulation Market is segmented based by Material (Organic and Inorganic Encapsulation Materials), Technology (Thin-Film Encapsulation (TFE), Hybrid Encapsulation, and Others), Application (Smartphones, Tablets, Wearable Devices, Televisions, and Automotive Display) and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The major driver of the flexible screen crystal encapsulation market is the growing global demand for flexible, foldable, and rollable electronic devices, particularly smartphones and wearables. Consumers are increasingly drawn to innovative form factors that offer portability without compromising screen size or performance. This trend has pushed manufacturers to adopt flexible OLED technology, which requires high-performance encapsulation to protect delicate components from moisture, dust, and oxygen exposure. Foldable smartphones from brands like Samsung, Huawei, and Motorola have already demonstrated strong market traction, accelerating investment in encapsulation solutions. As product lifespans and durability become more critical to consumers, effective encapsulation becomes essential, further driving demand for advanced materials and technologies in this evolving electronics landscape.

Another key driver for this market is the technological progress in OLED displays and thin-film encapsulation (TFE) techniques. OLEDs are thinner, more energy-efficient, and offer better contrast and flexibility than traditional LCDs. However, their sensitivity to moisture and oxygen necessitates highly effective encapsulation solutions. Thin-film encapsulation, in particular, has emerged as a preferred method because it enables ultra-slim, lightweight, and flexible devices without sacrificing protection. Innovations in atomic layer deposition (ALD), inkjet printing of barrier layers, and hybrid material development are helping manufacturers achieve superior encapsulation at reduced costs. These advancements are making flexible displays more viable for mass production, increasing their presence in smartphones, TVs, and wearables—and in turn, boosting demand for encapsulation solutions.

Market Restraints:

Despite its promising growth, the flexible screen crystal encapsulation market faces a major restraint in the form of high production costs and technical complexities. The development and application of advanced encapsulation techniques like thin-film or hybrid methods require expensive equipment, specialized materials, and highly controlled manufacturing environments. Additionally, ensuring consistent barrier performance while maintaining display flexibility poses significant engineering challenges. For smaller manufacturers or those in developing regions, these hurdles can limit entry and scalability. Moreover, any defect or inconsistency in encapsulation can severely affect product lifespan and reliability, leading to higher rejection rates and losses. As a result, many companies hesitate to invest heavily in flexible display production without guaranteed returns, slowing broader market adoption.

The socio-economic impact of the Global Flexible Screen Crystal Encapsulation Market is significant, as it supports the rapid evolution of next-generation consumer electronics, enhancing user experience and driving digital lifestyle adoption. Economically, it contributes to job creation in high-tech manufacturing, R&D, and supply chain sectors, particularly in regions like Asia-Pacific and North America. The market also fosters innovation and competitiveness among tech companies, encouraging investment in advanced materials and sustainable production methods. Socially, it promotes the proliferation of portable, energy-efficient, and multifunctional devices that improve communication, healthcare monitoring (through wearables), and infotainment accessibility. As flexible electronics become more mainstream, they can bridge the digital divide and enhance quality of life, especially in developing regions through affordable and durable smart devices.

Segmental Analysis:

The inorganic encapsulation materials segment is projected to witness significant growth due to its superior barrier properties against moisture, oxygen, and other environmental contaminants. Materials such as silicon nitride and aluminum oxide are commonly used for their excellent chemical stability and durability, making them ideal for protecting sensitive flexible OLED and AMOLED displays. Inorganic encapsulation is especially critical in applications requiring long-term reliability, such as foldable smartphones and high-end wearables. As manufacturers aim for enhanced performance and extended product lifespan, the demand for high-quality inorganic barrier films is rising.

Additionally, advancements in atomic layer deposition (ALD) techniques are improving the scalability and uniformity of inorganic coatings, further driving their adoption across large-scale production environments. For instance, in May 2025, an article published in the journal, npj Flexible Electronics, reported that research developed a silbione-blended organic/inorganic hybrid epoxy polymer (SBH) that significantly enhances the mechanical flexibility and durability of thin-film encapsulation for wearable organic light-emitting diodes (OLEDs) devices. The SBH films demonstrated superior toughness, low water vapor transmission rates, and strong protection under harsh conditions, making them highly suitable for flexible, wearable electronics. This advancement strengthens the inorganic encapsulation materials segment by improving barrier reliability and flexibility, supporting broader adoption of durable, high-performance flexible displays in the wearable market.

The thin-film encapsulation (TFE) segment is anticipated to see substantial growth due to its ability to provide lightweight, flexible, and highly effective protection for advanced displays. TFE consists of alternating layers of organic and inorganic materials, creating a multi-layer barrier that resists moisture and oxygen ingress while maintaining device flexibility. This technology is particularly important for foldable and rollable OLED displays, where traditional rigid encapsulation methods are unsuitable. The rising popularity of ultra-slim devices like foldable smartphones, curved televisions, and flexible wearables is driving TFE adoption. Furthermore, technological improvements in deposition methods—such as atomic layer deposition (ALD) and inkjet printing—are making TFE more cost-effective and scalable, enabling broader integration across the electronics industry and fueling segment growth.

The smartphones segment is expected to be the fastest-growing application area within the flexible screen crystal encapsulation market. As leading smartphone manufacturers increasingly incorporate foldable and flexible OLED screens into their flagship models, the need for durable, lightweight, and effective encapsulation solutions becomes critical. Consumer demand for innovation, larger displays in smaller form factors, and premium features is accelerating the shift toward foldable phones. Encapsulation plays a key role in protecting these sensitive flexible displays from environmental damage, ensuring device longevity and performance. Major brands like Samsung, Huawei, and Motorola are investing heavily in flexible display technology, which in turn boosts the demand for encapsulation materials and technologies. The trend is expected to continue as foldable smartphones move into mainstream adoption.

The Asia-Pacific region is poised to witness the highest growth in the flexible screen crystal encapsulation market, driven by the presence of leading display manufacturers and strong demand for consumer electronics. Countries like South Korea, China, Japan, and Taiwan are home to major players such as Samsung Display, LG Display, and BOE Technology, which are at the forefront of flexible OLED production.

The region benefits from robust manufacturing infrastructure, significant R&D investment, and supportive government policies promoting high-tech industries. For instance, in February 2025, ASUS announced the all-new Zenfone 12 Ultra, a premium 6.78-inch smartphone designed to redefine elegance, functionality, and innovation. Powered by the latest Snapdragon 8 Elite Mobile Platform, this flagship device combined modern style with advanced AI features, offering both on-device and cloud-based AI options. It also emphasized sustainable design, setting a new benchmark for premium smartphones in terms of performance and eco-friendliness. This announcement influenced the flexible screen crystal encapsulation market by increasing demand for high-quality, durable encapsulation materials that support large, advanced displays with AI capabilities. ASUS’s focus on premium design and sustainability pushed manufacturers to innovate more reliable and eco-friendly encapsulation solutions, thereby advancing the market’s growth and technological development.

Rapid urbanization, rising disposable incomes, and increased smartphone penetration in emerging markets like India and Southeast Asia further fuel demand for flexible electronic devices. As a result, the Asia-Pacific region is expected to remain a central hub for production, innovation, and consumption throughout the forecast period.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Flexible Screen Crystal Encapsulation Market is characterized by intense innovation, strategic partnerships, and strong R&D investment among key players aiming to gain technological leadership. Major companies such as Samsung SDI, LG Chem, 3M, BASF, Toppan Printing, and Universal Display Corporation dominate the market with advanced encapsulation technologies, particularly in thin-film and hybrid solutions. These players focus on enhancing barrier performance, reducing production costs, and scaling up manufacturing to meet rising demand from flexible OLED display manufacturers. Startups and smaller firms are also entering the market with niche innovations, contributing to healthy competition. Additionally, collaborations between material suppliers and electronics manufacturers are accelerating product development cycles and enabling faster commercialization of next-generation flexible devices.

List 20 major players for above market are:

Recent Developments

Q1. What are the main growth driving factors for this market?

The main drivers include the rising demand for flexible and foldable displays in smartphones, tablets, and wearable tech, along with advancements in OLED and AMOLED technologies. Consumer preference for lightweight, durable, and innovative electronics is pushing manufacturers to adopt flexible screen solutions. Additionally, increased R&D investments and rapid product launches by key players are boosting market growth globally.

Q2. What are the main restraining factors for this market?

The key restraints include the high cost of production and encapsulation materials, as well as complex manufacturing processes that require advanced infrastructure. Technical challenges in achieving long-term durability and perfect barrier protection can also hinder widespread adoption. Additionally, limited availability of skilled workforce and slow standardization of encapsulation technologies may slow down market expansion, especially among smaller manufacturers and emerging economies.

Q3. Which segment is expected to witness high growth?

The consumer electronics segment, particularly flexible smartphones and wearable devices, is expected to witness the highest growth. This is driven by increasing consumer demand for compact, foldable, and lightweight devices. Flexible OLED screens are gaining popularity due to their superior display quality and flexibility. As tech giants innovate with next-gen devices, the need for advanced encapsulation solutions in this segment continues to grow rapidly.

Q4. Who are the top major players for this market?

Leading players in the market include Samsung SDI, LG Chem, Toppan Printing Co. Ltd., 3M, and BASF. These companies invest heavily in R&D and advanced encapsulation technologies to maintain their market edge. They are involved in partnerships and product innovation to support the flexible display industry. Other notable players include Universal Display Corporation and Kateeva, contributing to technological advancements in this space.

Q5. Which country is the largest player?

South Korea is the largest player in the global flexible screen crystal encapsulation market, primarily due to the presence of major display manufacturers like Samsung and LG. The country leads in OLED technology, R&D capabilities, and mass production infrastructure. Its strong tech ecosystem and government support for electronics innovation have helped position South Korea at the forefront of this rapidly growing market.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model