Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Hi-Tech Medical Equipment Market is experiencing strong growth as healthcare systems increasingly transition toward advanced, technology-integrated diagnostic, monitoring, and treatment solutions. Growth is primarily driven by accelerating demand for precision healthcare, digital transformation in hospitals, rising deployment of AI-powered diagnostic tools, robotics-assisted surgical systems, and smart connected medical devices. The rising burden of chronic diseases, aging populations, and the shift toward minimally invasive and remote-care solutions are further strengthening market expansion.

The Global Hi-Tech Medical Equipment Market is witnessing several transformative trends driven by rapid advancements in healthcare technology and digital innovation. One of the most notable trends is the increasing integration of artificial intelligence (AI) and machine learning in medical imaging, diagnostics, and surgical systems, enabling faster, more accurate clinical decisions and personalized treatment plans. Robotics-assisted surgery and automated medical workflows are also gaining momentum as healthcare providers aim to improve procedural precision and reduce patient recovery time.

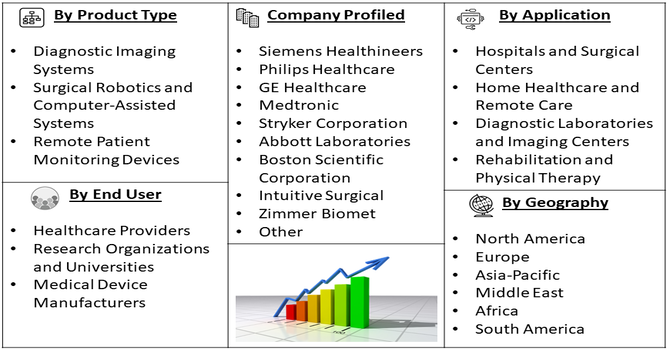

Segmentation: Global Hi-Tech Medical Equipment Market is segmented By Product Type (Diagnostic Imaging Systems, Surgical Robotics and Computer-Assisted Systems, and Remote Patient Monitoring Devices), Technology (Artificial Intelligence and Machine Learning-enabled Devices, Internet of Medical Things (IoMT)-Based Equipment, Augmented Reality (AR) and Virtual Reality (VR) Medical Systems, 3D Printing and Bioprinting Technologies), Application (Hospitals and Surgical Centers, Home Healthcare and Remote Care, Diagnostic Laboratories and Imaging Centers, Rehabilitation and Physical Therapy), End User (Healthcare Providers, Research Organizations and Universities, Medical Device Manufacturers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

One of the primary drivers of the Global Hi-Tech Medical Equipment Market is the increasing need for faster, more accurate, and minimally invasive diagnostic and treatment technologies. Chronic diseases such as cancer, cardiovascular disorders, diabetes, and neurological conditions continue to rise globally, placing pressure on healthcare systems to adopt advanced tools that improve clinical outcomes.

In 2025, The inauguration of AIIMS Raipur’s Robotic Surgery Facility, Devhast, had positively impacted the Global Hi-Tech Medical Equipment Market by driving demand for advanced robotic surgical systems. The adoption of minimally invasive, high-precision technology had enhanced patient outcomes, accelerated the use of cutting-edge medical devices, and supported training and research in robotic-assisted surgery worldwide. Hi-tech medical equipment—such as AI-enabled imaging systems, robotic surgical tools, wearable monitoring devices, and precision medical platforms—helps clinicians detect diseases earlier, personalize treatment plans, and significantly improve patient survival and recovery rates.

The rapid expansion of telemedicine, home healthcare, and remote patient monitoring is another major growth driver. The global healthcare landscape is shifting toward decentralized care models that reduce hospital burden and enhance accessibility, especially for aging populations and patients in rural or underserved regions. For instance, in August 2024, Pfizer’s launched, PfizerForAll digital platform had accelerated the rapid expansion of telemedicine and indirectly influenced the Global Hi-Tech Medical Equipment Market. By streamlining healthcare access and remote patient management, it increased demand for connected diagnostic tools, digital monitoring devices, and advanced medical equipment to support telehealth services and virtual care solutions. This shift has been accelerated by digital transformation initiatives, government healthcare modernization programs, and an increasing focus on cost efficiency and patient-centric care.

Market Restraints

The Global Hi-Tech Medical Equipment Market faced significant restraints due to limited affordability and the complexity of integration. High costs of advanced medical devices restricted access for smaller hospitals, clinics, and healthcare providers in developing regions, slowing market penetration.

Additionally, integrating sophisticated equipment into existing hospital systems required extensive technical expertise, training, and infrastructure upgrades. This complexity often led to longer implementation times and increased operational challenges. As a result, many healthcare facilities hesitated to adopt cutting-edge medical technologies, limiting overall growth. Together, high costs and integration difficulties remained key barriers to widespread adoption and expansion in the hi-tech medical equipment market.

The Global Hi-Tech Medical Equipment Market had a significant socioeconomic impact by improving healthcare quality, accessibility, and efficiency worldwide. Advanced diagnostic and treatment equipment enabled earlier disease detection, better patient outcomes, and reduced long-term healthcare costs. The market’s growth created employment opportunities in manufacturing, research, healthcare services, and technical support, while stimulating investment in related industries such as electronics and software. Additionally, widespread adoption of hi-tech medical devices had strengthened healthcare infrastructure, supported rural and urban health initiatives, and promoted innovation. Overall, the market’s expansion had enhanced public health, contributed to economic development, and improved quality of life for patients and communities globally.

Segmental Analysis

Diagnostic Imaging Systems emerge as a key growth area as healthcare providers increasingly adopt advanced imaging technologies such as MRI, CT, PET-CT, and hybrid scanners for accurate disease detection, oncology diagnostics, and real-time clinical decision-making. These systems are benefiting from rapid advancements in resolution quality, automated processing, and AI-based image interpretation, which help reduce diagnostic delays and enhance precision. Growing investment in early disease screening programs and increasing chronic disease prevalence further strengthen the dominance of this segment in the global market.

Artificial Intelligence and Machine Learning-enabled Devices are experiencing the fastest acceleration as AI becomes integral to predictive analytics, clinical automation, robotic-assisted procedures, and imaging diagnostics. These technologies enable faster and more accurate clinical insights, reduce human error, and support personalized treatment strategies across various specializations such as oncology, neurology, cardiology, and orthopedics. The convergence of AI with cloud platforms, IoMT ecosystems, and digital twins is reshaping healthcare delivery, making this segment one of the most transformative forces in the market.

Hospitals and Surgical Centers dominate due to their role as primary adopters of advanced medical technologies including robotic surgical systems, smart monitoring platforms, automated diagnostic machines, and digitally integrated operating rooms. Hospitals are increasingly investing in modernization initiatives, digital health systems, and minimally invasive surgical technology to enhance patient outcomes, improve workflow efficiency, and reduce procedural complications. The rising demand for precision surgery and intensive care monitoring continues to strengthen this segment’s market presence.

Healthcare Providers hold the largest share as they represent the frontline users of high-tech medical devices such as AI-enabled diagnostic systems, connected patient monitoring tools, and digital health platforms. Hospitals, clinics, and specialized care centers are prioritizing technology upgrades to meet evolving clinical standards, regulatory requirements, and patient expectations for faster, accurate, and personalized care delivery. Growing investments in digital transformation and workforce training further reinforce the dominance of this end-user group.

North America leads the global market, supported by strong research and development activities, advanced healthcare infrastructure, and high early adoption of emerging technologies. The presence of major medical device innovators, favorable reimbursement frameworks, and robust regulatory systems accelerates commercialization of next-generation solutions such as robotic surgery, AI-powered diagnostics, and connected care platforms. For instance, in October 2025, Osso VR’s launch of the Osso Nurse Training solution had strengthened the North American Hi-Tech Medical Equipment Market by promoting the adoption of immersive training technologies. The VR platform had enhanced nurse onboarding, improved procedural skills, and increased demand for advanced medical simulation equipment, driving innovation and growth in healthcare training solutions.

Rising healthcare spending and strategic government initiatives to promote digital and precision healthcare further position North America as the fastest-expanding regional market over the forecast period. For instance, The Centers for Medicare & Medicaid Services (CMS) reported that national health spending grew 8.2% in 2024 and projected a 7.1% increase in 2025. Over the period from 2024 to 2033, spending is expected to rise at an average annual rate of 5.8%, with Medicare expenditures growing 7.8% per year, reflecting continued expansion in healthcare demand and investment in medical technologies. Thus, such factors are fuelling this market’s growth in this region.

| Report Matrics | Details |

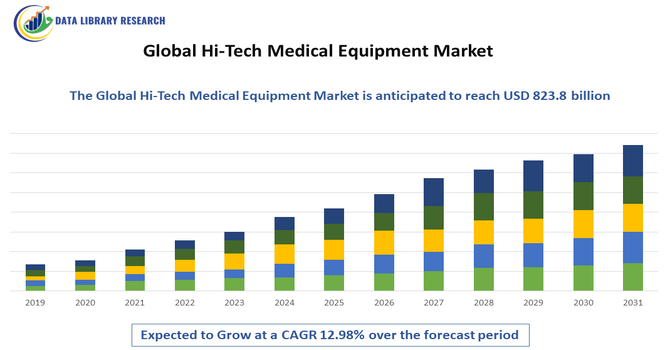

| Market Size Value | USD 823.8 billion |

| Growth Rate | CAGR of 12.98 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The Global Hi-Tech Medical Equipment Market is highly competitive and characterized by a strong presence of established multinational corporations, emerging technology innovators, and specialized medical device manufacturers. Companies are focusing on advancements in artificial intelligence–driven diagnostics, robotic-assisted surgery, remote patient monitoring, digital healthcare platforms, and connected medical systems to gain a competitive edge. Strategic partnerships, mergers and acquisitions, and continuous R&D investment are common strategies adopted to expand product portfolios and global reach. Furthermore, regulatory approvals, cybersecurity capabilities, and integration with digital health ecosystems such as IoMT, EHRs, and cloud-based platforms are becoming critical differentiators. With accelerating digitalization of healthcare and rising demand for precision medicine, innovation-driven competition continues to intensify across all product categories.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market's growth is primarily driven by the rising number of chronic illnesses globally, such as diabetes and heart conditions, which require continuous monitoring and advanced diagnostic tools. Additionally, the rapid aging of the population worldwide increases demand for sophisticated health tech. The widespread adoption of smartphones and high-speed internet also fuels this expansion, enabling remote patient monitoring and personalized, preventative healthcare solutions in the home setting.

Q2. What are the main restraining factors for this market?

Key restraining factors include the complex and stringent regulatory requirements imposed by bodies like the FDA and the European Union, which often delay product approval and significantly increase development costs. Furthermore, data privacy and cybersecurity challenges pose a major risk, as these high-tech devices handle and transmit vast amounts of sensitive patient information. High device costs and short product replacement cycles also limit adoption, especially in emerging economies.

Q3. Which segment is expected to witness high growth?

The segments focused on personalized and continuous monitoring solutions are expected to witness the highest growth. Specifically, wearable medical devices like smart straps, clips, and advanced fitness trackers are projected to grow exponentially due to their portability and ease of use in managing daily health. This trend strongly supports the application segment of Remote Patient Monitoring (RPM), which is central to the future of data-driven healthcare delivery.

Q4. Who are the top major players for this market?

The competitive landscape features a unique blend of established medical technology manufacturers and major consumer electronics companies. Traditional MedTech leaders include firms such as Medtronic, Siemens Healthineers, and Royal Philips. However, significant market expansion and innovation are increasingly driven by technology giants like Apple Inc., Google, and Xiaomi, who leverage their consumer platforms to offer sophisticated smart watches and connected diagnostic wearables.

Q5. Which country is the largest player?

North America holds the dominant market share globally for high-tech medical equipment, with the United States being the single largest country player within that region. This leadership position is due to its substantial healthcare expenditure, advanced digital infrastructure, and favorable reimbursement policies that strongly encourage the swift adoption of cutting-edge diagnostic and monitoring technologies. The US also remains the global hub for research and development in medical device innovation.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model