Get Complete Analysis Of The Report - Download Updated Free Sample PDF

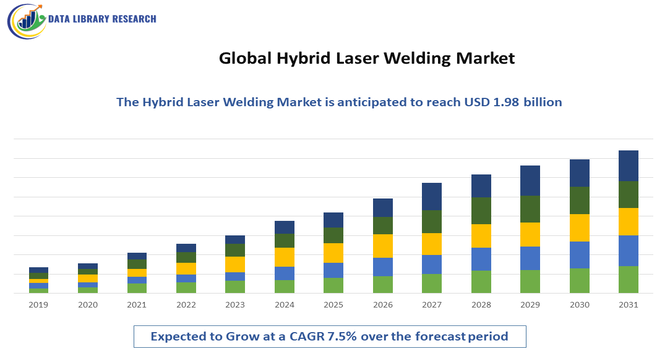

The Global Hybrid Laser Welding Market is experiencing strong growth, driven primarily by the increasing demand for high-precision, high-strength welding solutions across automotive, aerospace, shipbuilding, and heavy engineering industries. The hybrid laser welding process—combining laser beams with traditional arc welding—offers superior penetration depth, faster welding speeds, reduced heat distortion, and improved joint quality, making it ideal for advanced manufacturing requirements.

Additionally, the push toward lightweight materials, rising adoption of automation and Industry 4.0 technologies, and the need for cost-efficient, high-productivity welding systems are further accelerating market expansion worldwide.

The Global Hybrid Laser Welding Market is currently leveraging several key trends that are reshaping its dynamics: first, there is rapid integration of AI and automation, with hybrid welding systems increasingly combining real-time process monitoring, adaptive control, and predictive analytics to optimize weld quality and minimize defects. Second, manufacturers are embracing Industry 4.0 connectivity, embedding IoT sensors, digital twins, and edge computing into welding cells to support traceability, remote diagnostics, and closed-loop feedback control. Third, green and energy-efficient laser sources—including green-wavelength lasers—are gaining momentum, especially for joining dissimilar or challenging materials such as copper and aluminum used in EVs and advanced electronics.

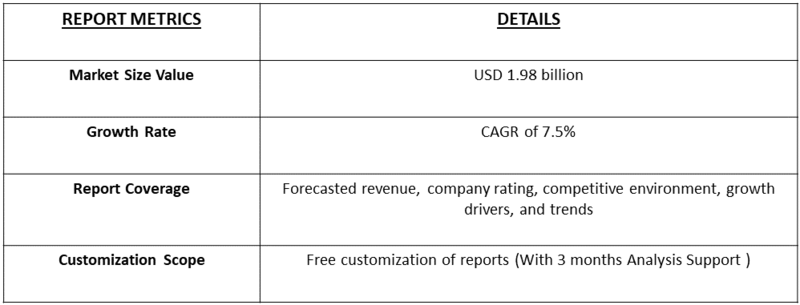

Segmentation: Global Hybrid Laser Welding Market is segmented By Laser Type (Fiber Lasers, CO₂ Lasers, Diode Lasers, Solid-State Lasers), Welding Technique (Laser-MIG (Metal Inert Gas) Hybrid Welding, Laser-TIG (Tungsten Inert Gas) Hybrid Welding, Laser-Plasma Hybrid Welding), Material Type (Steel, Aluminum, Stainless Steel, High-Strength Low-Alloy (HSLA) Materials), Application (Automotive Manufacturing, Aerospace and Defense, Shipbuilding, Heavy Machinery and Equipment, Energy and Power Sector), End User (Fabrication Shops, Industrial Manufacturing Facilities, Research and Development Institutions), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

The Global Hybrid Laser Welding Market has had a significant socioeconomic impact by enhancing manufacturing efficiency, precision, and safety across industries such as automotive, aerospace, and electronics. By enabling faster production with minimal errors, it reduces labor costs and resource wastage. The technology also supports the adoption of advanced electric and hybrid vehicles, promoting cleaner transportation solutions. Its implementation drives skilled job creation in high-tech sectors while encouraging innovation in industrial processes. Thus, hybrid laser welding contributes to economic growth, environmental sustainability, and improved product quality, benefiting both manufacturers and end consumers worldwide.

Market Drivers:

The major drivers boosting the Global Hybrid Laser Welding Market is the rising adoption of lightweight and high-strength materials across the automotive and aerospace industries. As manufacturers shift toward materials such as advanced high-strength steels (AHSS), aluminum alloys, titanium, and composites to reduce vehicle weight and improve fuel efficiency, conventional welding techniques often fall short due to their limitations in joining dissimilar materials, higher heat input, distortion issues, and inability to produce deep penetration welds. For instance, In April 2024, Hyundai Motor Group formalized a strategic cooperation agreement with Toray Industries, Inc., the global leader in carbon fiber technology, to significantly advance material innovation for future mobility.

This collaboration is centrally focused on the joint research and development of lightweight, high-strength materials, particularly Carbon Fiber-Reinforced Polymer (CFRP) components. These advanced composites are slated for critical applications, including casings for Electric Vehicle (EV) battery systems and structural elements of electric motors. The partnership is a cornerstone of Hyundai Motor Group's long-term electrification strategy, aiming to simultaneously enhance vehicle performance, maximize battery range, and ensure superior structural safety and customer experience across its next-generation EV lineup.

The increasing adoption of automation and Industry 4.0 technologies across manufacturing facilities is another strong driver for market growth. Hybrid laser welding systems are highly compatible with robotic automation, real-time monitoring tools, digital twins, and AI-based process optimization, making them central to modern smart manufacturing environments. For instance, in November 2025, Viam partnered with Universal Robots to integrate UR Series collaborative robots into its industrial automation solutions. Leveraging AI-powered robotic surfacing systems, the collaboration enhanced manufacturing efficiency, reduced delays, and ensured process consistency. Amid ongoing labor shortages, these solutions enabled automation of physically demanding tasks, accelerating Industry 4.0 adoption and boosting precision and productivity, thereby positively impacting the growth of the Global Hybrid Laser Welding Market.

Segmental Analysis:

Fiber lasers hold a dominant position in the hybrid laser welding market due to their superior beam quality, higher energy efficiency, and ability to weld a wide range of materials with exceptional precision. Their compact design, low maintenance requirements, and high electrical-to-optical efficiency make them highly suitable for industrial environments. Fiber lasers are increasingly preferred in automotive, aerospace, and heavy machinery production, where intricate welds, deeper penetration, and high-speed processing are required. Their compatibility with automation and robotic welding systems further elevates their adoption in advanced manufacturing setups.

Laser-MIG hybrid welding is the most widely adopted technique because it combines the penetration strength of laser welding with the filler metal capabilities of MIG welding. This technique enables the joining of thicker materials, enhances gap-bridging ability, and reduces welding defects such as porosity and cracking.

Industries such as shipbuilding, automotive body manufacturing, and construction equipment production rely heavily on Laser-MIG hybrid welding due to its ability to deliver strong, consistent welds with high productivity rates. The technique also supports cost savings by reducing post-weld finishing and improving overall operational efficiency.

Steel represents one of the largest material segments in hybrid laser welding as it remains a primary material across automotive, shipbuilding, construction, and heavy machinery industries. Hybrid laser welding offers significant advantages when processing steel, including deep weld penetration, minimal distortion, and improved joint strength.

High-strength steel variants used in modern vehicle frames and structural components particularly benefit from this welding method due to its ability to maintain mechanical integrity. As manufacturers increasingly adopt lightweight yet durable structures, the demand for hybrid welding for steel applications continues to rise.

The automotive manufacturing segment is a key driver of hybrid laser welding adoption due to the industry’s focus on precision welding, automation, and lightweight material integration. Hybrid laser welding is extensively used in body-in-white (BIW) assembly, chassis components, battery housings in electric vehicles, and structural frames.

Its ability to weld complex geometries at high speed while maintaining superior joint quality makes it ideal for mass production environments. With the global shift toward electric and hybrid vehicles, the demand for advanced welding solutions in battery systems and high-strength steel components is amplifying further growth within this segment.

Industrial manufacturing facilities represent a significant end-user segment as they deploy hybrid laser welding for large-scale production, heavy-duty component fabrication, and automation-driven processes. These facilities benefit from the flexibility, high repeatability, and reduced fabrication time offered by hybrid laser welding systems. Industries such as machinery, metal fabrication, energy equipment manufacturing, and transportation components rely on this technology to enhance productivity, improve weld consistency, and optimize production cost structures. As smart manufacturing and Industry 4.0 adoption accelerate globally, industrial manufacturing facilities are increasingly integrating hybrid welding systems into automated production lines.

North America is expected to witness the highest growth in the Global Hybrid Laser Welding Market over the forecast period, driven by the region’s strong manufacturing infrastructure, rapid technological adoption, and substantial investments in advanced welding automation.

The automotive and aerospace industries, which demand high-precision welding for lightweight materials and structural components, are major contributors to market expansion. For instance, in October 2025, Siemens and rhobot.ai launched their advanced AI solution for manufacturing, following successful deployment at CarbonAMS in Ireland. The edge-native AI, available via Siemens Xcelerator, enabled real-time optimization and control of industrial processes by integrating with factory automation hardware and software. Building on 2024 pilots with Agbotic Inc., the solution enhanced efficiency and precision, driving North America’s robust manufacturing infrastructure, rapid technology adoption, and significant investments, thereby positively impacting the growth of the Global Hybrid Laser Welding Market.

Additionally, the region’s emphasis on reshoring manufacturing operations and increasing production efficiency fuels the adoption of hybrid welding solutions across fabrication shops and industrial plants. The presence of key technology providers, growing integration of Industry 4.0 practices, and expanding electric vehicle manufacturing further support market acceleration in the United States and Canada.

Thus, such factors together are driving the market’s growth in this region.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Hybrid Laser Welding Market is shaped by a mix of specialized laser manufacturers, traditional welding-equipment leaders, robotics and automation integrators, and system integrators that bundle lasers with arc sources, sensors, and process-control software. Companies compete on laser source performance, hybrid process integration (laser + arc), automation and robotics compatibility, closed-loop monitoring and quality assurance features, service & maintenance networks, and industry-specific turnkey solutions for sectors like automotive, aerospace, and shipbuilding.

The major players for this market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the soaring demand for lightweight, high-strength structures, especially in automotive and aerospace sectors. Hybrid laser welding offers superior advantages like high speed, deep penetration, and minimized thermal distortion, which are essential for increasing manufacturing efficiency and product quality. This technology is crucial for modern automated production lines seeking high throughput and reliable joint strength for critical components.

Q2. What are the main restraining factors for this market?

Market expansion is constrained mainly by the substantial initial capital investment required for purchasing and integrating hybrid laser welding machinery. Furthermore, the specialized nature of the technology demands highly skilled technicians for operation and maintenance, resulting in a significant knowledge and talent gap. This high cost and complexity act as a notable barrier to broader adoption, particularly among smaller companies.

Q3. Which segment is expected to witness high growth?

The Automotive segment is predicted to experience the highest growth due to the global push for electric vehicle (EV) manufacturing and vehicle lightweighting initiatives. Within the technology, the high-power fiber laser segment is also seeing rapid adoption. These advanced systems are becoming vital for joining dissimilar materials and ensuring the structural integrity and precision required for assembling modern vehicles and their battery packs.

Q4. Who are the top major players for this market?

The market is dominated by global manufacturing and laser technology giants. Key players include major industrial equipment and laser specialists like TRUMPF, Coherent, Inc., and IPG Photonics Corporation, which supply the core laser sources. Additionally, automation and robotics companies such as KUKA AG and FANUC Corporation are significant contributors, integrating the complex hybrid welding systems into comprehensive production solutions worldwide.

Q5. Which country is the largest player?

The Asia-Pacific (APAC) region currently holds the largest market share, with China being the dominant country player. This leadership is fueled by the country's massive and rapidly expanding automotive manufacturing industry and high production volumes in general electronics and heavy machinery. Strong governmental support and investment in advanced manufacturing techniques further cement the region's top position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model