Get Complete Analysis Of The Report - Download Updated Free Sample PDF

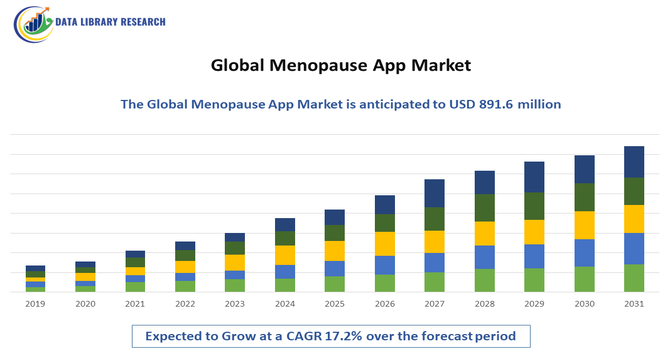

The Global Menopause App Market is witnessing robust growth, driven by the rising adoption of digital health solutions, increasing awareness of women’s health, and the growing prevalence of menopause-related symptoms among the aging female population. Menopause apps are designed to assist women in tracking symptoms, monitoring hormonal changes, managing lifestyle adjustments, and accessing educational and therapeutic support during the menopausal transition. The market is gaining momentum due to the growing emphasis on personalized healthcare, integration of artificial intelligence (AI) and machine learning (ML) for predictive symptom tracking, and the rising popularity of telemedicine platforms that offer remote consultations with gynecologists and wellness experts.

The Global Menopause App Market is experiencing rapid transformation, driven by emerging digital health trends and the growing focus on women’s midlife wellness. The key trends is the expansion of FemTech into menopause care, as developers shift focus from fertility and menstrual tracking toward supporting women aged 40–60 through perimenopause and postmenopause. The market is seeing increasing adoption of AI-driven and wearable-integrated solutions, enabling personalized insights, predictive symptom tracking, and seamless integration with smart devices for real-time monitoring of hot flashes, sleep patterns, and mood fluctuations.

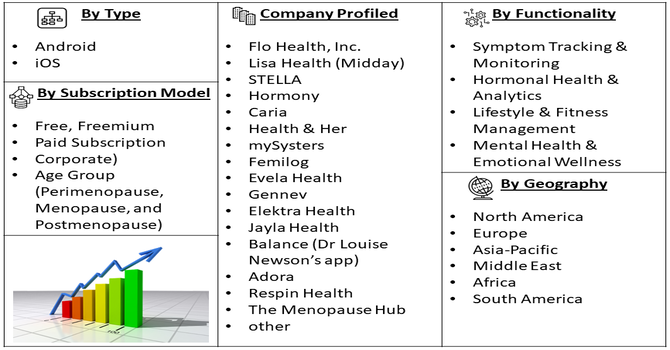

Segmentation: The Global Menopause App Market is segmented By Platform Type (Android, and iOS), Functionality (Symptom Tracking & Monitoring, Hormonal Health & Analytics, Lifestyle & Fitness Management, Mental Health & Emotional Wellness), Subscription Model (Free, Freemium, Paid Subscription, and Corporate), Age Group (Perimenopause, Menopause, and Postmenopause), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Increasing global awareness about menopause and its impact on women’s physical and mental health is a major driver of the menopause app market. Governments, healthcare organizations, and FemTech companies are actively promoting discussions around menopause, reducing stigma, and encouraging women to seek digital health support. For instance, as part of PM Narendra Modi’s “Swasth Nari, Sashakt Parivar Abhiyaan,” JIPMER Nursing College organized a Postnatal Depression awareness campaign on 22 September 2025 in Puducherry. Nursing faculty and students educated OPD patients and the public through talks, counselling, and materials, promoting early recognition and support. The initiative improved women’s mental and physical wellbeing and highlighted the need for digital health tools, indirectly influencing the global menopause and women’s health app market.

As more women prioritize holistic wellness and preventive healthcare, menopause apps that provide symptom tracking, lifestyle recommendations, and educational resources are witnessing growing adoption. This heightened awareness, coupled with greater acceptance of digital health tools, is significantly expanding the market’s user base.

The integration of artificial intelligence (AI), machine learning (ML), and wearable technologies is revolutionizing menopause care. Modern menopause apps now offer personalized insights, predictive analytics for symptom management, and data synchronization with smartwatches and fitness trackers. For instance, in March 2025, Sidekick Health launched a 12-week clinical study in Germany to evaluate its prescription digital therapeutic, MENO! App, targeting unmet needs of menopausal women. The study validated the app’s effectiveness in symptom relief and showcased technological advancements, including AI integration and wearable compatibility, reinforcing innovation in digital health and boosting growth and adoption within the global menopause app market.

Market Restraints:

The major restraints in the global menopause app market is the growing concern over data privacy and security. These apps collect highly sensitive personal health information, including hormonal data, mental health status, and lifestyle habits. Inadequate data protection measures, lack of transparency in data usage, and instances of third-party data sharing have led to user distrust. As regulatory scrutiny over digital health platforms intensifies—particularly under frameworks like GDPR and HIPAA—companies face increasing compliance challenges. This has slowed adoption among privacy-conscious users and limited the expansion of some apps in regions with strict data protection laws.

The global menopause app market is reshaping socioeconomic dynamics by empowering millions of women to better manage symptoms through digital tools, which not only improves quality of life but also helps reduce healthcare costs and productivity losses; with the market already valued in the hundreds of millions and growing rapidly, it attracts major investment, spurs innovation in femtech, and addresses a long neglected healthcare gap—yet it also risks deepening inequalities, since subscription costs or digital literacy barriers may exclude lower income women from these benefits.

Segmental Analysis:

The Android segment holds the largest share of the global menopause app market, primarily due to the widespread availability and affordability of Android smartphones, especially in emerging economies such as India, China, and Brazil. The open-source nature of the Android platform allows developers to introduce affordable and easily accessible menopause management applications to a broad user base. Additionally, the Google Play Store’s vast ecosystem supports a diverse range of wellness and health-tracking apps, enhancing accessibility for women across various income levels. The increasing compatibility of Android devices with wearable technologies and fitness trackers further drives the segment’s growth.

The Symptom Tracking & Monitoring segment dominates the market as it forms the core function of most menopause apps. These apps enable women to record, monitor, and analyze symptoms such as hot flashes, mood changes, sleep disturbances, and menstrual irregularities. With the integration of artificial intelligence (AI) and data analytics, modern tracking features now offer predictive insights, helping users anticipate and manage symptoms more effectively. Continuous monitoring not only empowers women to understand their bodies but also facilitates data sharing with healthcare providers for personalized treatment. The growing demand for self-management tools and increased awareness about menopausal health contribute significantly to the expansion of this segment.

The Freemium model accounts for the highest revenue share in the menopause app market, as it allows users to access essential tracking features for free while offering advanced analytics, virtual consultations, and lifestyle guidance through paid premium tiers. This model has proven successful in attracting large user bases while generating steady revenue from premium upgrades. Additionally, it caters to diverse economic groups by providing flexibility between free and subscription-based access. The success of the freemium model is further enhanced by app developers’ strategies to integrate targeted advertisements and personalized recommendations, creating a balance between accessibility and profitability.

The Perimenopause segment represents the largest user group in the menopause app market, as women in this age range experience early hormonal fluctuations and symptom onset. This phase is marked by irregular menstrual cycles, mood swings, sleep disruptions, and physical changes that encourage women to seek digital health support. Perimenopausal women are increasingly turning to mobile apps for tracking symptoms, accessing educational content, and receiving lifestyle recommendations to ease the transition into menopause. The segment’s dominance is also supported by growing awareness campaigns and the adoption of digital health tools among women in their 40s who are more tech-savvy and health-conscious.

North America dominates the global menopause app market, driven by high smartphone penetration, strong digital health infrastructure, and widespread acceptance of FemTech solutions.

The region’s leading position is reinforced by growing awareness of women’s health issues, availability of advanced apps with AI and telehealth integration, and the presence of key market players offering evidence-based digital therapeutic solutions. For instance, in October 2025, a USD 5 million grant from the Steven & Alexandra Cohen Foundation, led by Alex Cohen, funded the digital-innovation phase of the NextGen Now initiative, creating a digital ecosystem for updated educational content. The project supported training for current and future healthcare professionals, advanced AI and wearable technology integration, and strengthened North America’s menopause app market by enhancing digital tools for midlife women’s care.

The U.S. market, in particular, benefits from collaborations between healthcare providers, employers, and insurers to integrate menopause support into workplace wellness programs. Furthermore, strong regulatory frameworks for digital health technologies and a growing emphasis on personalized medicine continue to stimulate market expansion across the region.

To Learn More About This Report - Request a Free Sample Copy

The Global Menopause App Market is moderately fragmented and highly competitive, with numerous FemTech startups and digital health companies introducing innovative solutions for women’s midlife health. Key players are focusing on integrating AI-driven analytics, wearable connectivity, and telehealth features to enhance user engagement and personalization. Strategic collaborations with healthcare providers, wellness platforms, and pharmaceutical companies are becoming common to expand service offerings and credibility. Companies are also emphasizing evidence-based content, data privacy, and holistic wellness support to differentiate themselves in an increasingly crowded market.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is primarily driven by the rapidly aging global female population, with over a billion women expected to be post-menopausal by 2025. This large demographic is seeking digital tools for symptom management, tracking, and personalized health guidance. Increased investment in women's health technology (FemTech) and rising consumer awareness of digital health solutions also propel growth.

Q2. What are the main restraining factors for this market?

Key restraining factors include user concerns over data privacy and security, as these apps handle highly sensitive personal health information. Additionally, the existing social stigma surrounding menopause can make some women reluctant to use or discuss dedicated apps. There is also a lack of sufficient technological proficiency among some older users, limiting the potential user base.

Q3. Which segment is expected to witness high growth?

Within the broader women's health market, the Menopause app segment itself is projected to be among the fastest-growing categories. Furthermore, the demand for Personalized Insights features is set for high growth. These features use AI and tailored data to provide customized recommendations for symptom relief, lifestyle adjustments, and communication with healthcare providers.

Q4. Who are the top major players for this market?

The market is highly competitive and features a mix of specialized FemTech startups and established health app developers. Some of the top players include Flo Health, Clue, Natural Cycles, Glow, and Ovia Health. These companies are continually adding specific menopause-related features and integrating them with broader women's health and wellness platforms to capture market share.

Q5. Which country is the largest player?

North America holds the largest market share in the Menopause App and the broader Women's Health App market. This dominance is due to the high digital literacy, widespread smartphone adoption, and a strong culture of health awareness and high spending on digital healthcare services in the region, particularly in the United States.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model