Covid-19 Impact on Military IoT Market:As the COVID-19 pandemic continuing its effect around the world, many defense and aerospace companies are facing its impact during this time around the world. For instance, commercial aviation companies in the U.S., France, Germany, and Canada are facing disruption in the production process and reduced demand as workforces staying at home, passengers stop traveling, and delay in delivery of new aircraft. Analysts expecting a drop from 3,000 to 4,000 aircraft during the pandemic period. On the defense side, contractors operating in the sector are in a better position, hence the impact of the pandemic is likely low in the short to mid-term. However, low demand due to budget constraints affecting the production as in aircraft manufacturing.

Market OverviewThe growing use of IoT in BMS for the special operations and the changing nature of the warfare are key drivers for the market growth. The growth of global military IoT market is determined by factors such as increased use of the IoT in BMS for the special operations and the changing nature of warfare. Furthermore, growing adoption of AI in the warfare systems for logistics and transportation, battlefield healthcare, and the data information processing is anticipated to boost growth of market.

Military IoT encompasses use of technologies such as the global positioning systems (GPS) and the satellite communication to deliver real-time information to the military commanders. Real-time data provided by the military IoT systems enables operators to plan the operations and take the optimal decisions. Moreover, these systems offer numerous benefits such as better situational awareness and data on equipment health, permitting users to practise enhanced safety. Though, issues associated with the data management and the threats to cybersecurity may hinder market growth.

Segment OverviewDevices that use Wi-Fi technology comprise laptops, desktops, digital cameras, smartphones and tablets, and drones. Companies including Thales Group are using the Wi-Fi for themilitary IoT systems. Hence, Wi-Fi segment is anticipated to register CAGR of over 11.0% during forecast period.

Based on application, global military IoT market has been categorised as health monitoring, training and simulation, real-time fleet management, equipment maintenance, inventory management, and others. Training and simulation segment is expected to exhibit highest CAGR during forecast period. The growing adoption of wearable devices by the armed forces for the training purposes is driving growth of the segment.

Regional OverviewThe market in North America is likely to register CAGR of over 10.0% during forecast period. The growth of market in North America is motivated by factors such as growing adoption of IoT systems and high military expenditure by government and defense bodies in region. According to (SIPRI) Stockholm International Peace Research Institute, the U.S. was the largest spender on military. The country augmented investments from 2015, USD 596 billion to USD 610 billion in the year 2017.

Furthermore, growing use of the IoT-based systems and the components by U.S. Army for overseas operations in the countries such as Syria and Iraq are boosting the market growth in region. In Canada, increasing investments by Canadian government in info technology for military is bolstering market growth. For example, in Jan 2019, the Public Services and Procurement Canada signed over three contracts with the General Dynamics Corporation for combined value of USD 621.5 million to deliver support for control, land command, communications, intelligence, surveillance, computers, and reconnaissance (LC4ISR) systems.

Competitor overviewIn Nov 2018, the FLIR Systems Inc. introduced FLIR TruWITNESS, wearable sensor platform intended for city-level security and the public safety operations. Furthermore, FLIR Systems Inc. was presented cost-plus-fixed-fee five-year contract by U.S. Department of the Defense’s (DTRA) Defense Threat Reduction Agency.

Key Players

- FLIR Systems Inc.

- Forescout Technologies, Inc.

- AT&T Inc.

- Northrop Grumman Corporation

- Honeywell International Inc.

- BAE Systems

- FreeWave Technologies, Inc.

- Harris Corporation

- IBM Corporation

- Thales Group

- SAP SE

- Lockheed Martin Corporation

Market SegmentationBy Technology

- Wi-Fi

- Cellular

- RFID

- Others

By Component

- Hardware

- Software

- Services

By Application

- Training and Simulation

- Real-Time Fleet Management

- Health Monitoring

- Equipment Maintenance

- Inventory Management

- Others

By Geography

- North America

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- UAE

- Rest of LAMEA

Research Process

Data Library Research are conducted by industry experts who offer insight on

industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager

and SOFT) of the companies that active & prominent as well as the midsized organization

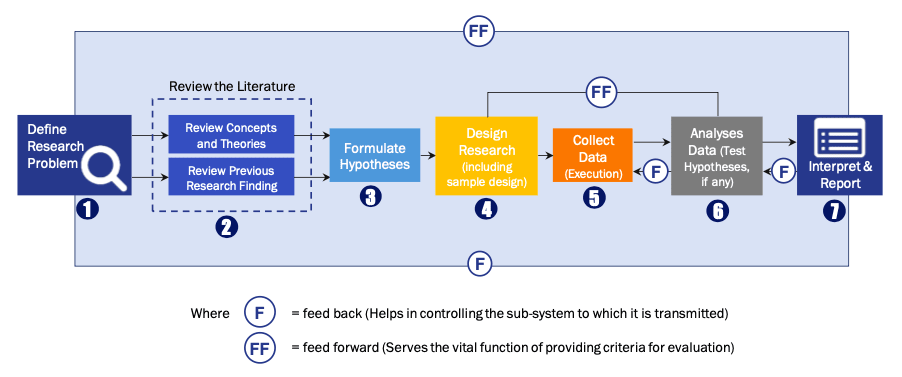

FIGURE 1: DLR RESEARH PROCESS

Primary Research

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary Research

Secondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size Estimation

Both, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model