Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Mini Limit Switches Market involves compact electromechanical devices used to detect object presence or position in automation and control systems. These switches are essential in industries like manufacturing, automotive, and robotics for precise motion control and safety applications.

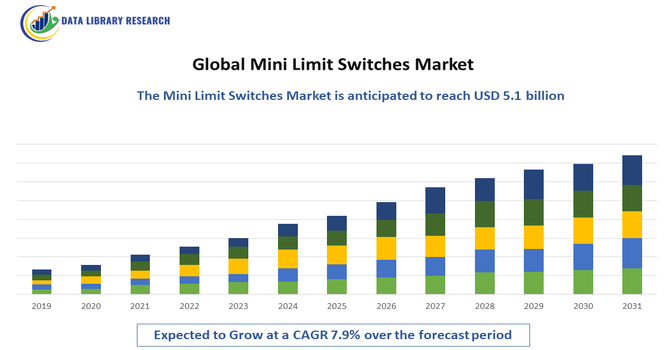

Market growth is driven by increasing automation across industries, rising demand for compact and reliable control devices, advancements in smart manufacturing, and the need for efficient space-saving solutions in machinery. Additionally, expanding applications in automotive safety systems and industrial robotics further propel the market’s expansion globally. Furthermore, the growing emphasis on Industry 4.0 and the integration of Internet of Things (IoT) technologies have accelerated the adoption of mini limit switches, enabling real-time monitoring and enhanced operational efficiency. Strict government regulations regarding workplace safety and machine performance also boost demand. Additionally, rising investments in emerging economies’ manufacturing sectors and continuous innovation in switch materials and designs contribute to market growth by improving durability, sensitivity, and environmental resistance of mini limit switches.

The Global Mini Limit Switches Market has witnessed significant trends, including the shift toward compact, high-precision switches for automation and robotics applications. Increasing adoption of smart factories and Industry 4.0 technologies has driven demand for switches with IoT compatibility and real-time monitoring capabilities. Additionally, manufacturers are focusing on durable, environmentally resistant designs suitable for harsh industrial conditions. The growing use of mini limit switches in automotive, packaging, and electronics sectors, coupled with rising demand in emerging markets, is shaping overall market growth.

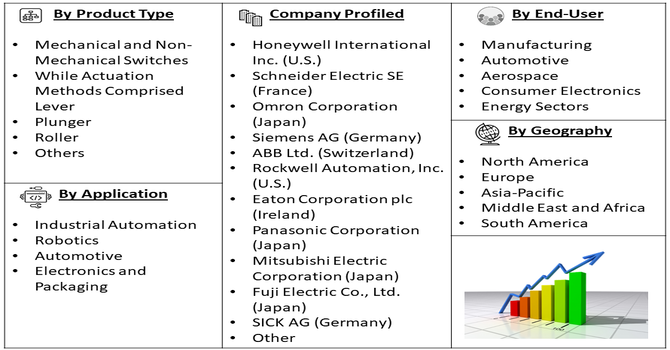

Segmentation: The Global Mini Limit Switches Market was segmented By Type (Mechanical and Non-Mechanical Switches, While Actuation Methods Comprised Lever, Plunger, Roller, and Others), Applications (Industrial Automation, Robotics, Automotive, Electronics and Packaging), End-User Industries ( Manufacturing, Automotive, Aerospace, Consumer Electronics, and Energy Sectors) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Driver:

The global surge in industrial automation has significantly driven the mini limit switches market. Manufacturers across automotive, food & beverage, and electronics industries increasingly integrate automated machinery to enhance operational efficiency, reduce labor costs, and improve precision. Mini limit switches, known for their compact design, reliability, and cost-effectiveness, are critical in detecting object position, controlling machinery movement, and ensuring safety in automated systems. As industries continue to expand and modernize their production lines, the demand for mini limit switches is expected to grow, supporting seamless integration in robotics, conveyors, and other automated equipment worldwide.

The expanding automotive and electronics sectors have contributed to rising demand for mini limit switches globally. In vehicles, these switches are used for door detection, gear position monitoring, and safety systems, while in electronics, they ensure precise control in devices like printers, vending machines, and home appliances. Increasing production of electric vehicles, smart devices, and automated consumer electronics has amplified the need for compact, durable, and accurate limit switches. Additionally, stringent safety and regulatory requirements in these sectors further drive adoption, reinforcing the market’s steady growth trajectory across Asia-Pacific, North America, and Europe.

Market Restraint

The growth of alternative sensor technologies, such as proximity sensors, photoelectric sensors, and Hall-effect sensors, has posed a challenge for the mini limit switches market. These non-contact sensors offer higher precision, durability, and flexibility, reducing mechanical wear and maintenance needs. Industries seeking advanced automation solutions increasingly favor these alternatives, which can integrate more easily with modern control systems and IoT platforms. Consequently, mini limit switches face competitive pressure, particularly in high-tech manufacturing and electronics applications, restraining market expansion despite strong demand in traditional industrial and automotive segments.

The Global Mini Limit Switches Market significantly impacts the economy by enabling widespread industrial and manufacturing automation, directly contributing to increased productivity, efficiency, and reduced operational costs across sectors like automotive and robotics. This efficiency gain, however, has a socioeconomic dual edge: while it boosts GDP and global competitiveness, it also accelerates job displacement in routine manual labor, demanding workforce retraining in maintenance and high-tech automation roles. Societally, these switches enhance worker safety by providing reliable mechanical fail-safes in heavy machinery, reducing industrial accidents and lowering healthcare costs associated with workplace injuries, thus balancing economic growth with social well-being.

Segmental Analysis:

The Non-Mechanical Switches segment in the Global Mini Limit Switches Market was projected to witness the highest growth over the forecast period. This growth was driven by increasing adoption of advanced sensing technologies that provide higher precision, durability, and faster response times compared to traditional mechanical switches. Non-mechanical switches, including capacitive, optical, and magnetic types, offered enhanced reliability in harsh environments and reduced maintenance costs, making them suitable for emerging industries such as robotics, medical devices, and smart manufacturing. The rising demand for compact, energy-efficient, and contactless switching solutions further fueled the adoption of non-mechanical switches, positioning this segment as a key driver of market expansion globally.

The Industrial Automation segment was expected to witness the highest growth over the forecast period, reflecting the global push toward Industry 4.0 and smart manufacturing. Mini limit switches were increasingly integrated into automated assembly lines, robotic systems, and conveyor mechanisms to monitor position, motion, and safety parameters with high precision. Growing demand for process optimization, reduced downtime, and improved operational efficiency encouraged manufacturers to adopt mini limit switches extensively. Additionally, the shift toward predictive maintenance and IoT-enabled smart factories further boosted the adoption of these switches, as industries required reliable and compact sensing solutions capable of sustaining continuous operations under harsh industrial conditions.

The Aerospace segment was projected to experience the highest growth over the forecast period due to the increasing demand for lightweight, reliable, and high-performance mini limit switches in aircraft systems. These switches were critical in monitoring flight control surfaces, landing gear operations, fuel systems, and cabin mechanisms, ensuring operational safety and efficiency. Rising global air travel, investments in next-generation aircraft, and advancements in unmanned aerial vehicles (UAVs) created a surge in demand for precise and durable switching solutions. The need for switches capable of withstanding extreme temperatures, vibrations, and pressure variations further reinforced the adoption of mini limit switches in aerospace applications worldwide.

The North America region was expected to witness the highest growth over the forecast period, driven by rapid industrial automation adoption, advanced manufacturing technologies, and strong aerospace and automotive sectors. The region’s emphasis on Industry 4.0 initiatives, smart factories, and safety-compliant automation solutions significantly boosted demand for mini limit switches. Additionally, government incentives for technological innovation, robust R&D infrastructure, and the presence of major players in electronics, robotics, and defense industries supported market growth. Increasing demand for efficient, compact, and durable switching solutions across multiple industrial and commercial applications further positioned North America as a leading growth region in the global mini limit switches market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Mini Limit Switches Market featured a blend of established multinational corporations and emerging regional players thereby creating a moderately fragmented environment. Key players such as Schneider Electric SE, Omron Corporation, Honeywell International Inc., ABB Ltd. and Siemens AG invested heavily in R&D, advanced product portfolios, and geographic expansion to gain competitive edge. Innovation in miniaturisation, IoT enabled features, ruggedness, and customisation emerged as key differentiators. Regional firms focused on cost effective solutions and local market agility. Strategic collaborations, acquisitions and partnerships reshaped market dynamics, while high entry barriers and regulatory standards limited new entrants.

The major players for above market:

Recent Development

Q1. What are the main growth driving factors for this market?

The market is primarily propelled by the widespread adoption of industrial automation and smart manufacturing (Industry 4.0) across global sectors. Mini limit switches are essential for providing precise position detection and reliable safety mechanisms in increasingly complex, automated machinery, robotics, and assembly lines. Furthermore, the push for miniaturization of components in applications like consumer electronics and automotive systems creates specific demand for small, high-precision, and durable electromechanical switches.

Q2. What are the main restraining factors for this market?

Major constraints include competition from alternative, non-contact sensing technologies, such as proximity sensors and photo-electric devices, which are often favored for their superior durability in harsh, dirty environments. Additionally, the longevity and reliability of traditional mechanical switches are highly vulnerable to environmental factors like extreme temperatures, vibration, and dust/moisture ingress, necessitating higher IP ratings and increasing material costs to ensure consistent performance.

Q3. Which segment is expected to witness high growth?

The Automotive and Electronics Manufacturing application segments are expected to witness high growth. This is driven by the rapid expansion of electric vehicle (EV) production, requiring compact, reliable switches for safety and control systems, and the dense automation in electronics assembly lines. By function, the segment focused on safety applications is also growing quickly, propelled by stringent global machine safety regulations that mandate reliable switch mechanisms to prevent accidents and ensure operational compliance.

Q4. Who are the top major players for this market?

The market is dominated by well-established global industrial technology and automation companies. Top major players include Honeywell International Inc., OMRON Corporation, Schneider Electric SE, and Siemens AG. These companies leverage their strong brand trust, broad product portfolios, and extensive global distribution networks. Their competitive edge lies in the ability to produce highly reliable, certified switches (e.g., UL, CE) and integrate advanced features like wireless connectivity for IoT-enabled predictive maintenance applications.

Q5. Which country is the largest player?

The Asia Pacific (APAC) region, led by China, is the largest market player in terms of both production and consumption volume. This dominance is due to the region's status as the global manufacturing powerhouse, experiencing rapid industrialization, extensive factory automation, and massive infrastructure development. The high volume of production across the automotive and electronics sectors in China, Japan, and South Korea drives immense, continuous demand for all types of limit switches, including the miniature variants.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model