Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Nasal Preparations Market involves products designed for delivering drugs through the nasal cavity to treat various conditions such as allergies, sinusitis, nasal congestion, and respiratory diseases. It includes sprays, drops, gels, and powders that provide rapid absorption, ease of use, and targeted therapy. Growing prevalence of respiratory disorders, increasing demand for non-invasive drug delivery, and advancements in formulation technologies drive this market’s expansion worldwide.

The Global Nasal Preparations Market is witnessing rapid growth driven by rising respiratory disorders and increased awareness of nasal drug delivery benefits. Innovations in formulations, such as nasal sprays with improved bioavailability and targeted delivery systems, are gaining traction. The demand for non-invasive and fast-acting treatments for allergies, sinus infections, and migraines fuels product adoption. Additionally, growth in biologics and vaccines administered nasally is expanding the market scope. Increasing OTC availability, coupled with technological advancements like mucoadhesive and sustained-release nasal gels, supports a dynamic and evolving competitive environment. Emerging markets also contribute significantly due to improved healthcare access.

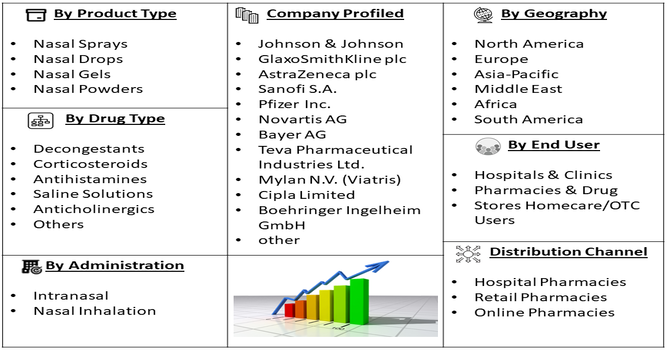

Segmentation: The Global Nasal Preparations Market is segmented by Product Type (Nasal Sprays | Nasal Drops | Nasal Gels | Nasal Powders), Drug Type (Decongestants | Corticosteroids | Antihistamines | Saline Solutions | Anticholinergics | Others (Vaccines, Peptides, Biologics)), Route of Administration (Intranasal | Nasal Inhalation), End User (Hospitals & Clinics | Pharmacies & Drug Stores | Homecare/OTC Users), Distribution Channel (Hospital Pharmacies | Retail Pharmacies | Online Pharmacies) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The Global Nasal Preparations Market is significantly driven by the increasing prevalence of respiratory conditions such as allergic rhinitis, sinusitis, asthma, and chronic obstructive pulmonary disease (COPD). Nasal sprays, gels, and drops offer rapid symptom relief, targeted therapy, and non-invasive administration, making them preferred among patients. Additionally, rising air pollution, allergens, and seasonal infections contribute to higher demand for nasal formulations. Hospitals, clinics, and pharmacies are witnessing growing prescription and OTC sales, fueling market expansion. Increasing awareness of nasal drug delivery benefits among patients and healthcare providers further strengthens adoption globally.

Technological innovations in nasal drug delivery have fueled market growth by improving therapeutic efficacy and patient compliance. Developments such as mucoadhesive formulations, sustained-release gels, nanoparticle-based sprays, and intranasal vaccines enhance bioavailability and provide rapid onset of action. These advancements enable treatment of systemic conditions like migraines, CNS disorders, and infectious diseases via nasal administration. Additionally, integration with biologics and peptide-based therapeutics expands clinical applications. Pharmaceutical companies increasingly focus on R&D to deliver safer, more effective nasal formulations, driving adoption in both developed and emerging markets.

Market Restraints:

The market growth is restrained by stringent regulatory requirements and safety concerns associated with nasal formulations. Nasal products must meet rigorous approval standards for efficacy, sterility, and stability, which can delay product launches. Additionally, potential side effects like nasal irritation, epistaxis, or systemic exposure may limit patient acceptance. High development costs and complex manufacturing processes further challenge smaller players. Differences in regulatory frameworks across countries complicate global commercialization strategies. These factors collectively slow market expansion despite rising demand, emphasizing the need for robust safety testing and compliance to maintain consumer trust and regulatory approval.

Nasal preparations provide cost-effective, non-invasive treatment options, improving patient compliance and reducing hospitalization for respiratory and neurological conditions globally. This accessibility helps lower healthcare burdens, especially in underserved regions where injectable or oral medications pose challenges. Widespread use supports productivity by enabling faster relief from allergies and sinus issues, positively influencing workforce efficiency. Furthermore, nasal vaccines promote public health by facilitating easier immunization, particularly in pandemics. The market’s growth fosters employment and drives pharmaceutical innovation. However, economic disparities may limit access in low-income areas, underscoring the need for affordable formulations and expanded healthcare infrastructure.

Segmental Analysis:

The nasal sprays segment is expected to witness the highest growth over the forecast period due to its ease of administration, rapid onset of action, and ability to deliver targeted therapy. Increasing prevalence of respiratory conditions like allergic rhinitis, sinusitis, and asthma drives demand. Advancements in formulations, including mucoadhesive sprays, nanoparticle-based delivery, and intranasal vaccines, further boost adoption. Both prescription and over-the-counter products are gaining traction in developed and emerging markets. Healthcare providers prefer nasal sprays for non-invasive therapy, contributing to steady market expansion globally.

The decongestants segment is projected to grow significantly due to rising cases of nasal congestion caused by allergies, colds, and sinus infections. Nasal decongestants offer rapid relief, improving patient comfort and quality of life. Increasing awareness of their effectiveness and the availability of both OTC and prescription options drive widespread adoption. Technological innovations such as extended-release and combination formulations enhance efficacy. Growth in respiratory disorders and seasonal allergies globally, along with strong demand in hospitals, clinics, and retail pharmacies, positions decongestants as a high-growth segment within the nasal preparations market.

Hospitals and clinics are expected to witness the highest growth among end-user segments due to the increasing preference for professional administration of nasal therapies, especially for severe respiratory conditions and intranasal vaccines. Healthcare facilities provide access to a wide range of prescription nasal sprays, gels, and drops, ensuring safety and dosage accuracy. Rising patient visits for allergic rhinitis, sinusitis, and chronic respiratory diseases, coupled with advanced therapeutic options available in hospitals.

The hospital pharmacies segment of the Global Nasal Preparations Market is expected to witness the highest growth over the forecast period due to increasing patient admissions for respiratory illnesses, allergies, and chronic sinus conditions. Hospitals rely on nasal sprays, decongestants, and corticosteroids for rapid symptom relief and targeted therapy. Integration of advanced inventory management systems and easy access to prescription nasal formulations enhance their adoption in hospital settings. Additionally, rising preference for non-invasive treatments and physician recommendations drive demand. Hospital pharmacies also serve as key distribution hubs, facilitating timely access to both inpatient and outpatient nasal medications, boosting market expansion.

North America is expected to witness the highest growth in the Global Nasal Preparations Market over the forecast period due to a high prevalence of respiratory disorders, advanced healthcare infrastructure, and strong awareness of nasal drug delivery benefits.

The region’s well-established pharmaceutical industry, coupled with increasing R&D investments in innovative formulations such as intranasal vaccines, biologics, and peptide-based therapies, accelerates adoption. For instance, in March 2023, Amneal Pharmaceuticals, Inc. announced U.S. FDA approval for its naloxone hydrochloride nasal spray, a generic version of Narcan. This spray is designed to quickly treat opioid overdose emergencies, providing an accessible, life-saving option amid rising opioid crisis concerns, and expanding treatment availability across emergency and healthcare settings in the United States.

Also in March 2023, Pfizer, Inc. received U.S. FDA approval for ZAVZPRET, the first nasal spray targeting the calcitonin gene-related peptide (CGRP) receptor. This novel treatment offers adults an effective, non-invasive option for acute migraine relief, marking a significant advancement in migraine management and expanding the use of nasal sprays for neurological conditions. Additionally, favorable reimbursement policies, high per-capita healthcare expenditure, and increasing OTC availability of nasal sprays and decongestants further drive market growth. Thus, the presence of leading players and robust regulatory support contributes to North America’s dominance in the market.

| Report Matrics | Details |

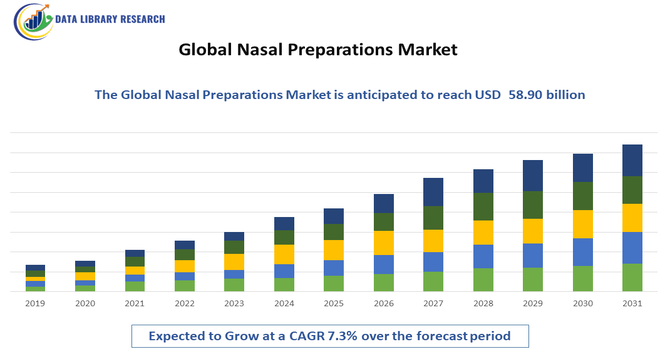

| Market Size Value | USD 58.90 billion |

| Growth Rate | CAGR of 7.3 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The Global Nasal Preparations Market is highly competitive, featuring key players such as Johnson & Johnson, GlaxoSmithKline, AstraZeneca, Sanofi, and Pfizer. Companies focus on innovation through R&D, launching novel nasal sprays, gels, and powders with enhanced efficacy and patient convenience. Strategic collaborations, mergers, and acquisitions aim to expand product portfolios and geographic reach. Additionally, generic manufacturers are increasing market share by offering cost-effective alternatives. Regional players in emerging markets contribute to competition by catering to localized needs. Regulatory compliance, patent expirations, and evolving consumer preferences shape competitive strategies, making innovation and cost-efficiency critical for maintaining market leadership.

The major players for this market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is growing primarily because more people are suffering from allergies, sinus infections, and chronic respiratory issues like asthma. Air pollution and urbanization are making these conditions more common. Additionally, patients prefer nasal sprays because they are painless, easy to use at home, and provide much faster relief than oral pills.

Q2. What are the main restraining factors for this market?

Growth is held back by concerns over side effects, such as nasal irritation, dryness, or "rebound congestion" from overusing certain sprays. Strict government regulations for new product approvals and high development costs also slow down innovation. Furthermore, frequent product recalls due to manufacturing issues can sometimes damage consumer trust and limit market expansion.

Q3. Which segment is expected to witness high growth?

The Nasal Sprays segment is also expected to witness the highest growth over the forecast period. This dominance is driven by the rapid adoption of corticosteroid and antihistamine sprays for chronic respiratory management. Furthermore, the expansion of nasal delivery for systemic treatments, such as for migraines, depression, and emergency opioid reversals, is significantly broadening the segment's market reach.

Q4. Who are the top major players for this market?

The market is led by major global pharmaceutical companies that specialize in respiratory care. Key players include GlaxoSmithKline (GSK), Cipla Inc., Bayer AG, Sanofi, and Johnson & Johnson. These companies stay ahead by launching new, preservative-free formulas and partnering with tech firms to create more efficient spray devices.

Q5. Which country is the largest player?

The United States is the largest player in this market. It has a high number of people with hay fever and sinus problems, along with a very advanced healthcare system. The easy availability of both prescription and over-the-counter nasal products, combined with heavy spending on medical research, keeps the U.S. in the top position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model