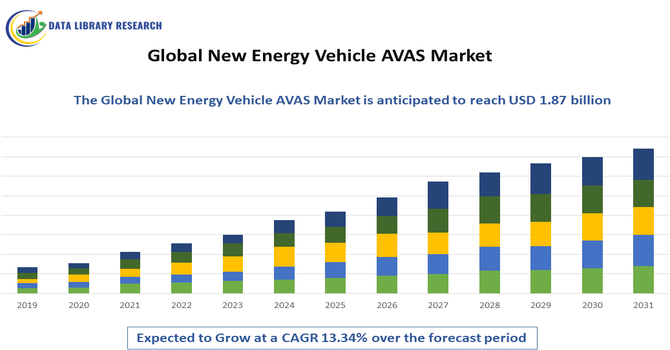

The global acoustic vehicle alerting system market size was valued at USD 470.8 million in 2026 and is expected to grow at a compound annual growth rate (CAGR) of 13.34% from 2026-2033, reaching USD 1.87 billion in 20233.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global New Energy Vehicle (NEV) Acoustic Vehicle Alerting System (AVAS) Market includes electronic sound systems designed to emit artificial noise for electric and hybrid vehicles at low speeds to alert pedestrians and cyclists. Because NEVs operate quietly, AVAS enhances safety by reducing collision risks, especially in urban and congested environments. Systems vary in sound type, volume control, and integration with vehicle electronics. Regulatory mandates in many countries require AVAS compliance for new electric and hybrid models.

The NEV AVAS market is being driven by rising global electric vehicle adoption and increasingly stringent safety regulations requiring audible alerts for pedestrian protection. Governments in North America, Europe, and Asia-Pacific have mandated AVAS installation at low speeds, prompting OEMs to integrate compliant systems in new models. Technological advancements, including customizable sound profiles, directional alerts, and integration with vehicle sensors, are shaping product innovation. Consumers and regulators are also pushing for enhanced sound design that balances safety with noise pollution concerns.

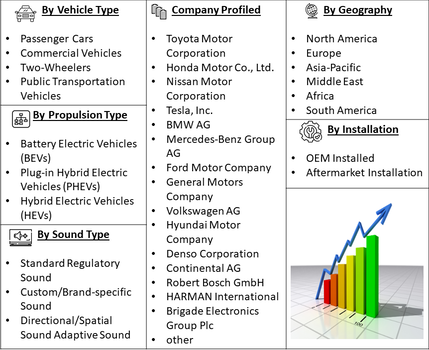

Segmentation: The Global New Energy Vehicle (NEV) Acoustic Vehicle Alerting System (AVAS) Market is segmented by Vehicle Type (Passenger Cars, Commercial Vehicles (Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs)), Two-Wheelers and Public Transportation Vehicles), Propulsion Type (Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Hybrid Electric Vehicles (HEVs) and Fuel Cell Electric Vehicles (FCEVs)), AVAS Type (Internal Speaker-Based AVAS, External Speaker-Based AVAS, Integrated AVAS (Vehicle’s existing audio system) and Stand-alone AVAS Modules), Sound Type (Standard Regulatory Sound, Custom/Brand-specific Sound, Directional/Spatial Sound and Adaptive Sound (Speed & Environment-based)), Installation (OEM Installed and Aftermarket Installation), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The main drivers of the NEV AVAS market is the growing number of global regulations mandating pedestrian alert systems for electric and hybrid vehicles. Since NEVs operate quietly at low speeds, governments in Europe, North America, and Asia have introduced rules requiring artificial noise to protect pedestrians and cyclists. Automakers must comply with these standards, leading to widespread AVAS adoption across new vehicle models. Regulatory enforcement has accelerated integration of AVAS into production lines, creating steady demand for compliant systems and supporting market expansion as NEV sales continue to rise worldwide.

The rapid growth of electric and hybrid vehicle adoption is a major driver for the NEV AVAS market. As more consumers switch to NEVs for environmental and economic reasons, the demand for safety technologies that address quiet operation increases. AVAS is essential for pedestrian safety, especially in urban and high-foot-traffic areas.

In July 2024, Stellantis’ rapid expansion of hybrid models and eDCT technology in Europe supported rising electric vehicle adoption by offering more accessible electrified options. This growth also strengthened the global NEV AVAS market, as increased hybrid vehicle production drove demand for pedestrian alert systems to meet safety regulations, accelerating AVAS integration across a broader range of electrified vehicle platforms worldwide. The expansion of public charging infrastructure, government incentives, and declining battery costs are accelerating NEV sales, thereby boosting the need for AVAS integration across various vehicle types, including passenger cars, commercial vehicles, and public transport fleets.

Market Restraints

A key restraint for the NEV AVAS market is the growing concern over noise pollution and public acceptance of artificial vehicle sounds. While AVAS enhances safety, some consumers and urban residents oppose loud or intrusive alerts, especially in quiet residential areas. Poorly designed or overly loud AVAS systems can lead to complaints and regulatory pushback, forcing manufacturers to balance safety with acceptable sound levels. Additionally, variability in sound standards across regions can complicate product development and increase costs. These challenges can slow market growth as companies work to develop effective yet socially acceptable AVAS solutions.

NEV AVAS adoption enhances public safety by reducing pedestrian and cyclist accidents in urban areas where electric vehicles operate quietly. This contributes to safer mobility environments and encourages broader electric vehicle acceptance. The market also supports job creation in manufacturing, software development, and vehicle integration services. As AVAS becomes standard in electric and hybrid vehicles, it fosters innovation in audio engineering and sensor technologies. Compliance with safety standards also reduces litigation risks for automakers and can lower societal costs from traffic injuries. Moreover, by addressing safety without increasing harmful emissions, AVAS supports sustainable urban transport and public health objectives in growing metropolitan regions.

Segmental Analysis:

The Heavy Commercial Vehicles (HCVs) segment is expected to witness the highest growth over the forecast period due to increasing adoption of electric trucks and buses for logistics and public transport. As commercial fleets expand in urban areas, safety concerns for pedestrians and cyclists have become more prominent, driving demand for AVAS solutions. HCVs also face stricter safety regulations and higher compliance pressure, encouraging OEMs to integrate AVAS systems during manufacturing. Additionally, fleet operators prioritize reliable and durable AVAS units that can withstand heavy usage, boosting growth in the HCV segment as electrification accelerates in the commercial sector.

The Plug-in Hybrid Electric Vehicles (PHEVs) segment is expected to witness the highest growth over the forecast period as PHEVs continue to gain popularity among consumers seeking a balance between electric driving and longer range. Since PHEVs operate quietly in electric mode, AVAS systems are essential for pedestrian safety, especially in city driving conditions. Growing government incentives and stricter emission norms are encouraging PHEV adoption, which in turn increases AVAS demand. Automakers are increasingly integrating AVAS in PHEV models to meet regulatory requirements and enhance safety, supporting strong growth in this segment.

The integrated AVAS segment is expected to witness the highest growth over the forecast period due to its cost-efficiency and seamless integration with existing vehicle systems. Automakers are increasingly adopting integrated AVAS solutions that utilize the vehicle’s existing audio components, reducing the need for additional hardware and simplifying installation. This approach also allows for better control and customization of sound profiles through the vehicle’s software. As OEMs seek scalable, affordable solutions to meet global regulations, integrated AVAS systems offer a practical option that supports efficient manufacturing and maintenance, driving strong adoption across passenger and commercial NEVs.

The standard regulatory sound segment is expected to witness the highest growth over the forecast period as most countries mandate specific AVAS sound requirements for pedestrian safety. Standardized sound profiles ensure consistent alerting performance and simplify compliance for automakers across regions. These sounds are typically designed to be easily recognizable and effective at low speeds without causing excessive noise pollution. As NEV production increases, manufacturers prioritize regulatory-compliant AVAS systems to avoid penalties and meet safety standards. The demand for standard sound solutions remains strong, especially for mass-market vehicles and fleets, driving growth in this segment.

The aftermarket installation segment is expected to witness the highest growth over the forecast period due to rising retrofitting demand for existing NEVs and hybrid vehicles. As regulatory standards evolve, many older electric and hybrid models require AVAS upgrades to remain compliant. Fleet operators and individual vehicle owners are increasingly opting for aftermarket solutions to enhance safety without replacing vehicles. Additionally, the growth of used NEV markets and conversion of traditional vehicles to electric powertrains is boosting aftermarket AVAS demand. With more affordable and customizable retrofit options available, the aftermarket segment is poised for strong growth.

The Asia-Pacific region is expected to witness the highest growth over the forecast period due to rapid electric vehicle adoption and expanding urbanization. Countries such as China, India, Japan, and South Korea are investing heavily in NEV infrastructure and offering incentives to accelerate electrification. For instance, in 2026, Mitsubishi Motors’ production of the Navara for Oceania and the Rogue Plug-in Hybrid for North America strengthened Asia-Pacific’s NEV AVAS market by accelerating electrified vehicle manufacturing and cross-border OEM collaboration. The Alliance’s expanded EV and PHEV lineup increased demand for AVAS integration in regional vehicles, supporting broader adoption of pedestrian safety systems across Asia-Pacific’s growing electric mobility sector.

Increasing awareness of pedestrian safety in densely populated cities is driving regulatory adoption of AVAS systems. The region’s growing manufacturing capabilities and strong presence of automotive OEMs and suppliers also support rapid AVAS integration. As NEV sales surge and regulations tighten, Asia-Pacific is expected to lead growth in the global AVAS market.

| Report Matrics | Details |

| Market Size Value | USD 1.87 billion |

| Growth Rate | CAGR of 13.34% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The NEV AVAS market features established automotive suppliers, specialized audio technology firms, and emerging sound design innovators competing for partnerships with electric vehicle manufacturers. Key players differentiate through advanced sound synthesis, regulatory compliance expertise, and integration capabilities with vehicle electronic systems. Competition also revolves around customization options, system reliability, and cost-effectiveness. Collaborations between OEMs and tech providers are common, as automakers seek scalable AVAS solutions for diverse vehicle platforms. Geographic expansion and local regulatory knowledge are strategic assets, especially in regions with evolving safety standards.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

Strict government regulations mandating sound emitters for quiet electric vehicles primarily drive this market. As EV adoption surges globally, safety concerns for pedestrians and the visually impaired necessitate AVAS technology. Additionally, automotive manufacturers are leveraging sound branding to differentiate their electric models, creating unique auditory identities for high-end consumer vehicles.

Q2. What are the main restraining factors for this market?

High implementation costs for advanced, multi-directional sound systems act as a significant restraint. Manufacturers face challenges in balancing external noise pollution with safety requirements. Furthermore, a lack of global standardization regarding specific sound frequencies and decibel levels creates complexity for suppliers. Technical issues like electromagnetic interference can also complicate the integration process.

Q3. Which segment is expected to witness high growth?

The passenger car segment is expected to witness the highest growth. This is fueled by the massive global shift toward private electric vehicle ownership and increasingly stringent urban safety laws. Within this, the high-fidelity sound segment is expanding rapidly as premium brands invest in customizable acoustic signatures to enhance user experience.

Q4. Who are the top major players for this market?

The market is dominated by global Tier-1 automotive suppliers including Bosch, Denso Corporation, Continental AG, and HARMAN International. Other key players include Brigade Electronics, Hella GmbH, and Kendrion. These companies focus on developing smart acoustic solutions that integrate with vehicle sensors to adjust sound volume based on speed and environment.

Q5. Which country is the largest player?

China is the largest player in the AVAS market due to its position as the world's leading producer and consumer of electric vehicles. Strong government subsidies and early implementation of domestic safety standards for "quiet vehicles" have allowed Chinese manufacturers to scale production and lead in technological deployment for EVs.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model