Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Online Patient Registry Software Market refers to the industry that develops digital platforms for systematic collection, storage, management, and analysis of patient health data. These solutions support clinical care, disease tracking, research, and regulatory reporting by enabling real time access to longitudinal patient information. Integration with electronic health records and analytics tools improves decision-making, research outcomes, and population health management worldwide.

The Global Online Patient Registry Software Market is evolving with strong growth in cloud based, interoperable solutions that integrate seamlessly with electronic health records (EHRs) to enable real world evidence generation and longitudinal care tracking. Use of interoperable registries for disease management, post marketing surveillance, and outcome research is increasing rapidly, especially for chronic and rare conditions. Advanced analytics and AI incorporation into registry platforms enables predictive insights and patient segmentation. Demand for modular and scalable systems that support multi site clinical studies and real time data sharing is rising. These trends reflect the shift toward data driven, patient centric care delivery and research infrastructure globally.

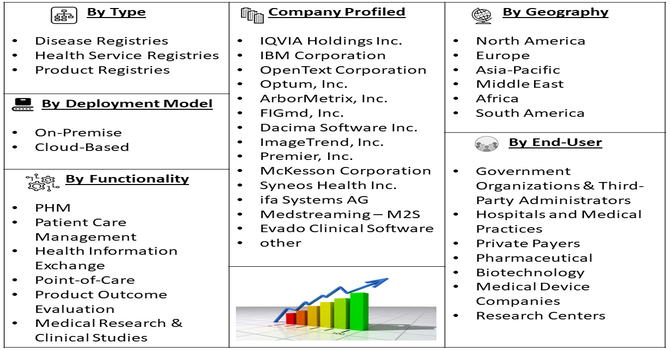

Segmentation: The Global Patient Registry Software Market, By Type (Disease Registries, Health Service Registries, and Product Registries), Software (Standalone, and Integrated), Pricing Model (Subscription, and Ownership), Deployment Model (On-Premise, and Cloud-Based), Database (Commercial, and Public), Functionality (PHM, Patient Care Management, Health Information Exchange, Point-of-Care, Product Outcome Evaluation, and Medical Research & Clinical Studies), End Use (Government Organizations & Third-Party Administrators, Hospitals and Medical Practices, Private Payers, Pharmaceutical, Biotechnology, and Medical Device Companies, and Research Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The Global Online Patient Registry Software Market is being driven by the growing adoption of digital health solutions, including electronic health records (EHRs), telemedicine, and remote patient monitoring systems. For instance, in January 2025, the Punjab Government launched a centralized platform to manage patient registration for outpatient opioid treatments, preventing misuse of Buprenorphine and improving care. This initiative boosted the adoption of digital health solutions and growth in the Global Patient Registry Software Market.

Healthcare providers increasingly rely on digital registries to collect and analyze longitudinal patient data, enabling improved clinical decision-making and personalized care. Integration with analytics and AI tools allows tracking of treatment outcomes, disease progression, and patient adherence. The shift toward value-based care and real-world evidence generation further accelerates registry adoption, positioning online patient registry software as a crucial component of modern healthcare infrastructure.

Increasing prevalence of chronic and rare diseases worldwide has created strong demand for patient registry software. These platforms facilitate systematic data collection, tracking, and reporting of disease-specific information, enabling healthcare providers, researchers, and pharmaceutical companies to monitor patient outcomes, optimize treatment protocols, and support clinical trials. For instance, in October 2025, NORD launched a mobile app linked to its IAMRARE® Registry Platform, enabling easier patient participation in rare disease studies. This initiative advanced rare and chronic disease management and accelerated the growth of the Global Online Patient Registry Software Market.

Registries help in real-world evidence generation, post-marketing surveillance, and regulatory compliance, especially for orphan drugs. The ability to collect large-scale, longitudinal patient data efficiently enhances research capabilities and supports evidence-based decision-making, thereby significantly driving the growth of the global online patient registry software market.

Market Restraints:

A major restraint for the global online patient registry software market is the growing concern around data privacy, security, and regulatory compliance. Handling sensitive patient information online exposes healthcare organizations to potential cyberattacks, unauthorized access, and data breaches. Compliance with regional regulations such as HIPAA, GDPR, and other local laws increases complexity and operational costs. Additionally, concerns about patient consent and data sharing can limit participation in registries, affecting data completeness and accuracy. These factors create hesitation among providers and organizations in fully adopting online registry solutions, slowing the overall market growth despite strong demand.

The Global Online Patient Registry Software Market has a significant socioeconomic impact by enhancing healthcare quality, research, and policy decision making. Centralized registries improve chronic disease tracking, outcomes monitoring, and evidence generation needed for value based care and regulatory submissions. They reduce administrative burden, enable better resource allocation, and support public health surveillance. Broader adoption of registry platforms aids clinical research and accelerates drug development, benefiting patients and healthcare systems. By improving data accessibility and standardization, these solutions contribute to reduced healthcare costs and more timely interventions. Additionally, they support equitable care delivery and population health management, particularly in chronic and rare disease communities.

Segmental Analysis:

The Disease Registries segment is expected to witness the highest growth due to the rising prevalence of chronic, rare, and lifestyle-related diseases globally. Healthcare providers, pharmaceutical companies, and research organizations are increasingly leveraging disease-specific registries to collect longitudinal patient data, monitor treatment outcomes, and generate real-world evidence. These registries support clinical trials, post-marketing surveillance, and regulatory reporting, improving patient care and operational efficiency. Growing adoption of AI and analytics tools integrated with registries further enhances their utility, driving market growth. The focus on personalized medicine and value-based care accelerates adoption in this segment.

The Standalone segment is anticipated to experience significant growth as healthcare organizations prefer dedicated patient registry software that operates independently of other hospital management or EHR systems. Standalone solutions offer flexibility, customization, and easier implementation for specialized clinical research and disease tracking needs. They allow healthcare providers to focus on specific patient populations or conditions without the complexity of integrating with broader IT infrastructure. Additionally, standalone systems reduce dependency on multiple platforms and enable rapid deployment. This approach is increasingly favored by research institutions, specialty clinics, and pharmaceutical companies for managing disease registries and longitudinal studies efficiently.

The Subscription segment is expected to witness substantial growth due to the cost-effective, flexible, and scalable nature of subscription-based patient registry software. Organizations can access software on a pay-as-you-go model without heavy upfront investments in licenses or infrastructure. Subscription solutions often include regular updates, maintenance, and cloud support, ensuring compliance with evolving healthcare regulations. This model is particularly attractive to small and medium-sized healthcare providers, research institutions, and pharmaceutical companies looking to manage patient data efficiently. The predictable operational expenses, rapid deployment, and accessibility from multiple locations accelerate adoption of subscription-based registry software across global markets.

The Cloud-Based segment is projected to grow rapidly as healthcare organizations increasingly adopt cloud computing for secure, scalable, and centralized patient data management. Cloud-based registries enable real-time access to longitudinal patient data, facilitate multi-site collaboration, and enhance integration with EHRs and analytics tools. They reduce infrastructure costs, improve data backup and recovery, and support regulatory compliance. Additionally, cloud platforms allow remote access and real-time updates, which is critical for research, disease surveillance, and clinical trials. The growing demand for digital health solutions and remote patient management drives the adoption of cloud-based patient registry software globally.

The Commercial segment is expected to witness high growth as pharmaceutical companies, biotechnology firms, and contract research organizations increasingly adopt patient registry software for clinical trials, drug development, and post-marketing surveillance. Commercial registries provide actionable insights into patient populations, treatment outcomes, and disease progression, supporting evidence-based decision-making. The growing focus on rare diseases, personalized medicine, and real-world evidence generation fuels the demand for commercial patient registry platforms. Additionally, regulatory requirements for data collection, reporting, and compliance incentivize commercial entities to invest in robust registry solutions, further driving the market’s expansion in this segment.

The Patient Care Management segment is projected to grow significantly as healthcare providers adopt registry software to improve patient outcomes, optimize care delivery, and manage chronic and complex diseases effectively. Registries help track patient history, monitor treatment adherence, and provide predictive insights for personalized interventions. Integration with analytics and decision-support tools allows clinicians to identify high-risk patients and implement timely care plans. The emphasis on value-based care and patient-centric healthcare models globally drives the adoption of registry software in patient care management. This segment’s growth reflects the need for efficient, data-driven approaches to enhance healthcare quality.

The Hospitals and Medical Practices segment is expected to witness the highest growth due to the increasing need for streamlined patient data management and improved care coordination. Hospitals and clinics use patient registry software to maintain comprehensive records, track disease outcomes, and support clinical research initiatives. Adoption is driven by the integration of EHRs, regulatory compliance requirements, and the need for efficient care delivery. Additionally, registry software enhances operational efficiency, reduces administrative burden, and facilitates quality reporting. The segment’s growth reflects the global trend of digital transformation in healthcare facilities to improve patient outcomes and research capabilities.

The North America region is expected to witness the highest growth over the forecast period due to advanced healthcare infrastructure, high adoption of digital health technologies, and strong government support for patient data management. The presence of major software providers, growing investment in clinical research, and increasing prevalence of chronic and rare diseases drive demand. For instance, in April 2024, Neuralink’s startup Synchron launched a patient registry to track U.S. Strentrode device recipients, facilitating large-scale clinical trial recruitment. This initiative boosted the adoption and growth of North America’s Online Patient Registry Software Market.

Similarly, in June 2024, OM1 launched its Registries Center of Excellence (CoE), assembling expert teams to provide advanced RWE and AI-powered insights. This initiative strengthened North America’s Online Patient Registry Software Market by enhancing registry capabilities, consultation services, and data-driven healthcare solutions.

Additionally, stringent regulatory requirements, such as HIPAA compliance, encourage healthcare organizations to implement robust patient registry solutions. High awareness of value-based care, integration of AI and analytics, and the adoption of cloud-based systems further contribute to the region’s leading market growth in online patient registry software.

| Report Matrics | Details |

| Market Size Value | USD 2.8 billion |

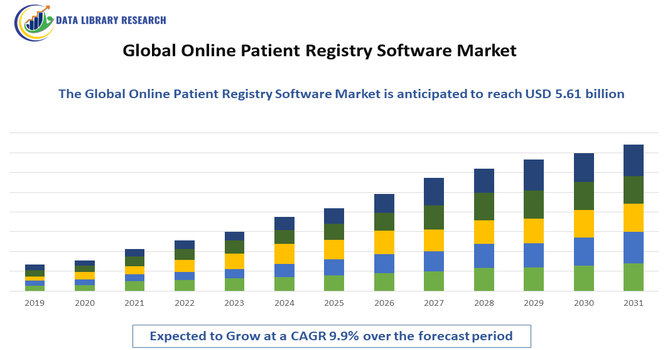

| Growth Rate | CAGR of 9.9 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global Online Patient Registry Software Market features a mix of established healthcare IT firms and specialized registry solution providers. Key players differentiate through advanced analytics, cloud deployment, and seamless EHR integration. Leading companies such as IQVIA, Dacima Software, Optum, ImageTrend, and ArborMetrix focus on broadening registry functionalities for research, clinical outcomes tracking, and real world evidence. Competition centers on improving interoperability, security, and user experience, while partnerships with healthcare providers and research organizations strengthen market presence. Innovation in AI driven data management, customizable modules, and subscription models enhances competitiveness as healthcare systems globally adopt digital registry platforms.

The major players for this market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The increasing demand for real-world evidence (RWE) to support drug approvals and safety surveillance is the primary driver. Additionally, the rising prevalence of chronic and rare diseases necessitates large-scale data collection for epidemiology and clinical research, pushing healthcare providers and pharmaceutical firms to adopt specialized online platforms.

Q2. What are the main restraining factors for this market?

Major restraints include the significant cost associated with implementing, maintaining, and integrating complex software systems into existing hospital infrastructure. Furthermore, stringent global data privacy regulations, such as HIPAA and GDPR, pose continuous compliance challenges, complicating cross-border data collection and sharing.

Q3. Which segment is expected to witness high growth?

The Disease Registries segment, specifically for rare and genetic disorders, is expected to see the highest growth. The complexity and low prevalence of these conditions require centralized, collaborative platforms to pool global patient data, which is essential for developing targeted diagnostics and personalized treatments that address unmet medical needs.

Q4. Who are the top major players for this market?

Top major players often include specialized health IT firms and large contract research organizations (CROs). Key names are IQVIA, known for its expansive registry services, PHARMASEAL, offering integrated clinical solutions, and Dassault Systèmes (Medidata), providing comprehensive clinical trial and patient data management software.

Q5. Which country is the largest player?

The United States (US) is the largest market player. This dominance stems from the country's huge healthcare expenditure, advanced digital health infrastructure, and high volume of pharmaceutical and biotech R&D activities, which heavily rely on extensive patient data and regulatory compliance via registry software.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model