Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The global oxygen and aerosol delivery devices market focuses on medical equipment designed to provide supplemental oxygen and aerosolized medications to patients with respiratory conditions. The growing prevalence of chronic respiratory diseases, increasing hospitalizations, and rising home healthcare demand drove adoption, supporting improved patient outcomes and treatment efficiency worldwide.

The growth of the global oxygen and aerosol delivery devices market was driven by the increasing prevalence of respiratory diseases such as COPD, asthma, and COVID-19-related complications, along with rising geriatric populations and air pollution exposure. Expanding hospital infrastructure, growing home healthcare adoption, and technological advancements in portable, user-friendly oxygen concentrators, nebulizers, and aerosol devices further fueled demand.

The global oxygen and aerosol delivery devices market has grown steadily due to rising prevalence of chronic respiratory diseases such as COPD and asthma. Portable oxygen concentrators and compact nebulizers gained traction as patients preferred convenient, home-use solutions. Innovations such as smart inhalers, digital dose tracking, and quieter, more efficient nebulizer systems enhanced usability. Adoption increased in both clinical and home-care settings, while integration with telemedicine platforms allowed remote monitoring and adherence tracking.

Segmentation: The market for oxygen and aerosol delivery devices is segmented by Product Type (Aerosol Delivery Devices (Nebulizers and Inhalers), Oxygen Delivery Devices (Oxygen Source Equipment and Oxygen Delivery Interfaces), Application (Chronic Obstructive Pulmonary Disease (COPD), Asthma, Cystic Fibrosis, Respiratory Distress Syndrome (RDS), and Other Respiratory Diseases), End-user (Hospitals and Clinics, Home Healthcare Settings and Ambulatory Surgical Centers), Distribution Channel (Retail Pharmacies, Hospital Pharmacies, and E-commerce/Online Channels), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The global oxygen and aerosol delivery devices market was strongly driven by the rising prevalence of respiratory illnesses such as chronic obstructive pulmonary disease (COPD), asthma, pneumonia, and COVID-19-related complications. For instance, in 2025, The Lancet reported that in 2021, there was an observed prevalence of asthma, with 3,340 cases per 100,000 people. Males who were below 20 years old had a greater prevalence of asthma. This report also stated that the prevalence of asthma is 9.1% among children, 11.0% among adolescents, and 6.6% among adults.

Also, the 2025, UN Environment Programme reported that, more than 99 percent of humanity is now breathing polluted air, leading to more than 8 million annual deaths, including more than 700,000 children under five. Rising exposure to polluted air increases respiratory illnesses such as asthma, COPD, and other lung disorders across all age groups, intensifying demand for oxygen therapy, inhalers, and nebulizers. Healthcare providers, hospitals, and home-care users will increasingly adopt these devices to manage pollution-induced respiratory conditions, prevent complications, and improve patient outcomes, thereby expanding both market size and technological innovation in respiratory care solutions worldwide. As, a result, demand for supplemental oxygen and aerosolized medication delivery devices surged in hospitals, clinics, and home-care settings.

Technological innovations significantly propelled the oxygen and aerosol delivery devices market. Manufacturers developed portable, lightweight, and energy-efficient oxygen concentrators and nebulizers, enhancing patient mobility and convenience. For instance, in December 2022, Kindeva Drug Delivery and Meridian Medical Technologies merged to create a global company specializing in drug-device combination products. The unified organization adopted the name Kindeva, with Meridian operating as “a Kindeva Company,” strengthening its position in the respiratory and drug delivery market.

Smart inhalers and digital dose-tracking devices enabled improved adherence to medication schedules and remote monitoring by healthcare providers. Integration of quieter, more efficient nebulizer mechanisms and multi-functional devices increased usability in both clinical and home-care environments. Additionally, devices with enhanced durability, battery life, and real-time performance feedback supported broader adoption.

Market Restraints:

The global oxygen and aerosol delivery devices market faced restraints due to high costs and limited accessibility, particularly in developing regions. Advanced portable oxygen concentrators, smart inhalers, and efficient nebulizers often required substantial investment, making them unaffordable for low-income patients and smaller healthcare facilities. Maintenance, replacement parts, and regulatory compliance further increased overall expenses. In addition, distribution challenges, inadequate healthcare infrastructure, and lack of awareness limited access in rural and remote areas. These factors constrained widespread adoption, slowing market penetration despite rising demand.

The growth of the oxygen and aerosol delivery devices market had significant socioeconomic effects, improving access to respiratory care and reducing hospital dependence. Portable and home-use devices enabled patients with chronic conditions to manage therapies effectively, improving quality of life and reducing healthcare costs. Widespread adoption supported aging populations and individuals affected by pollution-related respiratory illnesses, particularly in emerging regions. The market also generated employment opportunities in manufacturing, distribution, and healthcare services. By enhancing patient autonomy and enabling home-based care, these devices contributed to societal well-being, healthcare efficiency, and economic growth while promoting wider adoption of preventive and long-term respiratory health solutions.

Segmental Analysis:

The nebulizers segment was forecast to lead growth because the rising prevalence of chronic respiratory conditions, such as COPD, asthma, and cystic fibrosis, increased demand for effective aerosol based drug delivery. Portable, ultrasonic, and mesh nebulizers gained popularity for home based care, offering ease of use and improved medication delivery, especially among elderly and pediatric patients. As more patients preferred inhalation therapy over oral medications for lung diseases, and as home healthcare models expanded, nebulizers became a favored solution.

The COPD application segment was projected for strong growth because COPD remained a leading cause of chronic respiratory morbidity worldwide, especially amid aging populations, pollution, and smoking. Patients with COPD often required frequent, long-term inhalation therapy, making oxygen delivery devices and aerosol systems essential. Regular management and exacerbation prevention via nebulizers and inhalers drove demand among both hospital and home care users. As public health awareness grew and more diagnoses occurred, healthcare providers and patients increasingly adopted these devices to improve quality of life and reduce hospitalizations — elevating the COPD segment’s share in overall device demand.

Hospitals and clinics were expected to remain the largest and fastest-growing end-user segment because acute and severe respiratory conditions—such as COPD exacerbations, asthma attacks, pneumonia, and emergency breathing crises—required professional care and reliable aerosol delivery devices. Medical institutions invested in jet, ultrasonic, and mesh nebulizers for inpatient treatments, critical care, and emergency response. Bulk procurement, established procurement budgets, and regulatory compliance made hospitals major buyers of advanced aerosol and oxygen delivery equipment. As healthcare infrastructure expanded globally, particularly in developed and developing markets, hospital demand drove substantial growth for these devices.

The retail pharmacies (or outpatient / retail distribution) segment was poised for high growth because increasing self care, chronic disease management at home, and rising patient awareness led many to purchase inhalers and nebulizers directly for home use. As more people sought convenient, over the counter respiratory therapies for asthma, COPD, and other respiratory diseases, retail pharmacies became a key distribution channel. Additionally, the trend toward home healthcare and telemedicine encouraged patients to buy devices themselves rather than rely solely on institutional settings — boosting retail sales and broadening market reach globally.

North America was set to lead the market because of its mature healthcare infrastructure, high prevalence of respiratory diseases (COPD, asthma, etc.), and generous healthcare spending. Strong regulatory frameworks, favorable reimbursement policies, and well established distribution networks ensured wide access to oxygen and aerosol delivery devices.

Technological innovation from leading medical device manufacturers and high patient awareness further supported adoption. For instance, in April 2024, Teva partnered with Launch Therapeutics to accelerate development of its dual-action asthma rescue inhaler (ICS-SABA/TEV 248) and secured strategic development funding from Abingworth. These initiatives strengthened North America’s respiratory device pipeline, enhanced access to innovative asthma therapies, and reinforced the region’s leadership in advanced aerosol drug delivery solutions.

Furthermore, widespread chronic lung conditions and emphasis on preventive and outpatient respiratory care consolidated North America’s dominance in device demand and revenue contribution globally. For instance, in 2025, the Asthma and Allergy Foundation of America reported that in North America, high asthma prevalence among children—with 38.7% experiencing attacks and 44% remaining uncontrolled—boosted demand for oxygen and aerosol delivery devices. This drives market growth, emphasizing the need for effective respiratory care and advanced inhalation therapies.

| Report Matrics | Details |

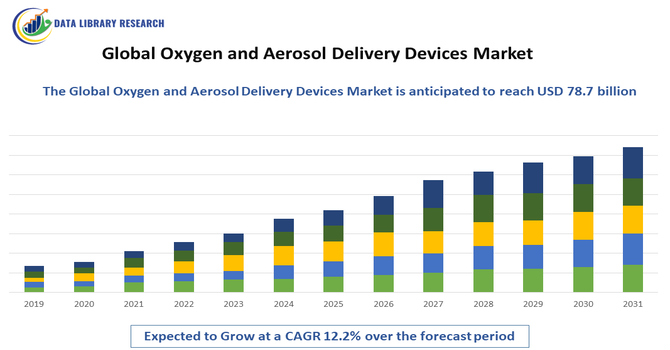

| Market Size Value | USD 42 billion |

| Growth Rate | CAGR of 12.2% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of oxygen and aerosol delivery devices was moderately consolidated, dominated by major global medical-device manufacturers offering comprehensive product portfolios. Companies competed through technological innovations, including portable oxygen concentrators, mesh nebulizers, and smart inhalers with digital monitoring. Strategic collaborations with pharmaceutical firms, focus on regulatory compliance, and emphasis on product reliability strengthened market positions. Research and development investments enabled advancements in usability, energy efficiency, and patient-centric design.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The main driver is the rising global rate of chronic respiratory illnesses, especially Asthma and Chronic Obstructive Pulmonary Disease (COPD). Factors like increasing air pollution and a growing elderly population prone to these diseases fuel device demand. Additionally, the increasing focus on convenient home healthcare and portable devices encourages market expansion.

Q2. What are the main restraining factors for this market?

Key restraining factors include the high cost of advanced delivery devices, such as modern mesh nebulizers, limiting access in lower-income areas. Complex and unfavorable reimbursement policies in some countries also hinder adoption. Lastly, technical issues like inconsistent drug deposition or potential side effects can sometimes restrict market growth.

Q3. Which segment is expected to witness high growth?

The Nebulizers segment, particularly advanced Vibrating Mesh Nebulizers, is expected to see the highest growth. Patients and healthcare providers prefer them due to their portability, quiet operation, and precise medication delivery. This technology makes sophisticated aerosol therapy easier and more comfortable for use in home-care settings.

Q4. Who are the top major players for this market?

The market is competitive, featuring major healthcare and medical device companies. Top players include Koninklijke Philips N.V., OMRON Corporation, PARI GmbH, and pharmaceutical giants like AstraZeneca and GlaxoSmithKline (GSK). These companies focus on technological innovation, especially in smart and portable inhalation devices.

Q5. Which country is the largest player?

North America holds the largest market share, with the United States being the dominant country player. This leadership is driven by the high prevalence of respiratory diseases, advanced healthcare infrastructure, and favorable reimbursement policies for respiratory care devices. However, Asia Pacific is the fastest-growing region.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model