Get Complete Analysis Of The Report - Download Updated Free Sample PDF

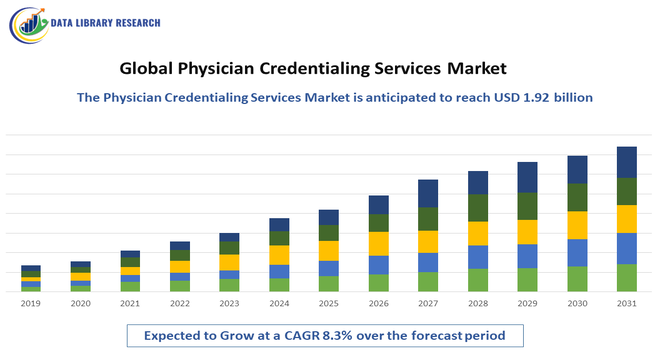

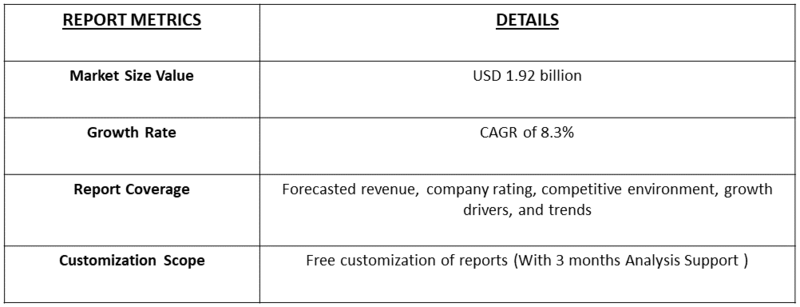

The Global Physician Credentialing Services Market involves the provision of services that verify, evaluate, and maintain physicians’ qualifications, licenses, and professional backgrounds. It ensures compliance with regulatory standards, hospital requirements, and insurance mandates. Driven by growing healthcare regulations, digitalization, and the need for operational efficiency, the market supports risk management, patient safety, and streamlined onboarding of medical professionals worldwide.

The growth of the Global Physician Credentialing Services Market has been driven by increasing healthcare regulations, the need for compliance with accreditation standards, and the growing emphasis on patient safety and quality care. Rising healthcare infrastructure and hospital expansions, combined with the adoption of digital credentialing platforms, have streamlined verification processes, reduced administrative burdens, and minimized errors.

The global physician credentialing services market is gaining momentum, driven primarily by stricter regulatory compliance demands, the growth of telehealth platforms crossing jurisdictional boundaries, and hospitals’ push to streamline onboarding of a growing and mobile medical workforce. Adoption of digital and cloud based solutions, along with artificial intelligence and data analytics tools, is accelerating to improve speed and accuracy of credential verification and ongoing monitoring. Technology shifts—such as integration with electronic health records and use of automated workflows—are replacing manual processes, while outsourcing of credentialing to specialised providers is increasing in response to cost and time pressures.

Segmentation: The Global Physician Credentialing Services Market can be segmented by Service Type (Offerings (Primary Source Verification, Credentialing Software‐Solutions, and Managed Services Or Outsourcing), Deployment (On Premises, Cloud Based, and Hybrid Models), End User (Hospitals, Physician Groups/Clinics, Healthcare Networks and Organizations, Insurance Companies and Other Healthcare Providers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The global physician credentialing services market is being strongly propelled by increasingly stringent regulatory and accreditation requirements in healthcare. Hospitals, clinics, and healthcare networks are obligated to verify the qualifications, experience, and licensure of physicians to comply with standards set by bodies such as The Joint Commission, the National Committee for Quality Assurance (NCQA), and government health authorities.

In March 2025, Medallion expanded its automated credentialing and privileging capabilities to support Joint Commission standards, including electronic workflows and automated application submissions. This improved efficiency, reduced errors, and accelerated physician onboarding, boosting demand for technology-driven solutions and positively impacting the global physician credentialing services market. Failure to adhere to these regulations can lead to legal repercussions, financial penalties, or reputational damage. As healthcare delivery becomes more complex and patient safety demands rise, institutions are investing heavily in credentialing solutions that ensure timely verification, continuous monitoring, and accurate documentation.

The rapid expansion of telemedicine and cross-border healthcare services is significantly driving the demand for physician credentialing services worldwide. As healthcare providers deliver services remotely across state and national boundaries, ensuring that physicians meet local licensing requirements and maintain verified credentials becomes essential. Telehealth platforms, especially post-pandemic, require faster, accurate, and compliant credential verification to onboard medical professionals efficiently. Digital solutions, AI-enabled verification, and cloud-based platforms facilitate this process, allowing seamless credentialing regardless of geographical constraints.

Market Restraint:

Despite market growth, high costs and operational complexities restrain adoption of physician credentialing services. Traditional credentialing processes are often labor-intensive, requiring verification from multiple primary sources, documentation review, and ongoing monitoring, which can lead to delays and errors. Even automated and outsourced solutions demand substantial financial investment in software, staff training, and integration with existing hospital systems. Smaller healthcare facilities and clinics, particularly in emerging markets, may find these costs prohibitive, limiting their ability to adopt comprehensive credentialing services.

The growing global physician credentialing services market has tangible socioeconomic impacts: by facilitating faster and more reliable verification of physician qualifications, it helps healthcare facilities reduce administrative overhead and enable qualified practitioners to start work sooner, thereby expanding access to care—especially in underserved or rural regions where timely onboarding of physicians can make a critical difference. At the same time, the automation and outsourcing of credentialing processes can free up medical staff to focus more on patient care rather than paperwork, improving productivity and potentially reducing burnout. Conversely, if credentialing is delayed or inefficient, it can escalate costs for smaller clinics, hinder physician mobility, and exacerbate disparities in healthcare access, thereby placing greater strain on public health systems and increasing inequality in service delivery.

Segmental Analysis:

The primary source verification segment of the global physician credentialing services market is anticipated to witness substantial growth during the forecast period, driven by the increasing emphasis on patient safety and regulatory compliance. Healthcare institutions are mandated to verify credentials directly from issuing authorities, such as medical schools, licensing boards, and professional associations, to ensure authenticity. Automated and digital verification platforms are streamlining this process, reducing manual effort, errors, and delays. The rising adoption of telemedicine, cross-border healthcare, and multi-hospital networks further fuels demand, as organizations seek reliable and standardized verification processes to onboard physicians efficiently while maintaining compliance with local and international regulations.

The on-premises deployment segment of the physician credentialing services market is projected to experience notable growth, primarily due to healthcare organizations’ preference for greater control over sensitive data and internal credentialing processes. Hospitals and large healthcare networks often require in-house systems to integrate seamlessly with existing electronic health records (EHRs) and IT infrastructure, ensuring secure and customized workflows. The ability to manage credentialing internally allows for faster decision-making, tailored reporting, and reduced reliance on external vendors. Additionally, regulatory compliance concerns and data privacy requirements in regions with strict healthcare laws support the adoption of on-premises solutions over cloud-based alternatives, contributing to sustained market expansion.

The cloud-based segment of the physician credentialing services market is anticipated to grow rapidly, fueled by increasing demand for scalable, flexible, and cost-efficient solutions. Cloud platforms enable healthcare providers to access credentialing data remotely, streamline application and re-credentialing processes, and ensure real-time updates of physician qualifications. Integration with telemedicine platforms and multi-facility networks allows centralized management across regions, reducing administrative burden and turnaround time. Furthermore, advancements in AI and data analytics enhance the accuracy and speed of credential verification, making cloud solutions attractive for both large hospitals and smaller clinics. The ease of deployment, lower upfront costs, and continuous software updates support sustained adoption globally.

The healthcare networks and organizations segment is projected to witness robust growth in the physician credentialing services market, driven by the increasing consolidation of hospitals, clinics, and specialty centers. These networks require standardized and centralized credentialing processes to ensure consistency, regulatory compliance, and patient safety across multiple facilities. The adoption of automated and outsourced credentialing services enables faster onboarding, reduces administrative overhead, and supports operational efficiency. Additionally, the expansion of telehealth services and multi-site operations necessitates reliable verification of physician qualifications across different regions. As healthcare organizations focus on improving quality of care and minimizing risk, demand for comprehensive credentialing services within large networks continues to rise.

North America is expected to remain the largest and fastest-growing market for physician credentialing services, driven by a mature healthcare infrastructure, stringent regulatory requirements, and widespread adoption of digital solutions. The region’s hospitals, clinics, and healthcare networks are under constant pressure to comply with The Joint Commission, NCQA, and state licensing standards, which necessitate robust credentialing processes.

Advanced adoption of electronic health records, cloud-based platforms, and AI-enabled verification tools supports faster and more accurate credentialing. Additionally, the growth of telemedicine and multi-state physician networks further fuels demand. For instance, in June 2024, iRCM Inc., a leading medical billing company, announced its comprehensive suite of end-to-end medical billing and credentialing services across the United States. Addressing administrative challenges faced by medical practitioners, iRCM provided solutions to optimize revenue, enhance risk management, and ensure accurate provider enrollment and credentialing. Its services, including medical coding, contract negotiation, EHR/EMR integration, and clinical quality improvement, covered over 40 medical specialties. This expanded service offering strengthened operational efficiency and adoption of credentialing solutions, significantly contributing to the growth of North America’s physician credentialing services market. Also, the high awareness of patient safety, coupled with continuous healthcare investments, ensures sustained expansion of credentialing services across North America.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global physician credentialing services market is moderately fragmented, with established players like Symplr, HealthStream, VerityStream, Cactus Software, and CredentialMyDoc dominating through comprehensive service portfolios and large healthcare client bases. Companies compete by integrating advanced technologies such as AI, machine learning, and blockchain, while offering end-to-end services including primary source verification, provider enrollment, compliance monitoring, and managed services. Niche and regional vendors differentiate with specialized offerings, cost-effective pricing, and flexible deployment models. Strategic initiatives like mergers, acquisitions, partnerships, and geographic expansion are common, with innovation, faster onboarding, and integrated workflows emerging as key factors for maintaining a competitive edge.

The 20 major players for the above market are:

Recent Development

Q1. What the main growth driving factors for this market?

The primary growth driver is the increasing complexity and volume of healthcare regulatory compliance required to ensure patient safety and quality of care. Healthcare institutions must continuously verify provider qualifications, licenses, and certifications from various sources, a time-consuming and error-prone manual process. The growth of the overall healthcare workforce and the need for efficient provider enrollment with insurance payers also significantly drives demand for specialized services and automated software that streamlines these essential administrative tasks.

Q2. What are the main restraining factors for this market ?

A key restraining factor is the high initial cost and complexity of implementing advanced credentialing software and integrating it with existing hospital management systems, Electronic Health Records (EHR), and HR databases. This substantial investment and the challenge of data integration can be prohibitive for smaller medical practices and clinics. Furthermore, the sensitive nature of personal health and professional data raises ongoing concerns about data security and privacy compliance (like HIPAA), requiring continuous and costly system maintenance.

Q3. Which segment is expected to witness high growth?

The Cloud-Based Deployment segment is expected to witness the highest growth. Cloud solutions offer superior scalability, accessibility, and cost-effectiveness compared to traditional on-premise systems, making them highly attractive to organizations of all sizes, including growing telemedicine providers. The integration of Artificial Intelligence (AI) and automation within these cloud platforms allows for faster primary source verification and re-credentialing, drastically reducing processing times and human error.

Q4. Who are the top major players for this market?

The market is led by technology and service providers specializing in healthcare IT and revenue cycle management. Top major players include companies that offer integrated provider management platforms, such as symplr, Verisys (now part of Verifiable), and companies focused on automation like IntelliCentrics. Other significant contributors are firms specializing in medical billing and Revenue Cycle Management (RCM) that offer credentialing as a critical service, such as CureMD and various specialized medical billing companies.

Q5. Which country is the largest player?

North America, primarily the United States, holds the largest market share in the Physician Credentialing Services Market. This dominance is due to a highly advanced and regulated healthcare infrastructure, strict compliance mandates from bodies like The Joint Commission and CMS, and the high adoption rate of health IT solutions. The US also has a complex, fragmented system of insurance payers, which makes outsourcing credentialing services a necessity for most hospitals and individual practices.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model