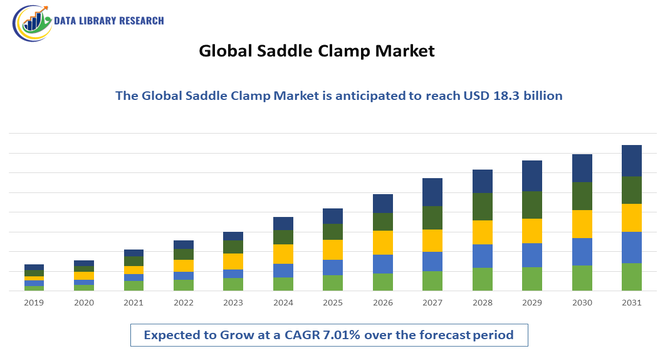

The Global Saddle Clamp Market size was valued at USD 6.76 billion in 2026, and this market is expected to reach to USD 18.3 billion in 2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Saddle Clamp Market refers to the production, distribution, and application of saddle clamps used to secure pipes, tubes, and cables onto surfaces or support structures. These clamps are widely utilized in plumbing, construction, automotive, oil and gas, and industrial sectors to provide stability and prevent movement or vibration. Manufactured from materials such as stainless steel, carbon steel, plastic, and aluminum, saddle clamps are available in various sizes and load-bearing capacities. Growing infrastructure development, industrialization, and maintenance activities drive demand. The market supports safe pipeline installations and efficient mechanical fastening solutions across residential, commercial, and industrial applications worldwide.

The Saddle Clamp Market is witnessing trends such as increasing demand for corrosion-resistant and lightweight materials, particularly stainless steel and advanced polymers. Manufacturers are focusing on durable, easy-to-install designs to reduce labor costs and improve efficiency. The growth of infrastructure projects, smart cities, and renewable energy installations is boosting product innovation. Customization based on pipe diameter, load requirements, and environmental conditions is gaining traction. Additionally, automation in manufacturing processes and digital supply chain integration enhance production efficiency. Sustainability trends are encouraging eco-friendly materials and recyclable components. These factors collectively shape product development and competitive strategies in the global saddle clamp market.

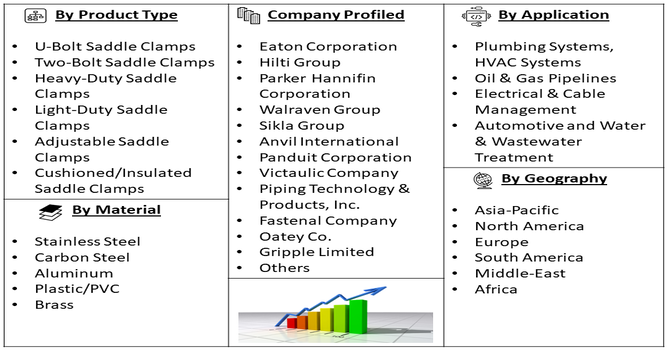

Segmentation: The Saddle Clamp Market is segmented by Product Type (U-Bolt Saddle Clamps, Two-Bolt Saddle Clamps, Heavy-Duty Saddle Clamps, Light-Duty Saddle Clamps, Adjustable Saddle Clamps and Cushioned/Insulated Saddle Clamps), Material (Stainless Steel, Carbon Steel, Aluminum, Plastic/PVC and Brass), Application (Plumbing Systems, HVAC Systems, Oil & Gas Pipelines, Electrical & Cable Management, Automotive and Water & Wastewater Treatment), Distribution Channel (Direct Sales (B2B), Distributors & Wholesalers, Retail Hardware Stores, and Online Sales Platforms), Load Capacity (Light Load, Medium Load and Heavy Load), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Rapid urbanization and infrastructure development are major drivers of the Saddle Clamp Market. Increasing investments in residential, commercial, and industrial construction projects require reliable pipe and cable fastening systems. Expanding water supply networks, wastewater treatment facilities, and energy distribution systems further boost demand. Governments worldwide are investing heavily in transportation, smart cities, and utility modernization, driving large-scale installations. Saddle clamps ensure secure mounting and structural integrity, making them essential components in these projects. Additionally, maintenance and renovation activities in aging infrastructure create consistent replacement demand. The continuous expansion of construction activities globally significantly accelerates market growth.

The expansion of oil and gas, petrochemical, and heavy industrial sectors significantly drives demand for saddle clamps. These industries require robust, vibration-resistant, and corrosion-proof fastening solutions for pipelines and tubing systems operating under high pressure and harsh environmental conditions. Increasing energy demand and exploration activities in emerging economies stimulate infrastructure installations. Industrial automation and plant expansions also contribute to rising clamp usage. Manufacturers are developing high-strength clamps capable of withstanding extreme temperatures and chemical exposure. The need for safety compliance and operational efficiency further enhances adoption, positioning industrial growth as a critical factor supporting the saddle clamp market globally.

Market Restraints:

Fluctuations in raw material prices, particularly steel and aluminum, pose a significant restraint for the Saddle Clamp Market. Since these materials constitute a major portion of production costs, price volatility impacts profit margins and overall product pricing. Manufacturers may face challenges in maintaining competitive pricing, especially in cost-sensitive markets. Additionally, supply chain disruptions and trade restrictions can increase procurement costs. Smaller manufacturers are particularly vulnerable to sudden price spikes, affecting their operational stability. These uncertainties may delay infrastructure projects or reduce demand in certain regions, limiting consistent growth and creating financial pressure across the supply chain.

The Saddle Clamp Market contributes significantly to infrastructure development, industrial safety, and economic growth. By ensuring stable and secure pipe and cable installations, saddle clamps enhance operational efficiency across construction, oil and gas, water management, and manufacturing sectors. The market supports employment in manufacturing, logistics, and distribution channels globally. In developing economies, growing infrastructure projects stimulate demand, promoting local industrialization. Reliable fastening solutions reduce maintenance costs and improve safety standards, positively impacting businesses and communities. However, raw material price fluctuations may affect affordability. Overall, the market underpins essential infrastructure systems, contributing to improved living standards and industrial productivity worldwide.

Segmental Analysis:

The Heavy-Duty Saddle Clamps segment is expected to witness the highest growth due to increasing demand from infrastructure, oil and gas, and industrial sectors requiring robust pipe support solutions. These clamps are designed to withstand high pressure, vibration, and harsh environmental conditions, making them ideal for large-diameter pipelines and heavy-load applications. Rapid industrialization and expansion of energy projects globally further drive demand. Additionally, stringent safety regulations in construction and pipeline installations encourage the adoption of high-strength fastening components. As industries prioritize durability, reliability, and long-term performance, heavy-duty saddle clamps are projected to experience substantial growth over the forecast period.

The Stainless-Steel segment is projected to witness the highest growth owing to its superior corrosion resistance, durability, and strength. Stainless steel saddle clamps are widely preferred in oil and gas, marine, and water treatment applications where exposure to moisture and chemicals is common. Growing infrastructure projects in coastal and industrial regions further boost demand for corrosion-resistant materials. Additionally, stainless steel offers long service life and reduced maintenance costs, making it cost-effective over time. Increasing regulatory standards emphasizing safety and material reliability also contribute to its adoption, positioning stainless steel as the fastest-growing material segment in the market.

The Oil & Gas Pipelines segment is expected to experience the highest growth due to expanding exploration, production, and transportation activities worldwide. Saddle clamps play a critical role in securing pipelines under high pressure and extreme environmental conditions. Rising global energy demand and new pipeline infrastructure projects in emerging economies are key growth drivers. Maintenance and replacement of aging pipeline networks further stimulate demand. Additionally, strict safety and compliance standards in the oil and gas industry require reliable fastening solutions. These factors collectively position the oil and gas pipelines segment as a leading contributor to saddle clamp market growth.

The Distributors & Wholesalers segment is projected to witness the highest growth as large-scale construction and industrial projects rely on bulk procurement channels. Distributors provide a wide product range, competitive pricing, and efficient supply chain management, making them essential for contractors and industrial buyers. Their established networks enable timely delivery and technical support, especially in remote or developing regions. Growing infrastructure investments and industrial expansion increase reliance on organized distribution systems. Additionally, partnerships between manufacturers and regional distributors strengthen market penetration. This efficient procurement model positions distributors and wholesalers as a rapidly growing distribution channel.

The Medium Load segment is expected to witness the highest growth due to its broad applicability across residential, commercial, and light industrial installations. Medium load saddle clamps offer a balance between strength and cost-effectiveness, making them suitable for plumbing, HVAC, and cable management systems. Increasing urbanization and commercial building projects drive demand for moderate-capacity fastening solutions. These clamps provide sufficient support for standard pipelines without the higher costs associated with heavy-duty variants. As infrastructure development expands globally, the versatility and affordability of medium load clamps are anticipated to fuel steady and significant growth throughout the forecast period.

The Asia-Pacific region is projected to witness the highest growth in the saddle clamp market due to rapid urbanization, industrialization, and infrastructure development. Countries such as China, India, Japan, and Southeast Asian nations are investing heavily in construction, energy, and water management projects. Expanding manufacturing industries and growing oil and gas pipeline installations further stimulate demand. Government initiatives supporting smart cities and industrial corridors enhance infrastructure expansion. Additionally, the presence of cost-effective manufacturing facilities and increasing foreign investments contribute to market growth. These combined factors position Asia-Pacific as the fastest-growing regional market over the forecast period.

| Report Matrics | Details |

| Market Size Value | USD 18.3 billion |

| Growth Rate | CAGR of 7.01% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global Saddle Clamp Market is characterized by the presence of multinational manufacturers and regional players competing on quality, price, and product innovation. Companies emphasize corrosion resistance, strength, and compliance with international safety standards. Strategic partnerships with construction firms, distributors, and industrial contractors strengthen market reach. Many players focus on expanding product portfolios and enhancing manufacturing efficiency through automation. Price competitiveness and bulk supply capabilities influence purchasing decisions in large-scale projects. Emerging players often compete by offering customized solutions. Geographic expansion into high-growth regions further intensifies competition, with companies prioritizing durability, reliability, and customer service excellence.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

Rapid urbanization and the aging of municipal water infrastructure are the primary drivers. Cities globally are upgrading piping systems to reduce leakage, where saddle clamps provide efficient, "hot-tap" connections without service interruptions. Additionally, the expansion of the oil and gas sector and increased irrigation projects in developing nations boost demand.

Q2. What are the main restraining factors for this market?

Fluctuating raw material prices, particularly for stainless steel, ductile iron, and specialized polymers, create pricing instability for manufacturers. Furthermore, the availability of alternative joining methods, such as electrofusion or mechanical couplings in specific high-pressure applications, limits market penetration. Strict environmental regulations regarding material coatings also increase production complexities and costs.

Q3. Which segment is expected to witness high growth?

The Stainless Steel segment is expected to witness the highest growth over the forecast period due to its superior corrosion resistance, high tensile strength, and long service life. Increasing demand from oil & gas, marine, construction, and water treatment industries is driving adoption of stainless steel saddle clamps for reliable, durable performance.

Q4. Who are the top major players for this market?

The market features prominent industrial manufacturers including Mueller Water Products, Victaulic, and AVK Group. Other significant players include Georg Fischer (GF Piping Systems), Saint-Gobain, and Smith-Blair (Xylem). These companies maintain their lead through extensive distribution networks and the development of corrosion-resistant, easy-to-install clamping solutions for diverse industries.

Q5. Which country is the largest player?

China is the largest player in the global market, both as a leading producer and a massive consumer. This dominance is fueled by aggressive infrastructure development, massive investments in wastewater treatment facilities, and a robust manufacturing base that exports cost-effective saddle clamp solutions to various international markets across Asia and Africa.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model