Get Complete Analysis Of The Report - Download Updated Free Sample PDF

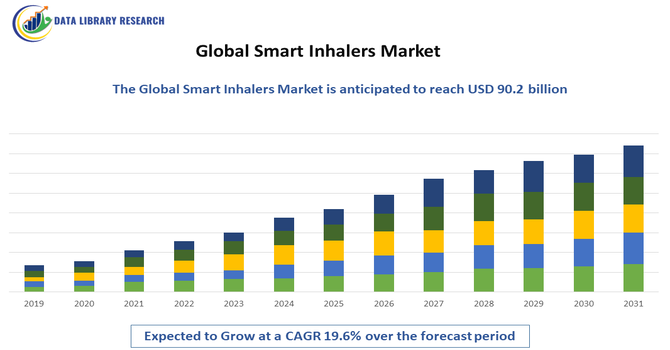

The Global Smart Inhalers Market comprises connected inhaler devices integrated with sensors, mobile apps, and IoT technology to monitor usage, improve medication adherence, and manage chronic respiratory diseases like asthma and COPD. Growth is driven by rising respiratory disease prevalence, digital health adoption, telemedicine expansion, and demand for personalized, real-time patient care. Additionally, increasing awareness of the economic and health benefits of improved medication adherence, along with supportive regulatory frameworks and reimbursement policies, has fueled market expansion.

The Global Smart Inhalers Market experienced rapid innovation as connected devices, IoT integration, and mobile health apps became mainstream. Adoption of digital health platforms enabled real time monitoring of usage patterns, adherence tracking, and remote patient management. Integration with wearables and cloud analytics enhanced personalized care and clinical decision support. Telemedicine growth further accelerated smart inhaler utilization, especially in chronic respiratory diseases like asthma and COPD. Partnerships between device manufacturers and software developers intensified to improve user experience and data security. Additionally, regulatory support for digital therapeutics and reimbursement frameworks gradually emerged, positioning smart inhalers as a key component of value based respiratory healthcare worldwide.

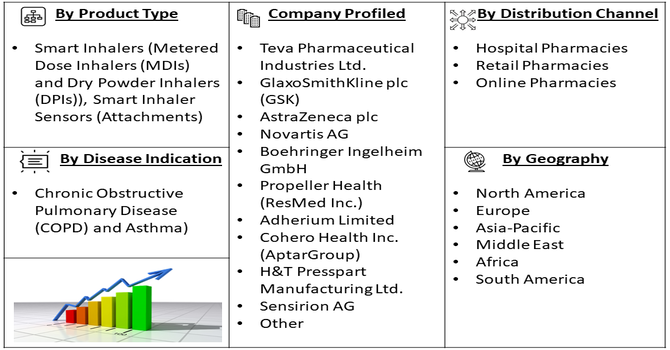

Segmentation: The Smart Inhalers Market is segmented by Product Type (Smart Inhalers (Metered Dose Inhalers (MDIs) and Dry Powder Inhalers (DPIs)), Smart Inhaler Sensors (Attachments)), Disease Indication (Chronic Obstructive Pulmonary Disease (COPD) and Asthma), Distribution Channel (Hospital Pharmacies, Retail Pharmacies and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The primary driver of the smart inhalers market was the growing prevalence of respiratory diseases such as asthma and chronic obstructive pulmonary disease (COPD), which increased demand for effective management solutions. For instance, WHO in 2024, reported that, globally, the prevalence of COPD is estimated at approximately 480–500 million people, representing around 10.6% of the population. Projections indicate that by 2050, the number of cases is expected to rise to roughly 592 million, marking a 23.3% increase from 2020. Similarly, asthma affected an estimated 262 million people in 2019. Higher disease burden increases demand for effective management solutions, including metered dose and smart inhalers, to improve adherence, monitor usage, and reduce hospitalizations. The expanding patient base encourages pharmaceutical companies and healthcare providers to adopt advanced inhaler technologies, integrate digital monitoring, and invest in patient education programs.

A second driver was the rapid expansion of digital health technologies, including IoT connectivity and mobile apps, enabling real time monitoring, data sharing, and personalized feedback. These innovations supported remote care models and aligned with value based healthcare objectives. In February 2023, Teva Pharmaceuticals’ presentation of Digihaler System data, including real-world and clinical trial insights, highlighted the benefits of smart inhalers with built-in sensors for personalized asthma management. This reinforced the rapid expansion of digital health technologies and boosted adoption within the Global Smart Inhalers Market by demonstrating improved patient monitoring and treatment outcomes. Additionally, supportive initiatives from healthcare providers and payers to encourage adherence and reduce long term costs further propelled smart inhaler adoption globally.

Market Restraints:

A significant restraint in the smart inhalers market was data privacy and regulatory concerns associated with connected health devices. As smart inhalers collected and transmitted sensitive patient information, stringent data protection laws, complex compliance requirements, and cybersecurity risks posed barriers to widespread adoption. Healthcare providers and patients often hesitated due to fears of data breaches and inadequate digital literacy. Furthermore, inconsistencies in reimbursement policies across regions limited financial incentives for adoption. Smaller healthcare facilities and low resource settings faced challenges in integrating advanced digital systems.

The Global Smart Inhalers Market contributed positively to healthcare outcomes and economic efficiency. By improving medication adherence and reducing exacerbations, smart inhalers lowered hospitalizations, emergency visits, and associated healthcare costs. Enhanced disease management empowered patients with better self care, improving the quality of life for millions with chronic respiratory conditions. The market also generated high-skilled employment in technology, clinical support, and data analytics sectors. In developing regions, smart inhaler adoption highlighted disparities in healthcare access, prompting investments in digital infrastructure. As a result, insurers and health systems increasingly recognized long term cost savings, fostering broader acceptance of connected health solutions and promoting preventive medicine paradigms.

Segmental Analysis:

The Metered Dose Inhalers (MDIs) segment is projected to witness the highest growth over the forecast period due to their widespread use, ease of administration, and cost-effectiveness. MDIs are preferred by patients for precise dosing and portability, making them suitable for both chronic and acute respiratory conditions.

Increasing awareness about proper inhaler techniques and adherence to prescribed therapy is driving adoption. For instance, In November 2024, the European Medicines Agency (EMA) released the COMP-AIR protocol to evaluate the comparative effectiveness of combination inhalers such as Fostair and Symbicort. These assessments guided optimal treatment strategies, enhancing the adoption and credibility of Metered Dose Inhalers (MDIs) by supporting evidence-based clinical decisions for asthma management. Additionally, their compatibility with smart inhaler technologies supports patient monitoring and data collection, positioning MDIs as a leading segment in respiratory care.

The asthma segment is expected to register the highest growth over the forecast period, driven by the rising global prevalence of the condition, especially among children and adults in urban regions. Increasing environmental pollution, changing lifestyles, and heightened allergen exposure are contributing to higher asthma incidence. Growing awareness of disease management and adherence to prescribed therapies is boosting demand for advanced inhaler devices. The development of smart inhalers that track usage, improve compliance, and enable real-time monitoring is enhancing patient outcomes. These factors collectively position the asthma segment as a key growth driver in the respiratory devices market.

The retail pharmacies segment is anticipated to witness the highest growth over the forecast period, driven by the convenience, accessibility, and wide availability of inhalers and related respiratory devices. Retail pharmacies serve as the primary channel for patients to obtain prescribed medications and increasingly offer pharmacist-led guidance on device usage.

The expansion of retail chains, combined with rising consumer awareness of respiratory health and digital health solutions, has increased footfall and sales. Integration of smart inhaler programs with pharmacy services further encourages adherence monitoring and patient support. Consequently, retail pharmacies are emerging as a pivotal distribution and education channel in the smart inhalers market.

The North America segment is projected to experience the highest growth over the forecast period, driven by the region’s high prevalence of chronic respiratory diseases, strong healthcare infrastructure, and widespread adoption of digital health technologies. Patients and healthcare providers increasingly prefer smart inhalers for asthma and COPD management due to their ability to monitor adherence and provide actionable data.

Supportive government regulations, reimbursement policies, and advanced research initiatives further accelerate adoption. For instance, in September 2023, CDC reported that, Asthma affected over 25 million Americans, including 4.2 million children, with disproportionate impact on Medicaid enrollees. Enhanced accessibility to guidelines-based treatments and improved Medicaid coverage across all states have supported better asthma management. These developments in reimbursement policies and increased treatment accessibility are driving adoption of smart inhalers in North America, boosting the Global Smart Inhalers Market by encouraging adherence, monitoring, and improved patient outcomes.

Additionally, the presence of major pharmaceutical and medical device companies in the region ensures continuous product innovation, making North America a key market for smart inhaler growth and technology integration. For instance, in August 2025, the FDA approved multiple generic metered-dose inhalers (MDIs) with eco-friendly green propellants, promoting reduced environmental impact. This initiative supported North America’s smart inhaler market by encouraging adoption of sustainable devices, aligning with regulatory priorities, and increasing patient and provider preference for environmentally responsible respiratory care solutions.

Thus, such factors are driving the growth of this market in this region.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Smart Inhalers Market featured key medical device manufacturers and technology firms vying for market share through innovation and strategic collaborations. Established pharmaceutical and inhaler producers partnered with digital health companies to integrate sensors, connectivity, and analytics into traditional devices. New entrants specializing in software and telehealth platforms drove differentiation by enhancing user interfaces and predictive insights. Mergers, acquisitions, and co development agreements were common as companies sought to expand product portfolios and global reach. Emphasis on regulatory approvals, clinical validation, and scalable solutions influenced competitive positioning. Regional players focused on localized solutions, while global leaders leveraged strong distribution networks to maintain dominance in major healthcare markets.

The major players for this market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is primarily driven by the rising global prevalence of chronic respiratory diseases, such as asthma and COPD. Smart inhalers significantly improve medication adherence and proper technique, which are critical issues in managing these conditions. Additionally, the rapid integration of digital health and remote patient monitoring systems fuels growth.

Q2. What are the main restraining factors for this market?

The key restraint is the high cost of the smart inhaler devices compared to traditional inhalers, which limits adoption, especially in lower-income regions. Furthermore, patient concerns regarding data privacy and the security of their personal health information collected by the connected devices create resistance and slow down widespread acceptance.

Q3. Which segment is expected to witness high growth?

The Asthma segment is anticipated to witness the highest market growth due to the immense global prevalence of the condition, particularly among children. Smart inhalers provide critical, real-time data on poor adherence and incorrect technique, which are major contributors to asthma-related hospitalizations. By improving patient compliance and enabling timely intervention through connected apps, these devices significantly reduce healthcare costs, driving massive adoption by payers and providers worldwide.

Q4. Who are the top major players for this market?

Major global pharmaceutical and medical device companies dominate the market. Key players include Teva Pharmaceutical Industries Ltd., GlaxoSmithKline (GSK), and Novartis AG, alongside specialist digital health companies like Propeller Health and Adherium Ltd. These firms are focused on R&D and strategic partnerships to integrate technology.

Q5. Which country is the largest player?

North America, led by the United States, holds the largest market share in terms of revenue. This dominance is due to the high prevalence of COPD and asthma, advanced healthcare IT infrastructure, high levels of patient and clinician awareness, and favorable reimbursement policies for connected medical devices.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model