Get Complete Analysis Of The Report - Download Updated Free Sample PDF

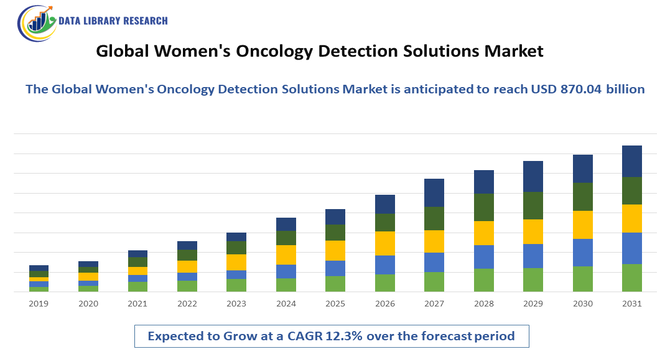

The global Women’s Oncology Detection Solutions market focuses on technologies and tools designed to detect cancers that primarily affect women, such as breast, ovarian, and cervical cancers. It includes advanced diagnostic methods like imaging, molecular testing, and AI-powered screening that help identify cancer early and accurately. This market plays a crucial role in improving women’s health by enabling timely diagnosis and personalized treatment options worldwide.

The Women’s Oncology Detection Solutions market is experiencing significant growth fueled by several key trends. Advances in artificial intelligence and machine learning are revolutionizing diagnostic accuracy, enabling earlier and more precise detection of cancers such as breast, ovarian, and cervical. The increasing use of liquid biopsies and comprehensive genomic profiling allows for more personalized and targeted treatment plans.

Additionally, the development of portable, minimally invasive, and point-of-care diagnostic devices is expanding access to cancer screening, especially in underserved and remote areas. Rising awareness about women’s health, coupled with strong government initiatives and increased funding for cancer research, is further accelerating the adoption of innovative detection technologies. These trends collectively are shaping a more patient-centric approach in women’s oncology diagnostics, improving outcomes and broadening market opportunities globally.

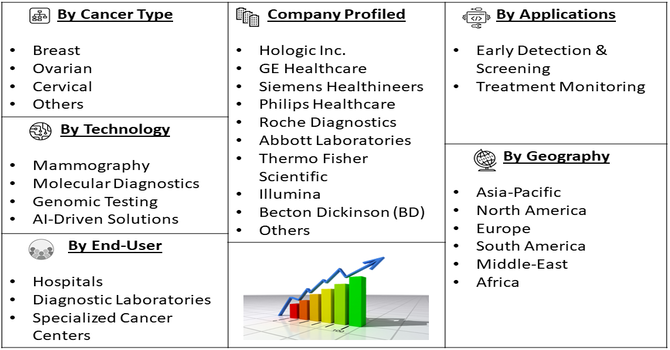

Segmentation: The Women’s Oncology Detection Solutions market is Segmented by Cancer Types (Breast, Ovarian, Cervical, and Others), Technology (Mammography, Molecular Diagnostics, Genomic Testing, and AI-Driven Solutions.), Applications (Early Detection & Screening and Treatment Monitoring), End-Users (Hospitals, Diagnostic Laboratories, and Specialized Cancer Centers) and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The primary drivers of the Women’s Oncology Detection Solutions market is the increasing incidence of women-specific cancers such as breast, ovarian, and cervical cancer globally. Factors like lifestyle changes, aging populations, and genetic predispositions have contributed to a rise in cancer cases. Early detection of these cancers significantly improves survival rates and treatment outcomes, which has increased the demand for advanced and accurate diagnostic solutions.

In October 2024, an article published in NCBI, reported that in the year 2021, adolescent and young adult (AYA) females were diagnosed with 383,241 new cancer cases. The article also highlighted that cancer statistics from 2022 showed that female-specific cancers ranked within the top 10 in incidence rates among women, collectively accounting for 38.3% of all cancers in females. Breast cancer was the most commonly diagnosed cancer among women, with nearly 2.3 million new cases reported in 2022, making it the second most prevalent cancer after lung cancer. Thus, this rising prevalence and emphasis on early detection are pushing the development and adoption of innovative technologies like molecular diagnostics, imaging, and AI-driven tools tailored specifically for women’s oncology.

Technological innovation is a major driver fueling growth in the Women’s Oncology Detection Solutions market. Breakthroughs in molecular diagnostics, genomics, and imaging techniques have greatly enhanced the accuracy, speed, and ease of cancer detection. For instance, liquid biopsy and genomic profiling allow non-invasive, early detection of tumors and personalized treatment plans based on genetic markers. @@@@ Artificial intelligence and machine learning algorithms are improving image analysis and diagnostic precision, reducing human error, and enabling earlier intervention. For instance, in October 2024, Health Executive Center and Siemens Healthineers Vietnam officially announced the implementation of a 3D mammography system integrated with Artificial Intelligence to improve the accuracy of breast cancer detection. This deployment highlighted growing adoption of cutting-edge technologies in emerging markets, driving demand for AI-integrated imaging solutions. It also improved access to high-quality breast cancer screening in the region, supporting earlier interventions and better patient outcomes.

Thus, such initiatives are expected to contribute to expand the market reach and accelerating technological innovation within women’s oncology diagnostics globally.

Market Restraints:

High Cost of Advanced Diagnostic Technologies

A significant restraint for the Women’s Oncology Detection Solutions market is the high cost associated with advanced diagnostic technologies. Cutting-edge tools like molecular profiling, AI-powered imaging, and liquid biopsy tests often require expensive equipment and specialized expertise, making them less accessible in low- and middle-income regions. This cost barrier limits widespread adoption, especially in developing countries where healthcare budgets are constrained and infrastructure is inadequate. Additionally, the expense can deter patients from undergoing regular screenings, slowing early diagnosis efforts. Thus, these financial and logistical hurdles restrict the overall growth potential of the market, particularly in areas where early cancer detection is most needed.

The Women’s Oncology Detection Solutions market has a profound socio-economic impact by improving early cancer detection, which leads to better treatment outcomes and reduced healthcare costs over time. Early diagnosis helps decrease the burden of advanced cancer treatments, lowering financial strain on patients and healthcare systems. Improved detection technologies also promote health equity by enabling access to screening in underserved communities, especially as portable and AI-driven tools become more widespread. Furthermore, healthier women contribute more actively to the workforce and society, supporting economic growth. However, disparities in access due to cost and infrastructure challenges remain, highlighting the need for inclusive policies to ensure that the benefits of these innovations reach all socio-economic groups globally.

Segmental Analysis:

The breast cancer segment is poised for significant growth due to the rising global incidence of breast cancer among women. Increasing awareness about the importance of early detection, combined with advancements in screening technologies, is driving demand for effective diagnostic solutions. Innovations such as 3D mammography, molecular testing, and AI-assisted imaging are improving the accuracy and speed of breast cancer detection, encouraging more women to undergo regular screenings. Additionally, government initiatives and healthcare campaigns focused on breast cancer prevention are expanding access to diagnostic services. With breast cancer being the most common cancer in women worldwide, this segment’s growth is expected to outpace others, making it a key focus for companies developing women’s oncology detection solutions.

Mammography remains the most widely used and trusted technique for breast cancer screening, which is why this segment is expected to see strong growth. Advances like digital mammography and 3D tomosynthesis have improved image clarity, helping detect tumors earlier and more accurately. Increased awareness campaigns and government screening programs worldwide are encouraging women to regularly undergo mammograms, boosting demand. The accessibility of mammography services in both urban and rural healthcare facilities is also expanding.

Additionally, the integration of AI technology to assist radiologists in interpreting mammograms is enhancing diagnostic confidence and efficiency. For instance, in April 2025, Hologic, Inc. showcased its leadership at the Society of Breast Imaging (SBI) Annual Symposium held in Colorado Springs, Colorado. The company highlighted groundbreaking new research from a leading healthcare institution, demonstrating the effectiveness of its AI-driven mammography technology. Hologic’s AI-driven mammography technology enhances diagnostic accuracy and efficiency, making mammography screenings more reliable and accessible. This innovation drives growth in the mammography segment by encouraging wider adoption of advanced imaging solutions in breast cancer detection. Thus, these factors combine to make mammography a fast-growing segment in the women’s oncology detection market.

Early detection and screening are critical to improving survival rates in women’s cancers, which is why this segment is expected to experience rapid growth. Innovations in non-invasive and minimally invasive diagnostic technologies make it easier for women to get screened regularly and detect cancer at an early, more treatable stage. Governments and healthcare organizations are increasingly prioritizing screening programs, especially in high-risk populations, to reduce cancer mortality. Growing awareness among women about the benefits of early diagnosis is also driving demand for these services. Furthermore, advancements in AI and molecular diagnostics are making screening more accurate and personalized, helping to identify cancer earlier than traditional methods and ultimately saving more lives.

Hospitals are expected to see substantial growth as key end-users in the women’s oncology detection solutions market. As primary centers for cancer diagnosis and treatment, hospitals are investing in state-of-the-art diagnostic equipment, including advanced imaging and molecular testing tools. The increasing number of cancer patients seeking timely and comprehensive care at hospitals is driving demand for better detection technologies. Moreover, hospitals are adopting AI-powered systems to enhance diagnostic accuracy and patient outcomes. Many hospitals are also expanding their cancer screening programs to reach larger populations, improving early detection rates. These investments and the growing patient base make hospitals a crucial segment contributing to the market’s overall expansion.

North America is expected to lead growth in the women’s oncology detection solutions market due to its advanced healthcare infrastructure and high awareness of women’s health issues. The region benefits from strong government support, extensive research funding, and widespread adoption of innovative diagnostic technologies.

The presence of leading market players and numerous clinical trials further accelerates the development and availability of cutting-edge solutions. For instance, in June 2025, Clairity, Inc., a digital health innovator advancing AI-driven healthcare solutions, received U.S. Food and Drug Administration (FDA) De Novo authorization for CLAIRITY BREAST, a novel image-based prognostic platform designed to predict five-year breast cancer risk from a routine screening mammogram. The FDA authorization of Clairity’s CLAIRITY BREAST platform significantly impacted the global Women’s Oncology Detection Solutions market by introducing a cutting-edge AI-driven tool for more accurate breast cancer risk prediction. This innovation enhances early detection capabilities, allowing healthcare providers to identify high-risk patients more effectively through routine mammograms.

Similarly, in April 2025, RadNet, Inc. entered into a definitive merger agreement under with iCAD. The merger between RadNet and iCAD had a significant impact on the Women’s Oncology Detection Solutions market by combining RadNet’s extensive diagnostic imaging network with iCAD’s advanced AI-powered breast health technologies. The merger strengthened the ability to offer more accurate, efficient, and cost-effective screening services, accelerating the adoption of AI-driven solutions in women’s oncology diagnostics. @@@@ Additionally, proactive screening programs and a growing aging population contribute to increased demand for early cancer detection services. Technological advancements, including AI integration and liquid biopsy adoption, are more rapidly implemented in North America, reinforcing its position as the largest and fastest-growing regional market in women’s oncology detection.

To Learn More About This Report - Request a Free Sample Copy

The global Women’s Oncology Detection Solutions market is characterized by a dynamic and competitive landscape, with both established healthcare giants and innovative startups driving advancements. Leading companies like Hologic Inc., Siemens Healthineers, GE Healthcare, Abbott Laboratories, and Roche Diagnostics dominate the market through a combination of robust product portfolios, strategic acquisitions, and substantial investments in research and development. These firms are focusing on enhancing diagnostic accuracy and accessibility by integrating artificial intelligence, liquid biopsy technologies, and portable diagnostic devices into their offerings. Additionally, companies such as Redcliffe Labs are introducing digital-first platforms like Femcliffe, catering to the growing demand for personalized and convenient women's health diagnostics . This blend of technological innovation and strategic collaboration is reshaping the market, fostering a competitive environment that prioritizes early detection, personalized care, and broader accessibility.

The major players for above market are:

Recent Developments:

Q1. What are the main growth driving factors for this market?

The market is growing mainly because more people are aware of women’s health issues, especially cancers like breast and ovarian cancer. Advances in technology, such as molecular diagnostics and imaging, are making detection easier and more accurate. Government support and the use of AI in diagnostics are also helping the market expand.

Q2. What are the main restraining factors for this market?

The high costs of advanced diagnostic tools, limited access in rural or low-resource areas, and a shortage of trained healthcare professionals slow down the market’s growth. Additionally, strict regulations and inadequate healthcare infrastructure in some regions make it harder for these solutions to be widely adopted.

Q3. Which segment is expected to witness high growth?

The breast cancer diagnostics segment is expected to see the most growth due to rising breast cancer cases and innovations in imaging, genetic testing, and AI technology. Prenatal diagnostics is also growing quickly as more women seek early detection and monitoring options.

Q4. Who are the top major players for this market?

Key players include Abbott Laboratories, Siemens Healthineers, GE Healthcare, Hologic, Roche, Becton Dickinson, Quest Diagnostics, PerkinElmer, bioMérieux, and Philips. These companies are investing heavily in new technologies and partnerships to strengthen their market position.

Q5. Which country is the largest player?

The United States leads the global market because of its advanced healthcare system, high awareness levels, and presence of major companies. Strong government support and significant research investments also contribute to the U.S.’s dominant role.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model