Get Complete Analysis Of The Report - Download Updated Free Sample PDF

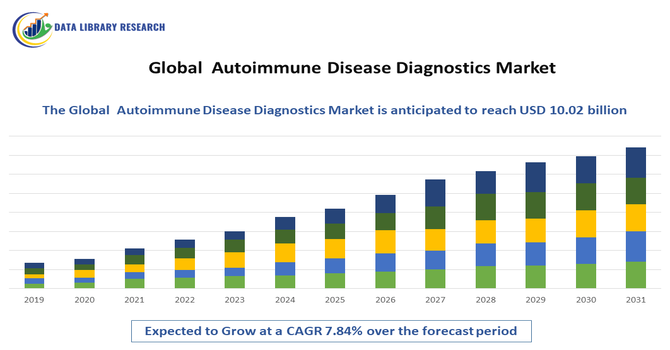

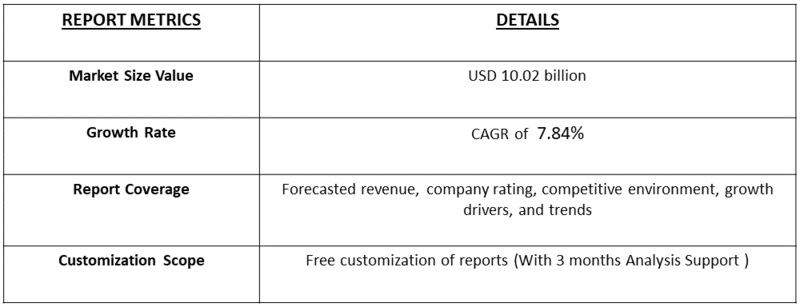

The Global Autoimmune Disease Diagnostics Market refers to the industry involved in the development, production, and commercialization of diagnostic tests used to detect and monitor autoimmune disorders such as rheumatoid arthritis, systemic lupus erythematosus, multiple sclerosis, and type 1 diabetes. These diagnostics primarily include immunoassays, autoantibody tests, antinuclear antibody (ANA) tests, ELISA-based assays, molecular diagnostics, and multiplex platforms performed in clinical laboratories, hospitals, and research institutions. Market growth is driven by rising autoimmune disease prevalence, technological advances in immunodiagnostics, and increased demand for early disease detection. Expanding healthcare infrastructure and improved awareness of autoimmune conditions further support the adoption of advanced diagnostic solutions globally.

The autoimmune disease diagnostics market is witnessing several technological and operational trends shaping its growth. A major trend is the integration of automation and high-throughput immunoassay platforms that enhance diagnostic accuracy and reduce turnaround time in laboratories. Multiplex assays capable of detecting multiple biomarkers simultaneously are also gaining adoption. Artificial intelligence–based analysis tools for immunofluorescence imaging are emerging to improve diagnostic interpretation. Additionally, healthcare systems are expanding screening programs and laboratory infrastructure, particularly in Asia-Pacific and emerging economies. Point-of-care testing and biomarker discovery initiatives are further accelerating innovation in autoimmune diagnostics, enabling earlier disease detection and personalized treatment planning for patients worldwide.

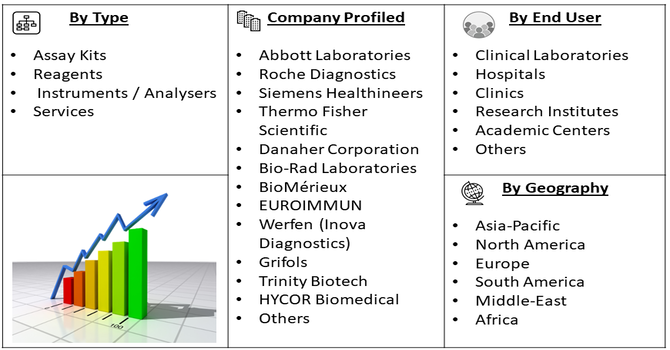

Segmentation: The Global Autoimmune Disease Diagnostics Market is segmented by Product Type (Assay Kits & Reagents, Instruments / Analysers and Services), Test Type (Antinuclear Antibody (ANA) Tests, Autoantibody Tests, Inflammatory Marker Tests, Routine Laboratory Tests, Immunologic Tests and Other Test Types), Disease Type (Systemic Autoimmune Diseases (Rheumatoid Arthritis, Systemic Lupus Erythematosus (SLE), Multiple Sclerosis, Scleroderma and Others) and Organ-Specific (Localized) Autoimmune Diseases (Type 1 Diabetes, Hashimoto’s Thyroiditis, Graves’ Disease, Inflammatory Bowel Disease and Others)), End User (Clinical Laboratories, Hospitals & Clinics, Research Institutes & Academic Centers and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing global prevalence of autoimmune diseases is a major driver for the autoimmune disease diagnostics market. Disorders such as rheumatoid arthritis (RA), systemic lupus erythematosus (SLS), and autoimmune thyroid diseases are being diagnosed more frequently due to environmental factors, genetic predisposition, lifestyle changes, and improved clinical awareness. For instance, in 2025, an article published by NCBI reported that in 2021, there were 17.92 million cases of RA globally, with the ASIR increasing from 10.42 to 11.8 cases per 100,000 individuals. Similar, an article titled, Global type 1 diabetes prevalence, incidence, and mortality estimate 2025: Results from the International diabetes Federation Atlas, 11th Edition, and the T1D Index Version 3.0, reported that there were an estimated 9.50 million people living with type 1 diabetes in 2025, compared to 8.4 million in 2021, a 13% increase.

The growing patient pool has significantly increased the demand for reliable diagnostic testing and disease monitoring tools. Healthcare providers are prioritizing early detection to reduce complications and improve treatment outcomes. As autoimmune conditions often require lifelong management, repeated diagnostic testing further increases market demand for immunoassays, biomarker panels, and laboratory-based screening solutions worldwide.

Technological innovations in diagnostic platforms are strongly driving growth in the autoimmune disease diagnostics market. Advances in immunoassays, multiplex testing systems, and molecular diagnostics have significantly improved sensitivity, specificity, and speed of autoimmune disease detection. For instance, in 2025, Revvity, Inc. announced expansion of its type 1 diabetes diagnostic portfolio with development of a population-scale 4-plex in vitro diagnostic assay supported by Sanofi. The initiative strengthened early detection capabilities for Type 1 Diabetes and supported innovation in large-scale autoimmune disease screening, positively influencing growth of the global autoimmune disease diagnostics market.

Automated laboratory analyzers allow high-throughput testing, enabling clinical laboratories to process large volumes of patient samples efficiently. Emerging technologies such as AI-based imaging analysis, antigen microarrays, and biomarker profiling are further enhancing disease detection capabilities. These innovations support earlier diagnosis and more precise disease classification, which is essential for personalized treatment strategies and improved patient outcomes. Continuous R&D investments by diagnostic companies are accelerating these technological improvements globally.

Market Restraints:

The major restraint affecting the autoimmune disease diagnostics market is the lack of standardized testing procedures and variability in diagnostic assays. Different laboratories often use varied immunoassay kits, biomarkers, and testing protocols, which can result in inconsistent diagnostic outcomes. Autoimmune diseases also present complex and overlapping symptoms, making clinical interpretation challenging and sometimes leading to delayed or inaccurate diagnoses. Additionally, certain specialized tests require advanced laboratory infrastructure and trained professionals, limiting accessibility in developing healthcare systems. These challenges may slow market adoption and hinder widespread implementation of advanced autoimmune diagnostic solutions despite growing demand for early detection and disease monitoring.

The socioeconomic impact of autoimmune disease diagnostics is significant due to the growing burden of chronic autoimmune conditions worldwide. Early and accurate diagnosis reduces long-term healthcare costs by enabling timely treatment and preventing complications. Improved diagnostic access also enhances patient quality of life and workforce productivity by minimizing disability associated with diseases such as lupus or rheumatoid arthritis. Governments and health organizations increasingly invest in diagnostic research and screening programs to manage rising healthcare expenditures linked to chronic immune disorders. Additionally, the expansion of diagnostic laboratories and manufacturing facilities creates employment opportunities and stimulates economic growth in the global in-vitro diagnostics industry.

Segmental Analysis:

The Assay Kits & Reagents segment is expected to witness the highest growth in the global autoimmune disease diagnostics market over the forecast period due to their essential role in routine diagnostic testing. These kits are widely used in immunoassays, ELISA tests, and multiplex platforms to detect specific autoantibodies associated with autoimmune disorders. Growing demand for early disease detection and continuous monitoring is increasing the consumption of assay reagents in clinical laboratories and hospitals. Additionally, technological advancements in reagent formulation and biomarker identification are improving test sensitivity and specificity. The recurring demand for consumables in diagnostic procedures, along with increasing laboratory testing volumes, is expected to drive strong growth for this segment globally.

The Antinuclear Antibody (ANA) Tests segment is anticipated to experience the highest growth during the forecast period due to its critical role as a primary screening tool for several autoimmune diseases. ANA testing is commonly used for diagnosing conditions such as systemic lupus erythematosus, rheumatoid arthritis, and scleroderma. Increasing awareness among healthcare professionals regarding early autoimmune disease detection is driving the adoption of ANA testing in hospitals and diagnostic laboratories. Moreover, improvements in automated immunofluorescence and multiplex assay technologies are enhancing test accuracy and efficiency. As autoimmune disease prevalence continues to rise worldwide, the demand for reliable and widely accepted screening tests like ANA is expected to increase significantly.

The Type 1 Diabetes segment is expected to witness the highest growth in the autoimmune disease diagnostics market over the forecast period due to the rising incidence of the disease, particularly among children and young adults. Increasing awareness about early detection and disease management is encouraging healthcare providers to adopt advanced diagnostic tests that identify autoimmune markers associated with pancreatic beta-cell destruction. The growing use of autoantibody tests, genetic screening, and biomarker-based diagnostic tools is improving the accuracy and speed of Type 1 diabetes diagnosis. Additionally, expanding healthcare infrastructure and screening programs across developing countries are supporting the increasing demand for early diagnostic testing in this segment.

The Hospitals & Clinics segment is projected to witness the highest growth in the autoimmune disease diagnostics market during the forecast period due to the increasing number of patient visits and diagnostic procedures conducted in these healthcare facilities. Hospitals and clinics are primary points of care where patients seek medical evaluation for autoimmune symptoms, leading to higher demand for diagnostic testing. The integration of advanced laboratory equipment and automated diagnostic platforms in hospital laboratories is improving testing capacity and efficiency. Furthermore, the expansion of healthcare infrastructure and the increasing availability of specialized diagnostic services in hospitals and clinics are expected to support significant growth in this segment.

North America is expected to witness the highest growth in the global autoimmune disease diagnostics market over the forecast period due to its advanced healthcare infrastructure and strong adoption of innovative diagnostic technologies.

The region has a high prevalence of autoimmune disorders, which increases demand for early detection and continuous disease monitoring. For instance, in 2025, The Lupus Foundation of America estimated that 1.5 million Americans, have a form of lupus. Similarly, in January 2026, Thyroid Foundation of Canada, reported that hypothyroidism affected approximately 5 individuals in 100.

Significant investments in research and development, along with the presence of major diagnostic companies and well-established laboratory networks, further support market expansion. For instance, in April 2025, Amgen announced that the U.S. Food and Drug Administration approved UPLIZNA for treating Immunoglobulin G4-related disease. The approval highlighted increasing recognition of rare autoimmune conditions, which encouraged earlier detection and monitoring. This development supported demand for advanced diagnostic testing and strengthened growth of the North American autoimmune disease diagnostics market.

Additionally, favourable reimbursement policies and increasing awareness about autoimmune diseases among healthcare professionals and patients contribute to the rising utilization of diagnostic tests across the region. For instance, in the United States, Autoimmune Disease Awareness Month, March highlighted the growing burden of autoimmune conditions affecting millions of people. Such initiatives led by the Autoimmune Association increased public and clinical awareness, encouraged early diagnosis, and promoted research efforts, which supported greater demand for autoimmune disease diagnostic testing across North America.

To Learn More About This Report - Request a Free Sample Copy

The global autoimmune disease diagnostics market is moderately consolidated, with a mix of multinational diagnostic corporations and specialized immunodiagnostic companies competing for market share. Leading firms maintain dominance through extensive immunoassay portfolios, automated diagnostic systems, and strong global distribution networks. Major companies leverage integrated diagnostic platforms and reagent-based revenue models, while smaller specialized firms focus on niche biomarker tests and innovative assay technologies. Strategic collaborations, acquisitions, and investments in research and development are common competitive strategies. Companies also differentiate themselves through advanced biomarker panels, regulatory approvals, and expanded laboratory testing services to strengthen their positions in the evolving autoimmune diagnostics industry.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is primarily driven by the rising global incidence of autoimmune disorders, such as rheumatoid arthritis and type 1 diabetes. Growth is further propelled by advancements in laboratory automation and multiplex testing, which allow for faster, more accurate results. Increased awareness and government funding for early diagnosis also boost adoption.

Q2. What are the main restraining factors for this market?

Growth is significantly hindered by the high cost of advanced diagnostic kits and specialized instrumentation. A global shortage of skilled laboratory professionals and clinicians trained in interpreting complex results remains a hurdle. Additionally, inconsistent regulatory standards and limited healthcare infrastructure in developing regions can delay the availability of new tests.

Q3. Which segment is expected to witness high growth?

The Antinuclear Antibody (ANA) Tests segment is expected to witness the highest growth over the forecast period due to its widespread use as a primary screening tool for autoimmune diseases. Increasing prevalence of conditions such as lupus and rheumatoid arthritis, along with advancements in automated immunofluorescence and multiplex testing technologies, is driving demand for ANA testing globally.

Q4. Who are the top major players for this market?

The market is led by global diagnostics giants, including Thermo Fisher Scientific, F. Hoffmann-La Roche, Abbott Laboratories, and Siemens Healthineers. Other key players driving innovation through specialized assays and analyzers include Bio-Rad Laboratories, Quest Diagnostics, Werfen (Inova Diagnostics), Euroimmun, and Beckman Coulter.

Q5. Which country is the largest player?

The United States is the largest market player, holding a dominant share of global revenue. This position is supported by a sophisticated healthcare ecosystem, high R&D investment, and favorable reimbursement policies that encourage the early adoption of advanced, high-cost diagnostic technologies.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model