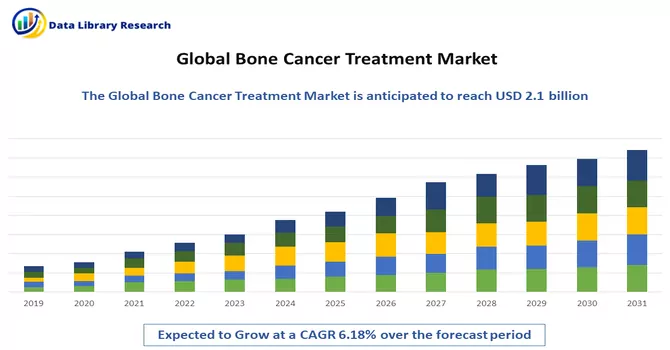

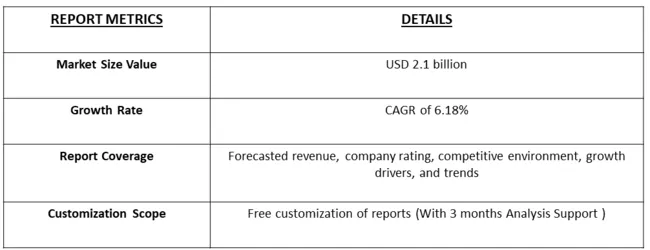

The bone cancer treatment market size is estimated at USD 2.1 billion in 2023 and is expected to register a CAGR of 6.18% during the forecast period (2024-2031).

Get Complete Analysis Of The Report - Download Free Sample PDF

Bone cancer refers to a rare type of cancer that originates in the bones, typically affecting the long bones of the arms and legs or the pelvis. It can occur at any age but is more common in children and young adults. Bone cancer can be primary, originating in the bones themselves, or secondary, spreading to the bones from other parts of the body. Symptoms may include bone pain, swelling, and fractures, and the condition is diagnosed through imaging tests and biopsy. Treatment options include surgery, chemotherapy, radiation therapy, and targeted therapy, depending on the type and stage of the cancer. Early detection and treatment are critical for improving outcomes in bone cancer patients.

The market overview of bone cancer treatment reflects a complex landscape shaped by a combination of conventional and innovative therapeutic approaches. Bone cancer, encompassing primary and metastatic forms, necessitates a multifaceted treatment strategy tailored to the specific type, stage, and individual patient characteristics. Conventional treatments, such as surgery, chemotherapy, and radiation therapy, remain foundational in addressing bone cancer. However, advancements in targeted therapies, immunotherapies, and precision medicine have significantly influenced the market, offering more tailored and effective options. The integration of novel agents, including receptor activators of nuclear factor-kappa B (RANK) ligand inhibitors and tyrosine kinase inhibitors, showcases the ongoing paradigm shift towards targeted and personalized interventions.

Moreover, the exploration of immunotherapeutic modalities and the development of bone-seeking radiopharmaceuticals contribute to the diversification of treatment options. As the bone cancer treatment market continues to evolve, the emphasis on a comprehensive and patient-centric approach, along with ongoing research and development efforts, drives innovation and progress in addressing the complexities of bone cancer management.

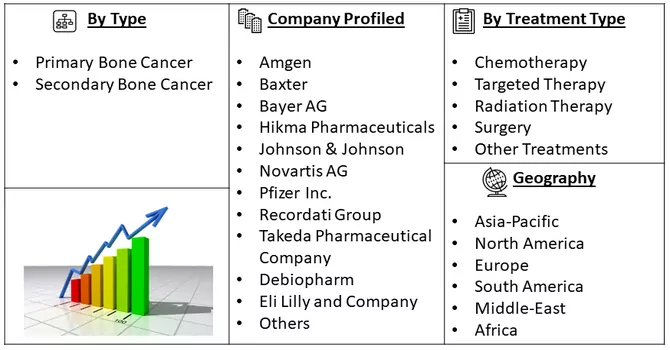

Market segmentation: Bone Metastasis Treatment Companies and it is segmented by Bone Cancer Type (Primary Bone Cancer [Osteosarcoma, Chondrosarcoma, Ewing Tumor, and Other Bone Cancer Types] and Secondary Bone Cancer [Metastatic Bone Cancer]), Treatment Type (Chemotherapy, Targeted Therapy, Radiation Therapy, Surgery, and Other Treatments), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market size and forecasts in value (USD million) for the above segments.

For Detailed Market Segmentation - Download Free Sample PDF

The market trends in bone cancer treatment underscore a dynamic landscape characterized by a growing focus on precision medicine, targeted therapies, and immunotherapeutic approaches. With advancements in understanding the molecular and genetic basis of bone cancers, there is a notable shift towards more personalized treatment strategies, aiming to tailor interventions based on individual patient profiles. The emergence of novel targeted agents, such as receptor activator of nuclear factor-kappa B (RANK) ligand inhibitors, showcases a trend towards specific and effective therapies. Additionally, the integration of immunotherapies, including checkpoint inhibitors and adoptive cell therapies, is gaining traction, offering promising avenues for bolstering the body's immune response against cancer cells. The market also witnesses ongoing developments in bone-seeking radiopharmaceuticals, contributing to improved diagnostics and therapeutics. Collaborations between pharmaceutical companies and research institutions further drive innovation in bone cancer treatment, reflecting a commitment to addressing the complexities of this challenging disease through diverse and cutting-edge therapeutic modalities.

Market Drivers:

The continuous evolution of diagnostic imaging technologies

The continuous evolution of diagnostic imaging technologies represents a pivotal driver in the medical field, revolutionizing healthcare by enhancing precision and early detection across various conditions, including bone-related malignancies. Advancements in techniques such as positron emission tomography (PET) scans, magnetic resonance imaging (MRI), and cutting-edge X-ray modalities have significantly improved the accuracy and depth of diagnostic capabilities. In the context of bone cancer treatment, these sophisticated imaging tools play a crucial role in early detection, precise localization, and comprehensive assessment of the extent of malignancies. The ongoing refinement and integration of these diagnostic technologies not only contribute to the optimization of treatment strategies but also underscore the importance of early intervention, ultimately improving patient outcomes and steering the trajectory of the entire bone cancer treatment market.

The rising incidence of bone-related malignancies

The escalating incidence of bone-related malignancies emerges as a compelling driver in the realm of oncology, significantly influencing the landscape of bone cancer treatment. Factors such as an ageing population, lifestyle changes, and improved diagnostic capabilities contribute to the increased detection of primary bone cancers and metastatic bone diseases. This surge in cases underscores the pressing need for advanced therapeutic interventions, propelling research, and development efforts in the bone cancer treatment market. As the prevalence of bone-related malignancies continues to rise, healthcare systems are faced with a growing patient population necessitating targeted and effective treatment modalities. This trend not only accentuates the urgency of addressing bone cancers but also fuels innovation, investment, and collaborative efforts within the medical community to meet the evolving challenges posed by the increasing occurrence of these malignancies.

Market Restraints:

Several market restraints pose challenges to the bone cancer treatment market, with one major factor being the complexity of developing effective therapies for diverse types of bone cancers. The heterogeneity of bone tumors necessitates specialized approaches, often hindering the development of universally applicable treatments. Additionally, the high cost associated with the research, development, and clinical trials of innovative bone cancer therapies poses financial challenges for both pharmaceutical companies and healthcare systems. Regulatory hurdles and stringent approval processes further contribute to delays in bringing novel treatments to market. Moreover, the limited awareness about bone cancers and the lack of standardized diagnostic criteria may lead to delayed or misdiagnosed cases, impacting the timely initiation of appropriate treatment. The potential side effects of aggressive treatments, such as surgery and certain targeted therapies, also influence treatment decisions and patient acceptance. These multifaceted restraints collectively shape the intricate landscape of the bone cancer treatment market, highlighting the need for comprehensive strategies to overcome these challenges and advance effective therapeutic interventions.

The COVID-19 pandemic has exerted a multifaceted impact on the bone cancer treatment market. Disruptions in healthcare systems, resource reallocation towards pandemic management, and pandemic-induced restrictions have led to delays in elective surgeries and treatment plans for many bone cancer patients. The redirection of clinical resources and prioritization of COVID-19-related care have affected the timely diagnosis and initiation of bone cancer treatment. Additionally, logistical challenges in the supply chain for pharmaceuticals and medical devices, coupled with disruptions in clinical trials, have further impeded the development and accessibility of new treatments. Patient hesitancy to seek healthcare services during the pandemic has also contributed to delayed diagnoses and treatments. While telemedicine has offered some alternative avenues for consultations, the overall impact of the pandemic on bone cancer treatment underscores the need for resilient and adaptable healthcare systems to address ongoing challenges and prioritize the well-being of cancer patients in the face of global health crises.

Segmental Analysis:

Ewing Tumor Segment is Expected to Witness Significant Growth Over the Forecast Period

Ewing sarcoma is a type of bone cancer that primarily affects children and young adults. It is a rare cancer that usually arises in the bones but can also develop in soft tissues. Treatment for Ewing sarcoma typically involves a combination of therapies, including surgery, chemotherapy, and radiation therapy. The goal of treatment is to remove the cancerous cells, prevent recurrence, and preserve the affected limb's function. In some cases, targeted therapy or immunotherapy may be used to target specific genetic mutations or enhance the immune system's ability to fight cancer. The treatment approach for Ewing sarcoma is often multidisciplinary, involving a team of specialists, including oncologists, surgeons, and radiation oncologists, to tailor treatment to each patient's specific needs and ensure the best possible outcome.

Targeted Therapy Segment is Expected to Witness Significant Growth Over the Forecast Period

Targeted therapy is a type of treatment for bone cancer that focuses on specific molecules or pathways involved in cancer growth and progression. Unlike traditional chemotherapy, which affects all rapidly dividing cells (both cancerous and healthy), targeted therapy aims to selectively target cancer cells while minimizing damage to normal cells. One example of targeted therapy in bone cancer is the use of drugs that target the receptor activator of nuclear factor-kappa B ligand (RANKL), a protein involved in bone remodelling. By inhibiting RANKL, these drugs can help slow down bone destruction caused by certain types of bone cancer, such as giant cell tumors of the bone. Targeted therapy is often used in combination with other treatments, such as surgery or chemotherapy, to improve outcomes for patients with bone cancer. However, like all cancer treatments, targeted therapy can have side effects, and its effectiveness may vary depending on the specific type and stage of bone cancer.

North America Region is Expected to Witness Significant Growth Over the Forecast Period

The North America bone cancer treatment market is characterized by advanced healthcare infrastructure, high healthcare spending, and a significant focus on research and development. The region's robust regulatory framework and strong reimbursement policies support the development and adoption of innovative treatment options for bone cancer. North America is also home to a large number of pharmaceutical and biotechnology companies actively engaged in developing novel therapies for bone cancer, including targeted therapies, immunotherapies, and personalized medicine approaches. Additionally, the region's increasing prevalence of bone cancer, particularly among the ageing population, is driving the market growth. However, challenges such as high treatment costs and the need for improved early detection methods remain. Overall, the North America bone cancer treatment market is poised for significant growth, driven by a combination of factors including technological advancements, increasing healthcare expenditure, and a growing focus on personalized medicine.

Get Complete Analysis Of The Report - Download Free Sample PDF

The analyzed market exhibits a high degree of fragmentation, primarily attributable to the presence of numerous players operating on both a global and regional scale. The competitive landscape is characterized by a diverse array of companies, each contributing to the overall market dynamics. This fragmentation arises from the existence of specialized solution providers, established industry players, and emerging entrants, all vying for market share. The diversity in market participants is underscored by the adoption of various strategies aimed at expanding the company presence. On a global scale, companies within the studied market are strategically positioning themselves through aggressive expansion initiatives. This often involves entering new geographical regions, targeting untapped markets, and establishing a robust global footprint. The pursuit of global expansion is driven by the recognition of diverse market opportunities and the desire to capitalize on emerging trends and demands across different regions. Simultaneously, at the regional level, companies are tailoring their approaches to align with local market dynamics. Regional players are leveraging their understanding of specific market nuances, regulatory environments, and consumer preferences to gain a competitive edge. This regional focus allows companies to cater to the unique needs of local clientele, fostering stronger market penetration. To navigate the complexities of the fragmented market, companies are implementing a range of strategies. These strategies include investments in research and development to stay at the forefront of technological advancements, mergers and acquisitions to consolidate market share, strategic partnerships for synergies, and innovation to differentiate products and services. The adoption of such multifaceted strategies reflects the competitive nature of the market, with participants continually seeking avenues for growth and sustainability. In essence, the high fragmentation in the studied market not only signifies the diversity of players but also underscores the dynamism and competitiveness that drive ongoing strategic maneuvers. As companies explore various avenues for expansion, the market continues to evolve, presenting both challenges and opportunities for industry stakeholders.

Some of the key market players are:

Recent Development:

1) In December 2021, the Breakthrough Devices designation was conferred upon ZetaMet technology by the FDA's Centers for Devices and Radiological Health, specifically acknowledging its revolutionary potential in the treatment of metastatic bone cancers and osteologic interventions. This regulatory recognition underscores the significance of ZetaMet technology as an innovative and promising advancement in addressing the challenges associated with metastatic bone cancers.

2) In October 2020, Johnson & Johnson finalized the acquisition of Momenta Pharmaceuticals Inc., a strategic move aimed at expanding their portfolio and bolstering their capabilities in various medical domains, including infectious diseases, vaccines, neuroscience, oncology, and pulmonary hypertension. This acquisition positions Johnson & Johnson to contribute significantly to the advancement of therapeutic solutions across diverse medical fields, further solidifying its commitment to addressing complex health issues and improving patient outcomes.

Q1. What was the Bone Cancer Treatment Market size in 2023?

As per Data Library Research the bone cancer treatment market size is estimated at USD 2.1 billion in 2023.

Q2. What is the Growth Rate of the Bone Cancer Treatment Market ?

Bone Cancer Treatment Market is expected to register a CAGR of 6.18% during the forecast period.

Q3. What segments are covered in the Bone Cancer Treatment Market Report?

By Bone Cancer Type, By Treatment Type and Geography these segments are covered in the Bone Cancer Treatment Market Report.

Q4. Who are the key players in Bone Cancer Treatment Market?

Some key players operating in the market include

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model