Get Complete Analysis Of The Report - Download Updated Free Sample PDF

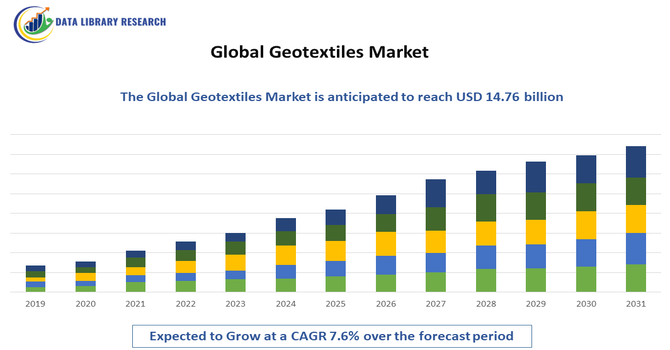

The Global Geotextiles Market comprises the production, distribution, and application of permeable textile materials used in civil engineering and environmental projects to separate, filter, reinforce, drain, and protect soils and aggregates. These fabrics—typically woven or non-woven and made from polymers such as polypropylene, polyester, and high-strength fibers—are essential in infrastructure projects including road construction, drainage systems, erosion control, landfill liners, and coastal protection. Their use enhances soil stability, extends service life of structures, and reduces maintenance costs, driving broad adoption across construction, transportation, agriculture, and environmental remediation worldwide. Market expansion is propelled by rising infrastructure spending and sustainability demands.

Current trends in the geotextiles market include the increasing integration of sustainable and recycled materials, with more products made from recycled PET and biodegradable fibers to meet environmental standards and circular-economy goals. Smart geotextiles with embedded sensors are emerging for real-time monitoring of soil stress and moisture, especially in advanced infrastructure projects. There is a growing emphasis on green infrastructure, such as vegetated swales and stormwater management systems, boosting demand for eco-friendly geotextiles. Public-private collaborations are expanding, and Asia-Pacific leads adoption due to rapid urbanization and infrastructure development. Demand in coastal protection and erosion control has also accelerated globally.

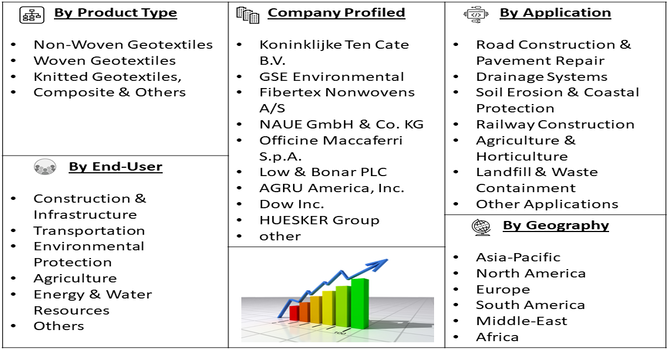

Segmentation: The Global Geotextiles Market is segmented by Product Type (Non-Woven Geotextiles, Woven Geotextiles, Knitted Geotextiles, and Composite & Others), Material (Synthetic Materials (Polypropylene, Polyester, Polyethylene and Others), and Natural Materials (Jute, Coir, and Ramie)), Application (Road Construction & Pavement Repair, Drainage Systems, Soil Erosion & Coastal Protection, Railway Construction, Agriculture & Horticulture, Landfill & Waste Containment and Other Applications), End-Use Industry (Construction & Infrastructure, Transportation, Environmental Protection, Agriculture, Energy & Water Resources and Others), Function (Separation, Filtration, Reinforcement, Drainage and Protection), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The major driver of the geotextiles market is the global surge in infrastructure development, especially in transportation networks such as highways, railways, and urban roadways. Governments and private sectors increasingly use geotextiles for soil stabilization, drainage, filtration, and reinforcement due to their ability to extend pavement life and reduce maintenance costs. For instance, in 2021, Indian Ministry of Rural Development required that at least 15% of PMGSY road projects incorporate green technologies, including coir geotextiles, which significantly increased government adoption of geotextiles for soil stabilization. The policy promoted the use of sustainable materials, encouraged private sector participation, expanded domestic manufacturing capacity, and strengthened overall market demand, thereby positively driving growth in the Global Geotextiles Market.

Projects under initiatives like national highway expansions and cross-border connectivity programs incorporate significant volumes of geotextiles, particularly in Asia-Pacific where infrastructure investment remains robust. Additionally, expanding water management and land reclamation projects further elevate demand, solidifying geotextiles as essential materials in modern civil engineering applications.

Growing emphasis on sustainable construction practices drives geotextile market growth as governments and developers seek materials that reduce environmental impact.

Environmental regulations and green infrastructure initiatives push for products with recycled content or biodegradable alternatives, fuelling innovation and broader adoption. For instance, in February 2026, Peak Nano’s biodegradable polymer films aligned with environmental regulations and green infrastructure goals, driving demand for eco-friendly alternatives. This innovation accelerated adoption of sustainable materials and positively influenced growth and sustainability trends in the Global Geotextiles Market.

Geotextiles used in erosion control, stormwater management, and vegetated soil reinforcement align with climate resilience goals and natural resource conservation. Public funding for eco-centric flood defense and urban greening projects further boosts demand for environmentally friendly geotextiles. This trend not only broadens application scope but also encourages manufacturers to enhance sustainable product portfolios, strengthening market resilience.

Market Restraints:

A key restraint in the geotextiles market is volatility in raw material costs and the environmental impact of conventional synthetic polymers. The production of geotextiles largely depends on petroleum-based materials like polypropylene and polyester, whose prices fluctuate with crude oil markets, raising manufacturing costs and squeezing margins. Additionally, concerns about the non-biodegradability of synthetic geotextiles have triggered regulatory restrictions in ecologically sensitive areas, slowing adoption of traditional products. Disposal of millions of tons of synthetic geotextiles increases landfill burdens, prompting demand for eco-alternatives that can be costlier or less established, thereby limiting overall market growth.

The geotextiles market supports socioeconomic development by enhancing infrastructure resilience and reducing lifecycle costs of public works, which boosts economic productivity and safety. By improving road longevity and drainage effectiveness, geotextiles reduce maintenance budgets for governments and private developers while creating jobs across manufacturing and engineering sectors. Their role in environmental protection, including erosion control and flood mitigation, safeguards communities and agricultural lands from climate-induced damages. Moreover, sustainability initiatives prompt innovation in biodegradable geotextiles, fostering eco-industry growth. In emerging economies, geotextile adoption enables rapid urbanization and rural connectivity, contributing to improved living standards and long-term regional development objectives.

Segmental Analysis:

The knitted geotextiles segment is poised for robust growth as demand rises for flexible, customizable fabrics in specialized civil engineering, landscaping, and environmental protection applications. Knitted geotextiles offer enhanced elasticity and permeability, making them suitable for complex terrains, high-slope erosion control, and unique reinforcement projects where conventional woven or non-woven options fall short. This adaptability is driving adoption in infrastructure and agricultural sectors, particularly where tailored soil stabilization and moisture control are needed. Emerging markets in Asia-Pacific and increasing interest in eco-friendly, lightweight geotextile solutions further boost this segment’s growth prospects over the forecast period.

The polypropylene material segment is projected to witness the highest growth due to its dominant position in the global geotextiles market. Polypropylene geotextiles are hydrophobic, chemically resistant, and cost-effective, making them ideal for a wide range of civil engineering and infrastructure applications such as separation, filtration, and reinforcement. Their durability under varied soil and moisture conditions extends pavement life and reduces maintenance costs, which is critical for long-term infrastructure projects. Growing investments in highway construction and land development globally are expected to sustain strong demand for polypropylene geotextiles through the forecast period.

The road construction and pavement repair application segment is anticipated to exhibit the fastest expansion as infrastructure development accelerates worldwide. Geotextiles play a vital role in improving soil stability, load distribution, and drainage in highway and pavement projects, reducing rutting, settlement, and overall maintenance costs. Government spending on transportation networks, particularly in developing economies, drives this growth. Additionally, stricter quality and performance standards for road longevity are encouraging engineers to integrate geotextile solutions early in design and construction, further bolstering adoption in this segment.

The construction and infrastructure end-use segment is expected to register the highest growth due to rising global investments in urban development, transportation networks, water management, and public works. Geotextiles enhance foundational performance in bridges, embankments, and earthworks by improving soil reinforcement, filtration, and drainage. Rapid urbanization, population growth, and the need for resilient infrastructure in both developed and emerging markets are driving demand across this segment. Additionally, government stimulus packages and sustainability goals aimed at reducing long-term maintenance costs further support geotextile adoption across major infrastructure projects.

The drainage application segment is projected to grow strongly as effective water management becomes increasingly critical in construction and environmental engineering. Geotextiles used in drainage systems help filter water, prevent soil clogging, and maintain permeability, making them essential in stormwater control, landfills, tunnels, and retaining structures. Urban expansion, flood mitigation initiatives, and stricter environmental regulations are driving the implementation of advanced drainage solutions. In regions with variable weather patterns, the demand for durable and reliable drainage geotextiles is rising, reinforcing this segment’s significant growth trajectory.

The North American geotextiles market is expected to witness substantial growth over the forecast period, supported by strong infrastructure spending, regulatory emphasis on environmental protection, and high adoption in major applications such as road construction, erosion control, and drainage. For instance, in 2026, U.S. Road construction projects heavily integrated advanced erosion control measures—such as geotextile filter bags, hydroseeding, and sediment basins—alongside robust drainage solutions, including armored culverts and permeable pavements. These initiatives complied with federal environmental regulations, minimized pollution, managed stormwater runoff, and prevented accelerated erosion during infrastructure development.

The region’s well-established construction industry and ongoing government investment in highway and urban development projects contribute to consistent demand. For instance, in 2025, German supplier Norma sold its water management business to U.S. company Advanced Drainage Systems in a USD 1 billion deal, resulting in Norma losing about a quarter of its projected annual revenue. The acquisition strengthened Advanced Drainage’s market presence, expanded North American geotextile and drainage product supply, and positively impacted the region’s Geotextiles Market by enhancing distribution and infrastructure capabilities.

Additionally, stringent standards for stormwater management and soil stabilization elevate the use of high-performance geotextiles. Technological advances, local manufacturing capabilities, and customization options further enhance market expansion across North America.

To Learn More About This Report - Request a Free Sample Copy

The global geotextiles industry is moderately fragmented, characterized by multinational corporations and specialized regional firms competing across infrastructure, environmental, and agricultural applications. Key players emphasize product innovation, sustainability, and geographic expansion to gain an edge. Many companies diversify portfolios across woven, non-woven, and hybrid geotextiles tailored to soil reinforcement, drainage, and filtration needs. Strategic maneuvers such as capacity expansion, R&D investment, and acquisitions are common to secure larger market shares and enter emerging regions. Europe and North America host well-established firms with strong technical capabilities, while Asia-Pacific’s rapid infrastructure growth attracts both global and domestic competitors, intensifying competition and driving cost efficiencies.

The major players for this market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The surge in global infrastructure projects, particularly in developing nations, acts as a primary catalyst. Geotextiles are increasingly vital for road construction, erosion control, and drainage systems. Additionally, strict environmental regulations regarding soil stabilization and waste management encourage the use of these materials to improve the longevity and sustainability of civil engineering.

Q2. What are the main restraining factors for this market?

Volatile raw material prices, specifically for petroleum-based polymers like polypropylene and polyester, create significant cost fluctuations for manufacturers. Furthermore, a lack of standardized technical knowledge in some regions can lead to improper installation or selection, while the availability of cheaper natural alternatives like coir or jute might deter adoption of high-performance synthetics.

Q3. Which segment is expected to witness high growth?

The Construction & Infrastructure segment is expected to witness the highest growth over the forecast period due to rising global investments in highways, bridges, railways, airports, and urban development projects. Rapid urbanization, population growth, and government infrastructure modernization programs are driving demand for geotextiles to enhance soil stability, drainage efficiency, structural durability, and long-term cost performance.

Q4. Who are the top major players for this market?

The market is dominated by global chemical and textile leaders, including Fibertex Nonwovens, TenCate Geosynthetics (Solmax), and Low & Bonar. Other significant players include Huesker Synthetic GmbH, GSE Environmental, and Officine Maccaferri. These companies maintain their positions through extensive R&D, focusing on high-tensile strength materials and sustainable, recycled polymer production.

Q5. Which country is the largest player?

The U.S. was expected to witness the highest growth in the Global Geotextiles Market over the forecast period due to extensive infrastructure investments, stringent environmental regulations, and increasing adoption of geotextiles in road construction, drainage, and erosion control. Technological advancements and sustainable construction initiatives further drove market expansion.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model