Get Complete Analysis Of The Report - Download Updated Free Sample PDF

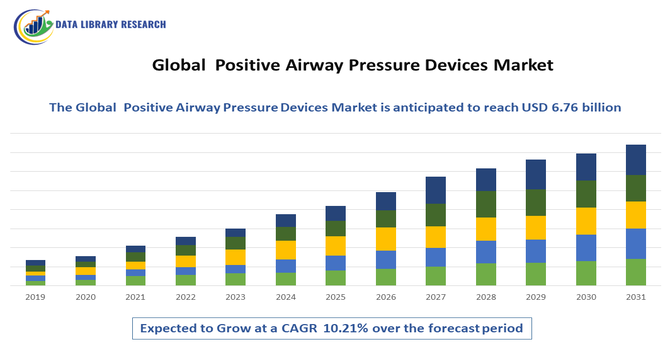

The Global Positive Airway Pressure (PAP) Devices Market comprises medical devices designed to maintain continuous or variable air pressure in a patient’s respiratory tract to treat sleep-related breathing disorders, particularly obstructive sleep apnea (OSA) and other respiratory insufficiencies. PAP devices, including Continuous PAP (CPAP), Automatic PAP (APAP), and Bi-level PAP (BiPAP) systems, deliver pressurized air to keep airways open during sleep, improving oxygenation and patient outcomes. The market’s growth is driven by rising prevalence of sleep apnea, an aging population, enhanced diagnostic rates, technological innovations in device comfort and connectivity, and expanding healthcare infrastructure across regions.

The key market trends include rapid adoption of technologically advanced PAP devices that enhance user comfort, connectivity, and remote monitoring capabilities. Integration of mobile apps, smart pressure adjustment algorithms, quieter motors, and travel-friendly designs are improving patient compliance and expanding home care treatment adoption. There is a noticeable shift toward home-based therapy as patients prefer convenience and cost-effective management outside clinical settings. Moreover, growing awareness of sleep disorders and routine screening programs continue to elevate PAP device demand.

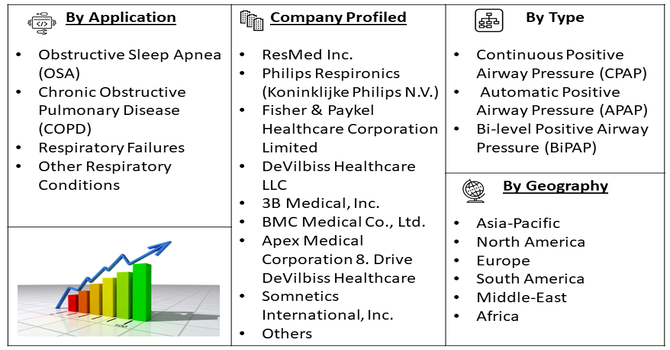

Segmentation: The Global Positive Airway Pressure Devices Market is segmented by Product Type (Continuous Positive Airway Pressure (CPAP), Automatic Positive Airway Pressure (APAP) and Bi-level Positive Airway Pressure (BiPAP)), Application (Obstructive Sleep Apnea (OSA), Chronic Obstructive Pulmonary Disease (COPD) and Respiratory Failures and Other Respiratory Conditions), End-User (Hospitals & Clinics, Home Care Settings & Sleep Labs and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A major driver of the PAP devices market is the increasing prevalence of sleep-related breathing disorders, particularly obstructive sleep apnea (OSA), globally. For instance, the 2025, NCBI published article reported that obstructive Sleep Apnoea (OSA) is a major, underdiagnosed global health crisis affecting an estimated 936 million adults (aged 30–69) with mild-to-severe, and 425 million with moderate-to-severe, conditions. @@@@ Lifestyle changes, rising obesity rates, and aging populations contribute to higher incidence of sleep apnea, prompting greater diagnosis and treatment adoption. Healthcare providers emphasize early intervention to prevent complications like cardiovascular disease and metabolic disorders, driving PAP device demand. Enhanced public awareness, growing sleep health education, and increased sleep study programs have expanded patient pathways into therapy. The consistent need for effective non-invasive respiratory support solutions ensures sustained demand and market growth.

Technological innovations in PAP devices significantly boost market expansion. Manufacturers are integrating features such as connected mobile apps, automatic pressure adjustments, smart sensors, quieter operation, and remote therapy monitoring, enhancing user experience and adherence. For instance, in March 2024, Philips Respiratory Care and Merck KGaA collaborated to integrate CPAP devices with digital health solutions, enhancing remote monitoring, therapy personalization, and home-based care, thereby advancing technological innovation and boosting adoption in the global Positive Airway Pressure Devices market.

These advances address comfort and convenience challenges associated with traditional devices, drawing in new users. Furthermore, the shift toward home-based healthcare solutions accelerates demand as patients and providers favor remote and cost-efficient treatment settings. Telehealth integration and digital health platforms enable clinicians to monitor therapy outcomes outside clinical environments, promoting broader PAP device utilization worldwide.

Market Restraints:

A significant restraint in the global PAP devices market is the high upfront cost of devices and inconsistent insurance reimbursement coverage across regions. Advanced PAP systems can range from several hundred to thousands of dollars, making them financially inaccessible for some patients, particularly in emerging economies. Limited or restrictive insurance coverage often requires extensive documentation, sleep study results, or prior authorization before approval, delaying treatment initiation. Many insurance plans cover only basic device models, leaving patients responsible for upgrades that improve comfort and compliance. This cost barrier restricts market penetration and slows adoption, especially among uninsured or underinsured populations.

The socioeconomic impact of the Positive Airway Pressure Devices Market is significant. PAP therapy improves quality of life for individuals with sleep apnea, reducing morbidity and healthcare costs linked to untreated conditions such as cardiovascular disease, hypertension, and daytime dysfunction. Enhanced sleep quality boosts productivity and reduces accident risks, particularly in working and aging populations. Healthcare systems benefit from decreased long-term treatment costs and hospital admissions related to respiratory complications. However, high device costs and insurance reimbursement challenges can limit access, particularly in lower-income regions, potentially creating disparities in treatment availability and outcomes.

Segmental Analysis:

The APAP segment is expected to experience the highest growth over the forecast period due to its ability to automatically adjust air pressure throughout the night based on patient breathing patterns. This functionality improves comfort and compliance compared with fixed-pressure CPAP devices, reducing therapy abandonment rates. The rising preference for personalized and convenient sleep apnea therapy, coupled with technological advancements like integrated sensors, mobile connectivity, and cloud-based monitoring, drives adoption. APAP devices are increasingly prescribed for both mild and moderate obstructive sleep apnea, making them popular among patients and clinicians. Growing awareness of treatment benefits further supports market expansion globally.

The OSA segment is projected to witness the highest growth due to the increasing prevalence of obstructive sleep apnea worldwide, driven by rising obesity rates, aging populations, and lifestyle factors. OSA is a major contributor to cardiovascular complications, metabolic disorders, and daytime dysfunction, emphasizing early diagnosis and treatment. Healthcare providers are promoting routine sleep studies, which boost PAP device prescriptions. Continuous technological improvements in CPAP, APAP, and BiPAP devices also enhance patient adherence. As awareness of OSA-related health risks rises, both hospitals and home-care providers increasingly recommend PAP therapy, fueling sustained growth in the OSA segment of the global PAP device market.

The home care and sleep lab segment is expected to witness significant growth due to the increasing adoption of home-based PAP therapy. Patients prefer home care for convenience, cost-effectiveness, and privacy, while sleep labs provide specialized diagnostic services supporting treatment initiation. The growth of telehealth and remote monitoring allows clinicians to track therapy adherence and outcomes without requiring in-person visits, further enhancing adoption. This shift reduces hospital dependence and lowers overall treatment costs, especially in regions with advanced home health infrastructure. Expanding awareness campaigns and patient education programs also encourage therapy compliance, making home care and sleep labs a rapidly growing distribution channel.

North America is expected to lead the global PAP devices market due to high awareness of sleep disorders, well-established healthcare infrastructure, and rising prevalence of obstructive sleep apnea. The U.S. is a major market driver, supported by widespread insurance coverage, reimbursement policies, and routine sleep study programs.

Also, the technological innovations such as APAP devices, smart connectivity, and home monitoring solutions further enhance adoption. For instance, In February 2024, ResMed launched its AirCurve 11 bilevel devices with advanced inspiratory and expiratory pressure support and integrated digital technology. This innovation simplified sleep apnea management for healthcare providers, improved patient adherence, and strengthened the adoption of advanced PAP therapies, driving growth and competitiveness in the North American market.

Additionally, aging populations and lifestyle-related factors, including obesity and sedentary habits, increase demand for effective therapy. For instance, the 2025, published report by Health Canada stated that in 2021, 29.5% of Canadian adults had a BMI classified as obesity. An additional 35.5% had a BMI classified as overweight. Therefore, 65% of Canadian adults are classified in the combined overweight and obesity category. Men were more likely than women to have a BMI in the overweight range (39.7% versus 31.3%).

Furthermore, the strong regulatory frameworks and active participation of healthcare providers in patient education and diagnosis contribute to North America maintaining the highest market share over the forecast period. For instance, in July 2024, the FDA’s reclassification of positive airway pressure (PAP) delivery systems from Class III to Class II, while keeping them prescription-only, streamlined regulatory requirements. This facilitated faster product approvals and market entry, boosting innovation and adoption, and significantly accelerating growth in the North American PAP devices market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the PAP devices market is moderately concentrated among global medical device manufacturers and respiratory care specialists who focus on innovation, product differentiation, and geographic expansion. Leading companies invest heavily in research and development to launch advanced PAP solutions with comfort, connectivity, and remote monitoring features. Market players also pursue strategic partnerships, collaborations, and expanded distribution networks to broaden their global reach. Competition is driven by technological advancements, brand reputation, product performance, and service support, with established players holding significant market shares but emerging firms contributing specialized and cost-effective alternatives.

The major factors are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is driven by the rising prevalence of obstructive sleep apnea, increasing obesity and aging population, and growing awareness of sleep disorders. Technological advancements such as smart connectivity, portable devices, and telemonitoring improve adoption. Expanding healthcare infrastructure and better diagnostic access further accelerate demand for positive airway pressure devices globally.

Q2. What are the main restraining factors for this market?

High device costs and limited reimbursement policies restrict affordability, especially in emerging markets. Patient discomfort, mask-related issues, and low adherence reduce long-term usage. Lack of awareness and underdiagnosis of sleep apnea also hinder adoption. Additionally, insurance approval delays and limited access to sleep clinics constrain overall market growth significantly.

Q3. Which segment is expected to witness high growth?

The Automatic Positive Airway Pressure (APAP) segment is expected to witness the highest growth due to its ability to automatically adjust pressure levels based on patient breathing patterns, improving comfort and compliance. Rising preference for personalized therapy, increasing home healthcare adoption, and advancements such as AI-enabled monitoring and connectivity are further accelerating segment demand globally.

Q4. Who are the top major players for this market?

Key market players include ResMed, Koninklijke Philips, Fisher & Paykel Healthcare, Drive DeVilbiss Healthcare, BMC Medical, Löwenstein Medical, and Vyaire Medical. Other notable companies include Medtronic, GE Healthcare, and Apex Medical. These firms focus on innovation, partnerships, and digital integration to strengthen their global presence and competitive positioning.

Q5. Which country is the largest player?

North America, particularly the United States, dominates the global market due to high sleep apnea prevalence, advanced healthcare systems, and strong reimbursement frameworks. However, China is emerging as a major growth leader due to expanding healthcare infrastructure, large patient population, and increasing awareness, making it a key future market.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model