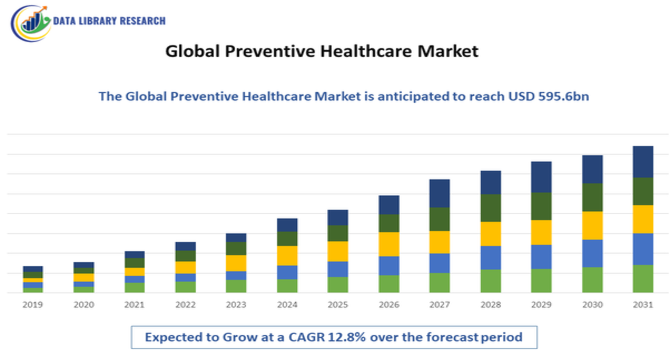

The Global Preventive Healthcare Market size was USD 276.65 billion in 2026, and is expected to reach USD 595.6bn by 2033, at a CAGR of 12.8% from 2026-2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Preventive Healthcare Market refers to services, technologies, and programs aimed at averting illness and promoting long term health rather than treating disease after onset. It includes preventive screenings, vaccinations, chronic disease monitoring, wellness programs, predictive analytics, and digital health tools like wearable devices and telemedicine platforms. By enabling early detection, personalized risk assessment, and continuous health monitoring, preventive healthcare reduces the burden of chronic conditions, improves patient outcomes, and lowers overall healthcare costs. The market spans individual consumers, healthcare providers, insurers, employers, and public health agencies worldwide, driven by rising health awareness and policy support for proactive care models.

Key trends in the Global Preventive Healthcare Market include rapid adoption of digital health technologies, such as AI powered analytics, telemedicine, and wearable monitoring devices that enable continuous real time tracking of health parameters. Personalized healthcare is gaining traction, with precision risk profiling and data driven interventions becoming mainstream. There’s also an increased integration of preventive services into traditional care pathways, emphasizing early detection and disease management. Employers and insurers are expanding wellness initiatives, while remote and hybrid care models enhance accessibility. These trends reflect a shift from reactive treatment toward proactive, data driven, and patient centric care that emphasizes long term wellbeing.

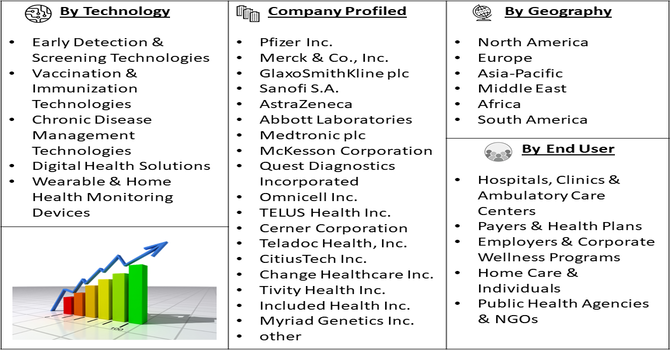

Segmentation: The Global Preventive Healthcare Market is segmented by Technology (Early Detection & Screening Technologies, Vaccination & Immunization Technologies, Chronic Disease Management Technologies, Digital Health Solutions, Wearable & Home Health Monitoring Devices, Advanced Technologies to Reduce Clinical Errors and Personalized/Genomic Medicine & Risk Assessment), End User (Hospitals, Clinics & Ambulatory Care Centers, Payers & Health Plans, Employers & Corporate Wellness Programs, Home Care & Individuals and Public Health Agencies & NGOs), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The strongest drivers for the Global Preventive Healthcare Market is the growing prevalence of chronic diseases like diabetes, cardiovascular conditions, cancer, and obesity. For instance, in July 2023, an article published by The Lancet reported that prevalence of abdominal obesity in the India was found to be 40% in women and 12% in men. The findings show that 5–6 out of 10 women between the ages of 30–49 is abdominally obese.

Similarly, Government of Canada, published the recent data that highlighted with 5,805,000 people (15%) affected by diagnosed and undiagnosed diabetes, projected to reach 7,304,000 (16%). Diagnosed cases stood at 4,007,000 (10%), expected to rise to 5,301,000 (12%). Type 1 accounted for 5–10% of prevalence. Combined diabetes and prediabetes affected 11,918,000 (30%), forecasted to grow to 14,123,000 (32%). Diagnosed cases were projected to increase 32% by 2034, while total diagnosed and undiagnosed cases were expected to rise 26%.

As these conditions rise globally due to aging populations, lifestyle changes, and urbanization, healthcare systems face escalating costs and resource strain. Preventive measures such as regular screening, early risk assessment, and continuous monitoring help identify and manage conditions before they progress, reducing long term treatment expenses and complications. Governments, insurers, and employers increasingly support preventive strategies to mitigate the chronic disease burden, driving investment in screening technologies, digital platforms, wellness programs, and personalized care initiatives worldwide.

Rapid technological advancements in digital health, AI, wearable devices, and remote monitoring are major drivers of market growth. Innovations like AI driven predictive analytics, smartphone connected sensors, telehealth platforms, and big data tools enable precise and timely identification of health risks, fostering more effective preventive actions. For instance, in 2025, FIG, Fujitsu, and Acer Medical collaborated to digitize senior gymnastics programs using AI-powered motion analysis, enhancing early disease detection and personalized exercise recommendations, thereby driving technological innovation and advancing the preventive healthcare market.

These technologies expand access to healthcare beyond traditional settings, improve patient engagement, and support personalized care plans based on real time data. Integration of genomics and machine learning helps tailor interventions to individual risk profiles. Such advancements enhance preventive care efficacy, increase adoption by providers and consumers, and create new market segments focused on proactive health management.

Market Restraints:

A significant restraint in the Global Preventive Healthcare Market is the high initial cost and access disparities associated with advanced preventive technologies and services. Deploying state of the art diagnostic tools, AI systems, wearable health platforms, and telemedicine infrastructure requires substantial investment, which may deter adoption in lower income regions or underserved communities. Healthcare providers and insurers may face budget constraints, and out of pocket costs for individuals can be prohibitive, limiting uptake.

The preventive healthcare market significantly influences global socioeconomic outcomes by reducing the economic burden associated with chronic diseases and costly treatments. Early detection and intervention improve productivity through healthier workforces and lower absenteeism while reducing long term healthcare expenditures for individuals, insurers, and governments. It supports aging populations by managing risks and maintaining quality of life, enabling sustainable healthcare systems. Preventive care campaigns also promote health literacy and empower communities to make informed lifestyle choices. Investments in preventive technologies and services foster job creation and innovation across healthcare and tech sectors, contributing to broader economic development and equitable access to essential health services.

Segmental Analysis:

The Chronic Disease Management Technologies segment is projected to experience the highest growth over the forecast period, driven by the increasing prevalence of chronic conditions such as diabetes, cardiovascular diseases, and obesity worldwide. Rising awareness of early intervention benefits, coupled with government initiatives and insurance support, is driving adoption of remote monitoring devices, mobile health apps, AI powered analytics, and telehealth platforms for continuous patient management. These technologies help track vital parameters, predict health risks, and personalize treatment plans, improving outcomes while reducing hospitalizations and costs. Integration with wearable devices and cloud-based platforms further enhances engagement, making this segment a key growth driver.

The Payers & Health Plans segment is expected to witness the highest growth among end-users during the forecast period. Health insurers and managed care organizations are increasingly investing in preventive healthcare services and technologies to reduce long-term medical expenditures and improve population health outcomes. Initiatives include coverage for wellness programs, chronic disease management, early screenings, and digital health platforms. By incentivizing preventive measures and leveraging data-driven insights, payers can identify high-risk populations, enhance patient engagement, and optimize care delivery. Rising competition among insurers to offer value-based care solutions further accelerates market adoption, positioning this segment as a major growth contributor.

The North American Region is expected to witness the highest growth in the preventive healthcare market over the forecast period due to high healthcare expenditure, strong digital health adoption, and supportive regulatory frameworks.

The United States dominates the region, driven by government initiatives for chronic disease prevention, widespread use of telemedicine, wearable devices, and AI-powered analytics for early detection and personalized care. For instance, in July 2025, in 2025, Universitätsmedizin Berlin and Siemens Healthineers collaborated on preventive medicine, advancing patient-centered research and clinical solutions, thereby influencing North America’s preventive healthcare market by promoting innovation, adoption of advanced preventive technologies, and enhanced disease prevention strategies.

Rising awareness among consumers about preventive measures and employer-led wellness programs further boosts market expansion. Additionally, the presence of major global players and advanced healthcare infrastructure ensures continuous innovation and adoption of preventive technologies, maintaining North America’s leadership in the global market.

| Report Matrics | Details |

| Market Size Value | USD 595.6bn |

| Growth Rate | CAGR of 12.8% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The Global Preventive Healthcare Market features a diverse and competitive landscape where large pharmaceutical firms, medical device manufacturers, digital health innovators, and integrated healthcare services providers all compete and collaborate. Companies differentiate through advanced diagnostics, AI analytics, personalized care platforms, and integrated wellness solutions. Strategic partnerships, acquisitions, and technology integrations are common, as firms seek to expand capabilities and drive innovation. Major multinationals leverage established distribution networks, while tech startups disrupt with cutting edge digital tools. Competition centers on enhancing early detection accuracy, improving patient engagement, and expanding telehealth and wearable adoption, making market dynamics highly dynamic and innovation driven.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is growing because people are shifting from "treating" illness to "preventing" it. Rising rates of chronic lifestyle diseases like diabetes and heart issues are pushing individuals toward early checkups. Additionally, corporate wellness programs and new AI-driven wearable tech—like smartwatches that track heart health—make it easier for people to monitor their bodies daily and avoid expensive hospital stays.

Q2. What are the main restraining factors for this market?

The biggest challenge is the high cost of advanced screening tests and the fact that many insurance plans still don't cover "wellness" visits fully. In some regions, a lack of digital literacy stops older populations from using helpful health apps. There are also ongoing concerns about data privacy, as patients worry about how their personal health information is stored and shared online.

Q3. Which segment is expected to witness high growth?

The Early Detection and Screening segment is witnessing explosive growth. This includes everything from advanced blood tests to high-tech imaging. Additionally, AI-powered diagnostic services are a major star; they help doctors catch potential problems years earlier than traditional methods. The "individual" segment is also booming as more people take charge of their own health using mobile apps and home-testing kits.

Q4. Who are the top major players for this market?

The market is led by diversified global giants in pharma and tech. Key players include Pfizer, GlaxoSmithKline (GSK), and Abbott Laboratories, which lead in vaccines and diagnostics. Tech-heavy firms like Medtronic, Siemens Healthineers, and McKesson are also massive contributors. These companies focus on "smart" healthcare, creating tools that make preventive monitoring more accurate and easier for patients to use.

Q5. Which country is the largest player?

The United States is currently the largest player in the preventive healthcare market. This is due to a very mature healthcare infrastructure and high consumer spending on wellness. The US also benefits from strict preventive care mandates and a massive tech ecosystem where companies like Apple and Google are constantly launching new health-tracking features for a wide audience.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model