Artificial Intelligence (AI) in Precision Medicine Market Overview and Analysis

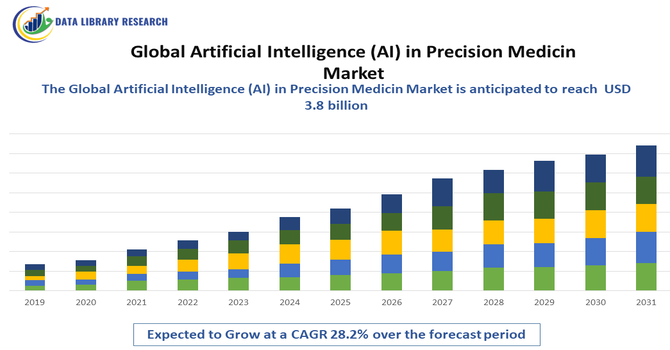

- The Global Artificial Intelligence (AI) in Precision Medicine Market reached USD 1.8 billion in 2025 and is expected to reach USD 3.8 billion by 2032, growing at a CAGR of 28.2% during the forecast period of 2025-2032.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Artificial Intelligence (AI) in Precision Medicine Market is experiencing rapid growth, driven by the increasing integration of AI algorithms in genomics, diagnostics, and personalized treatment planning to enhance patient outcomes. The market expansion is fueled by the growing availability of large-scale healthcare datasets, advancements in machine learning and deep learning technologies, and rising investments in AI-driven drug discovery and biomarker identification. The demand for predictive analytics in disease prevention, coupled with the shift toward value-based healthcare, is further propelling adoption across hospitals, research institutes, and pharmaceutical companies.

Artificial Intelligence (AI) in Precision Medicine Market Latest Trends

The latest trends in the Global Artificial Intelligence (AI) in Precision Medicine Market highlight a strong focus on the integration of multi-omics data, AI-driven biomarker discovery, and the rise of digital twins for personalized treatment simulation. There is a growing adoption of federated learning and explainable AI (XAI) to enhance transparency and data security while maintaining patient privacy in healthcare analytics. The use of generative AI for drug design and repurposing is gaining traction, significantly reducing development timelines. Cloud-based AI platforms and edge computing are improving real-time analysis of medical data, while collaborations between biotechnology companies, AI startups, and academic institutions are fostering innovation in predictive diagnostics and treatment optimization.

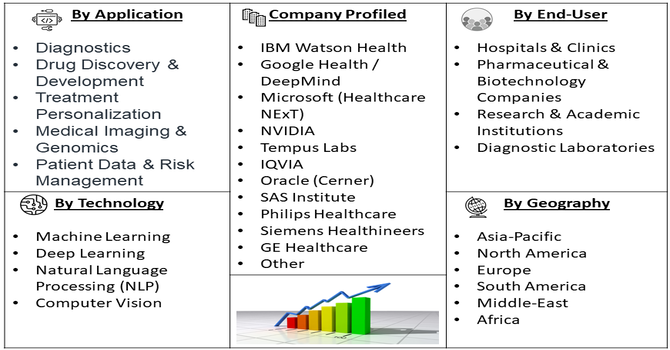

Segmentation: Global Artificial Intelligence (AI) in Precision Medicine Market is segmented By Technology (Machine Learning, Deep Learning, Natural Language Processing (NLP), Computer Vision), Application (Diagnostics, Drug Discovery & Development, Treatment Personalization, Medical Imaging & Genomics, and Patient Data & Risk Management), Component (Hardware, Software, and Services), End-User (Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Research & Academic Institutions, Diagnostic Laboratories), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

- Increasing Adoption of AI for Drug Discovery and Development

One of the primary drivers fueling the growth of the Global Artificial Intelligence (AI) in Precision Medicine Market is the rising adoption of AI technologies in drug discovery and development. Traditional drug discovery processes are time-consuming and expensive, often taking years to bring a single drug to market. AI accelerates this process by analyzing vast biological datasets, identifying molecular targets, predicting drug efficacy, and optimizing compound structures.

In October 2025, Eli Lilly and Company (NYSE: LLY) announced it had built the most powerful supercomputer owned by a pharmaceutical company, in collaboration with NVIDIA. The supercomputer powered an "AI factory," a specialized infrastructure managing the entire AI lifecycle, from data ingestion and training to fine-tuning and large-scale inference for drug discovery. Machine learning and deep learning models enable the identification of new therapeutic molecules and biomarkers, reducing R&D costs and timeframes. Pharmaceutical and biotechnology companies are increasingly leveraging AI-powered platforms to enhance precision, predict adverse effects, and improve the success rate of clinical trials, driving significant growth in the market.

- Growing Need for Personalized and Predictive Healthcare Solutions

The global healthcare industry is witnessing a paradigm shift toward personalized and predictive care, where treatment strategies are customized based on individual genetic, environmental, and lifestyle factors. AI plays a pivotal role in processing and interpreting massive amounts of genomic, proteomic, and clinical data to derive actionable insights for precision medicine. Through advanced algorithms, AI helps clinicians predict disease risks, select optimal therapies, and monitor patient responses in real time. The rising prevalence of chronic and genetic diseases, coupled with the demand for early diagnosis and targeted therapies, is driving healthcare providers and researchers to adopt AI-driven precision medicine platforms. This growing focus on individualized care is a major force propelling the expansion of the AI in precision medicine market.

Market Restraints

- High Cost and Complexity of AI Integration into Healthcare Systems

One major challenge is the high cost and complexity of AI integration into healthcare systems. Implementing AI-driven precision medicine solutions requires advanced computational infrastructure, extensive data storage, and skilled professionals—factors that can be cost-prohibitive, especially for smaller healthcare institutions. Another restraint is the lack of standardized data and interoperability across medical systems, which hampers the seamless exchange and analysis of patient information from different sources such as electronic health records, genomic databases, and imaging platforms. Additionally, data privacy and regulatory concerns pose significant barriers, as handling sensitive patient data raises ethical and compliance issues under laws such as HIPAA and GDPR. The shortage of AI-literate healthcare professionals and limited trust among clinicians in AI-based recommendations further slow down adoption. These factors collectively constrain the widespread implementation of AI in precision medicine, particularly in emerging markets.

Socio economic Impact on Artificial Intelligence (AI) in Precision Medicine Market

Artificial Intelligence (AI) in precision medicine is reshaping healthcare delivery and generating significant socioeconomic impact. By enabling personalized diagnostics, predictive treatment strategies, and accelerated drug development, AI reduces medical errors, shortens treatment timelines, and lowers healthcare costs. It enhances patient outcomes by tailoring therapies to individual genetic, molecular, and lifestyle profiles, promoting healthier populations and reducing the economic burden of chronic and complex diseases. Additionally, AI-driven innovations create high-skilled employment opportunities in biotechnology, data science, and clinical research, fostering economic growth. Widespread adoption also drives investment in healthcare infrastructure and digital technologies, strengthens public-private collaborations, and positions nations at the forefront of medical innovation, ultimately transforming both the health and economic landscape globally.

Segmental Analysis

- Machine Learning segment is expected to witness highest growth over the forecast period

The Machine Learning segment is expected to dominate the market during the forecast period due to its ability to analyze vast amounts of healthcare data and identify complex patterns within genomic, proteomic, and clinical datasets. Machine learning models assist in drug discovery, biomarker identification, and predicting patient outcomes, making it a crucial tool for advancing personalized medicine. Its widespread adoption across hospitals, pharmaceutical companies, and research institutes further accelerates market growth.

- Drug Discovery & Development segment is expected to witness highest growth over the forecast period

The Drug Discovery & Development segment holds a significant share, driven by the increasing use of AI algorithms to optimize drug design, identify new therapeutic targets, and shorten the clinical trial cycle. AI enhances the precision and efficiency of R&D processes, allowing pharmaceutical companies to reduce costs while improving success rates in drug development. This segment’s growth is supported by rising collaborations between AI firms and biotech companies for next-generation therapeutics.

- Software segment is expected to witness highest growth over the forecast period

The Software segment is projected to witness the fastest growth, as AI-powered platforms are essential for data integration, model training, and predictive analytics. These software solutions enable clinicians and researchers to visualize patient data, simulate treatment outcomes, and improve diagnostic accuracy. The continuous evolution of cloud-based AI software and integration with electronic health records (EHRs) further strengthens this segment’s expansion.

- Pharmaceutical & Biotechnology Companies segment is expected to witness highest growth over the forecast period

The Pharmaceutical & Biotechnology Companies segment leads the market, as these organizations are actively adopting AI-driven platforms to enhance drug discovery, clinical trials, and personalized treatment strategies. AI helps in understanding patient heterogeneity and predicting drug response, allowing companies to develop targeted therapies with higher efficacy. The increasing R&D investments and partnerships with AI technology providers are key growth enablers in this segment.

- North America region is expected to witness highest growth over the forecast period

North America dominates the global market, attributed to strong healthcare infrastructure, early technology adoption, and the presence of major AI and pharmaceutical companies. The U.S. in particular leads in AI-based healthcare research and clinical applications, supported by favorable government initiatives and funding.

Continuous innovation, along with rising demand for personalized and predictive healthcare, positions North America as the leading regional market for AI in precision medicine. For instance, in October 2024, Ataraxis AI, a leading AI precision medicine company, emerged from stealth mode with USD 4 million in seed funding co-led by Giant Ventures and Obvious Ventures. Raised in 2023, the funding supported Ataraxis in developing innovative AI-driven diagnostic tests designed to improve patient outcome predictions and deliver more precise, personalized treatment solutions.

In January 2025, AstraZeneca, a global pharmaceutical leader, announced a C$820 million (US$570 million) investment in Canada, creating over 700 high-skilled jobs and relocating to a larger, state-of-the-art GTA facility. Since 2023, AstraZeneca invested more than C$1.3 billion in R&D, including the C$3 billion acquisition of Fusion Pharmaceuticals. These investments accelerated clinical studies and fostered AI integration in precision medicine by enabling advanced data analytics, biomarker discovery, and personalized treatment development, strengthening Canada’s life sciences sector and advancing AI-driven innovations in oncology and patient care. Thus, such factors are fueling this market’s growth in the region.

| Report Matrics |

Details |

| Market Size Value |

USD 3.8 billion |

| Growth Rate |

CAGR of 28.2% |

| Forecast |

2026-2033 |

| Historical data |

2021-2024 |

| Base Year |

2025 |

| Report Coverage |

Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage |

Type, Application, End-User, Geography |

| Regional Scope |

North America, Europe, Asia Pacific, Middle East |

| Customized scope |

Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report |

Request a Free Sample Copy |

Artificial Intelligence (AI) in Precision Medicine Market Competitive Landscape:

The competitive landscape of the Global AI in Precision Medicine market is highly dynamic, featuring large tech firms, established healthcare vendors, and specialized AI-biotech startups — all competing through partnerships, acquisitions, platform integrations, and clinical validation to deliver AI-driven diagnostics, drug discovery, and personalized-treatment solutions. Market growth is further fueled by increasing investments in AI technologies, expanding healthcare data availability, and rising demand for precision medicine solutions. Companies are focusing on developing multimodal AI platforms, leveraging genomics, imaging, and real-world clinical data to enhance predictive accuracy, optimize treatment strategies, and reduce drug development timelines. Regulatory support, collaborations between biopharma and tech firms, and continuous innovation in machine learning algorithms are expected to drive adoption, making the market highly competitive and innovation-driven over the coming years.

Key Players:

- IBM Watson Health

- Google Health / DeepMind

- Microsoft (Healthcare NExT)

- NVIDIA

- Tempus Labs

- IQVIA

- Oracle (Cerner)

- SAS Institute

- Philips Healthcare

- Siemens Healthineers

- GE Healthcare

- Amazon Web Services (AWS) Healthcare

- Illumina

- GNS Healthcare

- BenevolentAI

- Recursion Pharmaceuticals

- PathAI

- Owkin

- Berg Health

- Flatiron Health

Recent Development:

- In October 2025, Guardant Health and Zephyr AI, a precision medicine firm leveraging artificial intelligence, announced a strategic partnership to deliver scalable, actionable insights supporting biopharmaceutical innovation. The collaboration combined their multimodal molecular data and AI/ML technologies to advance novel cancer biomarkers, guide targeted therapy selection, and enable response monitoring. Integrated with Guardant’s Infinity AI capabilities, the partnership demonstrated both companies’ commitment to using AI and multimodal data to empower oncologists, researchers, and biopharma developers in transforming cancer patient care.

- In April 2025, Precision for Medicine, and PathAI, a global digital pathology leader, announced a strategic collaboration to develop AI-based technologies and integrate PathAI’s advanced pathology capabilities into Precision for Medicine’s clinical trial and biospecimen operations. The partnership utilized several PathAI technologies and established an agreement to offer novel tools and analytical services for biomarker discovery, spatial biology, and tissue-based research. PathAI’s tools augmented Precision for Medicine’s proprietary pipeline, giving biopharma clients access to enhanced imaging workflows within its integrated laboratory and clinical trial services.

Frequently Asked Questions (FAQ) :

Q1. What are the main growth-driving factors for this market?

The primary growth drivers are the immense advancements in genomic research and the resulting availability of vast multi-omics and clinical datasets. AI, through deep learning and predictive analytics, is crucial for integrating and interpreting this complex information to identify biomarkers and customize treatments. Furthermore, the rising global prevalence of chronic diseases like cancer, the increasing demand for personalized medication, and significant investments from government and private sectors into R&D are fundamentally accelerating market growth.

Q2. What are the main restraining factors for this market?

Key restraints include the high initial capital investment required for implementing AI infrastructure, specialized software, and training personnel in healthcare settings. Compounding this challenge are critical data privacy and security concerns surrounding the handling of sensitive patient information (like genomic and EHR data), particularly in regions with stringent regulations such as GDPR and HIPAA. These factors create economic and regulatory hurdles that limit widespread adoption, especially among smaller institutions.

Q3. Which segment is expected to witness high growth?

By technology, the Natural Language Processing (NLP) segment is projected to witness the highest growth, as it is essential for extracting crucial, unstructured clinical insights from physician notes and electronic health records (EHRs). By therapeutic area, Neurology is also anticipated to show a very high growth rate due to the increasing incidence of complex neurological disorders like Alzheimer's and the pressing need for AI to accelerate early diagnosis and personalized treatment planning.

Q4. Who are the top major players for this market?

The market is led by a mix of technology giants and specialized health-tech firms. Top major players include NVIDIA Corporation (for high-performance computing hardware), Google Inc. (Alphabet), and Microsoft Corporation (for cloud platforms and AI tools). Specialized companies like Tempus AI (focused on oncology data), IBM (with its Watson Health initiatives), and Illumina (in genomics) are also fundamental contributors to the AI in precision medicine ecosystem.

Q5. Which country is the largest player?

North America, with the United States as the dominant country, holds the largest market share by revenue. This leadership is fueled by the region's highly sophisticated healthcare and IT infrastructure, substantial R&D funding in both AI and genomics, and the strong presence of major technology and pharmaceutical corporations. A favorable regulatory environment that actively promotes the integration of AI solutions into clinical practice further solidifies its market position.

List of Figures

Figure 1: Global Artificial Intelligence (AI) in Precision Medicine Market Revenue Breakdown (USD Billion, %) by Region, 2022 & 2029

Figure 2: Global Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 1, 2022 & 2029

Figure 3: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 4: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 5: Global Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 2, 2022 & 2029

Figure 6: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 7: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 8: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 9: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 10: Global Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 3, 2022 & 2029

Figure 11: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 12: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 13: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 14: Global Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 15: Global Artificial Intelligence (AI) in Precision Medicine Market Value (USD Billion), by Region, 2022 & 2029

Figure 16: North America Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 1, 2022 & 2029

Figure 17: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 18: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 19: North America Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 2, 2022 & 2029

Figure 20: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 21: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 22: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 23: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 24: North America Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 3, 2022 & 2029

Figure 25: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 26: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 27: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 28: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 29: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by U.S., 2018-2029

Figure 30: North America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Canada, 2018-2029

Figure 31: Latin America Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 1, 2022 & 2029

Figure 32: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 33: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 34: Latin America Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 2, 2022 & 2029

Figure 35: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 36: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 37: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 38: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 39: Latin America Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 3, 2022 & 2029

Figure 40: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 41: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 42: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 43: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 44: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Brazil, 2018-2029

Figure 45: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Mexico, 2018-2029

Figure 46: Latin America Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Rest of Latin America, 2018-2029

Figure 47: Europe Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 1, 2022 & 2029

Figure 48: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 49: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 50: Europe Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 2, 2022 & 2029

Figure 51: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 52: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 53: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 54: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 55: Europe Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 3, 2022 & 2029

Figure 56: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 57: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 58: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 59: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 60: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by U.K., 2018-2029

Figure 61: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Germany, 2018-2029

Figure 62: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by France, 2018-2029

Figure 63: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Italy, 2018-2029

Figure 64: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Spain, 2018-2029

Figure 65: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Russia, 2018-2029

Figure 66: Europe Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Rest of Europe, 2018-2029

Figure 67: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 1, 2022 & 2029

Figure 68: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 69: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 70: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 2, 2022 & 2029

Figure 71: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 72: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 73: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 74: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 75: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 3, 2022 & 2029

Figure 76: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 77: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 78: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 79: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 80: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by China, 2018-2029

Figure 81: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by India, 2018-2029

Figure 82: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Japan, 2018-2029

Figure 83: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Australia, 2018-2029

Figure 84: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Southeast Asia, 2018-2029

Figure 85: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Rest of Asia Pacific, 2018-2029

Figure 86: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 1, 2022 & 2029

Figure 87: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 88: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 89: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 2, 2022 & 2029

Figure 90: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 91: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 92: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 93: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 94: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Value Share (%), By Segment 3, 2022 & 2029

Figure 95: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 96: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 97: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 98: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Others, 2018-2029

Figure 99: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by GCC, 2018-2029

Figure 100: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by South Africa, 2018-2029

Figure 101: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Forecast (USD Billion), by Rest of Middle East & Africa, 2018-2029

List of Tables

Table 1: Global Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 2: Global Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 3: Global Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 4: Global Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Region, 2018-2029

Table 5: North America Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 6: North America Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 7: North America Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 8: North America Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 9: Europe Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 10: Europe Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 11: Europe Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 12: Europe Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 13: Latin America Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 14: Latin America Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 15: Latin America Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 16: Latin America Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 17: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 18: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 19: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 20: Asia Pacific Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 21: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 22: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 23: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 24: Middle East & Africa Artificial Intelligence (AI) in Precision Medicine Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Research Process

Data Library Research are conducted by industry experts who offer insight on

industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager

and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

![research-methodology1]()

Primary Research

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary Research

Secondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size Estimation

Both, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model

![research-methodology2]()