Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Peptide CDMO Pharmaceutical Market involves outsourcing peptide drug development and manufacturing services, enabling biopharmaceutical companies to access large-scale, cost-efficient production, advanced technology, and expertise for therapeutic peptides.

The Global Peptide CDMO (Contract Development and Manufacturing Organization) Pharmaceutical Market is witnessing significant growth, primarily driven by the increasing demand for peptide-based therapeutics across various therapeutic areas such as oncology, metabolic disorders, and infectious diseases. Rising investments by pharmaceutical and biotechnology companies in peptide drug development, coupled with the growing complexity of peptide synthesis and the need for specialized manufacturing expertise, are fueling the reliance on CDMOs. Additionally, the expansion of biologics and personalized medicine, along with the rising trend of outsourcing to reduce R&D costs and accelerate time-to-market, is further propelling the growth of the peptide CDMO market globally.

The latest trends in the Global Peptide CDMO Pharmaceutical Market include a growing emphasis on customized and scalable peptide synthesis solutions, enabling pharmaceutical companies to develop complex and high-purity peptides efficiently. There is an increasing adoption of advanced peptide manufacturing technologies, such as solid-phase peptide synthesis (SPPS), flow chemistry, and continuous manufacturing, which improve yield, reduce production time, and ensure consistent quality. Additionally, CDMOs are expanding their capabilities to offer integrated services, including analytical testing, formulation development, and regulatory support, allowing end-to-end outsourcing solutions. Strategic collaborations and partnerships between peptide developers and CDMOs are also on the rise, helping to accelerate drug development pipelines and support the growing demand for peptide therapeutics in precision medicine.

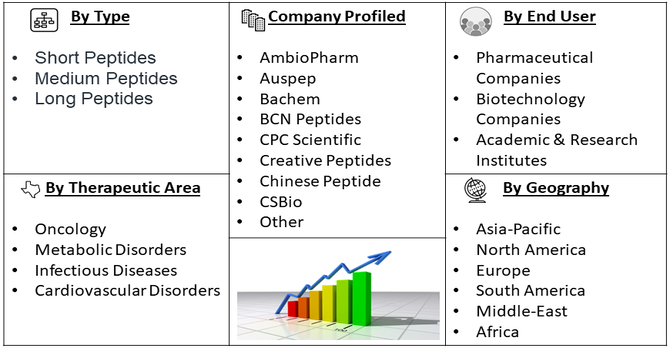

Segmentation: Global Peptide CDMO Pharmaceutical Market is segmented By Peptide Type (Short Peptides ,Medium Peptides, Long Peptides), Service Type (Peptide Synthesis, Peptide Purification, Analytical & Testing Services, Formulation & Fill-Finish Services), Therapeutic Area (Oncology, Metabolic Disorders, Infectious Diseases, Cardiovascular Disorders), End-User (Pharmaceutical Companies, Biotechnology Companies, Academic & Research Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing prevalence of chronic and complex diseases such as cancer, diabetes, cardiovascular disorders, and infectious diseases is driving the demand for peptide-based therapeutics. Peptides are highly specific, potent, and generally exhibit fewer side effects compared to conventional small-molecule drugs, making them attractive candidates for targeted therapy.

In August 2025, BioMed X, an independent biomedical research institute in Heidelberg, Germany, announced a collaboration with Novo Nordisk to tackle the challenge of efficient oral delivery of therapeutic peptides. A dedicated research team was formed, supported by both organizations, to advance this initiative. The partnership strengthened R&D capabilities, accelerated development of novel peptide formulations, and enhanced outsourcing opportunities for CDMOs. By improving delivery technologies, it expanded market potential, increased demand for specialized manufacturing services, and supported innovation and growth in the global peptide pharmaceutical sector. The growing adoption of peptide therapeutics across various therapeutic areas is therefore a significant growth driver for the market.

Pharmaceutical and biotech companies are increasingly outsourcing peptide development and manufacturing to CDMOs to reduce operational costs, optimize resource utilization, and accelerate time-to-market. Outsourcing enables companies to leverage specialized equipment, advanced manufacturing technologies, and regulatory expertise without investing heavily in in-house infrastructure.

In November 2024, Asymchem announced the development of automated peptide manufacturing, optimizing reactant suspension and mixing with resins through specially designed synthesizers and deploying a host computer system that enabled fully unmanned solid-phase synthesis production.This innovation enhanced efficiency, scalability, and reliability in peptide production, encouraging pharmaceutical companies to outsource manufacturing and development activities. By minimizing manual intervention, reducing production risks, and lowering operational costs, it accelerated timelines and strengthened trust in CDMO partnerships, thereby driving growth in the global peptide CDMO market and supporting wider adoption of outsourced biopharmaceutical development and manufacturing solutions.

Market Restraints:

Peptide synthesis and manufacturing are technically challenging, involving precise amino acid sequencing, complex purification processes, and stringent quality control measures. The requirement for specialized equipment, skilled personnel, and advanced technologies, such as solid-phase peptide synthesis (SPPS) and liquid-phase synthesis, increases production costs significantly. These high operational expenses can act as a barrier, particularly for small and mid-sized CDMOs, limiting their ability to compete or expand services.

The Global Peptide CDMO (Contract Development and Manufacturing Organization) Pharmaceutical Market has had significant socioeconomic impacts, driven by the rising demand for therapeutic peptides in treating chronic diseases such as diabetes, obesity, and cancer. Increased investment in peptide development and large-scale manufacturing has created high-skilled employment opportunities across biotechnology, pharmaceutical production, and research sectors, stimulating local and regional economies. The availability of CDMO services reduces drug development costs and accelerates time-to-market, making advanced therapies more accessible and affordable. Socially, these developments improve patient outcomes and public health by providing innovative treatments more efficiently. Furthermore, the market promotes technological innovation, sustainable manufacturing practices, and global collaboration, contributing to the growth of the biopharmaceutical industry and broader socioeconomic development worldwide.

Segmental Analysis:

Short peptides, typically composed of fewer than 20 amino acids, are widely utilized in research and therapeutic applications due to their ease of synthesis and high biological activity. They are commonly used in oncology, metabolic disorder treatments, and vaccine development. The relatively simpler structure and lower production costs compared to medium and long peptides make short peptides highly attractive for pharmaceutical and biotechnology companies, driving significant demand for CDMO services in their development and manufacturing.

Peptide synthesis is a core service offered by CDMOs and involves the construction of peptide chains through solid-phase or liquid-phase techniques. The complexity of peptide sequences and the need for high-purity products make outsourcing synthesis to specialized CDMOs essential for many pharmaceutical companies. Advanced synthesis technologies, scalability, and expertise in handling complex sequences are major factors contributing to the growth of this service segment.

Oncology is a key therapeutic area driving demand for peptide therapeutics. Peptides are used as targeted therapies, cancer vaccines, and drug delivery vehicles, offering specificity and reduced side effects compared to traditional chemotherapy. The increasing prevalence of cancer globally, coupled with rising investments in peptide-based oncology drug development, is fueling growth for CDMOs specializing in oncology peptides.

Biotechnology companies are major consumers of peptide CDMO services due to their focus on developing innovative and complex peptide therapeutics. These companies often lack large-scale manufacturing infrastructure and rely on CDMOs for synthesis, purification, and analytical support. The growing number of biotech startups and their emphasis on research-intensive peptide therapeutics are driving the demand for outsourced development and manufacturing services.

The North America region is expected to witness the highest growth over the forecast period in the Global Peptide CDMO Pharmaceutical Market. This growth is driven by the region’s well-established pharmaceutical and biotechnology ecosystem, high R&D investments, and strong adoption of peptide-based therapeutics across oncology, metabolic disorders, and infectious diseases.

In June 2025, Valo Therapeutics Oy (ValoTx), a clinical-stage biotechnology company, announced encouraging interim results from its ongoing Phase 1 clinical trial, START (Safety and Anti-Tumor Activity of PeptiCRAd-1 in Cancer, NCT05492682), evaluating its oncolytic virus-based cancer immunotherapy. The positive trial outcomes highlighted the growing demand for peptide-based therapeutics, driving outsourcing of peptide manufacturing and development. This trend accelerated engagement with CDMOs, boosted market growth, and encouraged investment in scalable, high-quality peptide production, supporting innovation and expansion within the global peptide pharmaceutical and contract development sectors. Additionally, the presence of advanced manufacturing infrastructure, specialized CDMOs with expertise in peptide synthesis and formulation, and supportive regulatory frameworks are further accelerating market expansion. The increasing number of biotech startups and strategic collaborations with CDMOs to outsource complex peptide development are also contributing significantly to the region’s leading position.

| Report Matrics | Details |

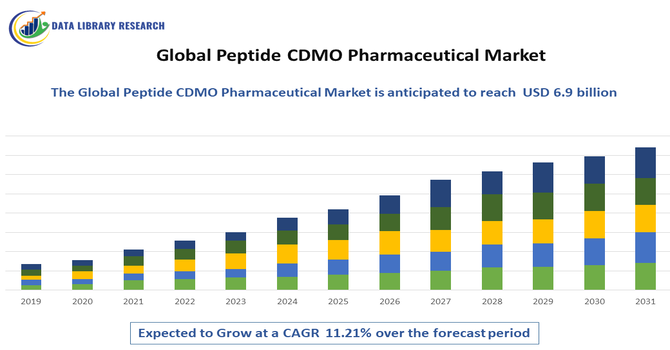

| Market Size Value | USD 6.9 billion |

| Growth Rate | CAGR of 11.21% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The Global Peptide CDMO Pharmaceutical Market is highly competitive, driven by the increasing demand for peptide-based therapeutics and the complexity of peptide synthesis and manufacturing. Key players focus on offering end-to-end services, including synthesis, purification, formulation, and regulatory support, while leveraging advanced technologies to ensure high-quality, scalable production. Strategic partnerships, collaborations, and investments in capacity expansion and technological innovations are shaping the market landscape and enabling CDMOs to meet the growing needs of pharmaceutical and biotechnology companies worldwide.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The peptide CDMO market is experiencing robust growth driven primarily by the rising global demand for complex peptide therapeutics, particularly for chronic diseases like diabetes, cancer, and obesity. Pharmaceutical and biotech companies are increasingly outsourcing development and manufacturing to specialized CDMOs to leverage their technical expertise, reduce high capital expenditure, and accelerate time-to-market. Additionally, ongoing advancements in peptide synthesis technologies, such as solid-phase peptide synthesis (SPPS), are enabling more efficient and scalable production.

Q2. What are the main restraining factors for this market?

The chief restraint is the high cost and complexity of manufacturing therapeutic-grade peptides. Peptide synthesis is significantly more expensive than small molecule production, requiring specialized equipment, expensive raw materials, and lengthy, challenging purification processes to achieve stringent regulatory purity standards. These elevated production costs can limit the commercial viability of certain peptide drugs and restrict access in price-sensitive regions, posing a continuous challenge for CDMOs.

Q3. Which segment is expected to witness high growth?

The Contract Development service segment is anticipated to witness high growth, driven by the increasing complexity of new peptide drug candidates which require specialized R&D services, including process optimization, formulation development, and advanced analytical testing. By end-user, the Biopharmaceutical Companies segment will also show robust expansion as smaller biotech firms heavily rely on CDMO expertise and infrastructure to move their complex peptide pipeline through clinical trials.

Q4. Who are the top major players for this market?

The market is dominated by global CDMOs known for their specialized capabilities in complex synthesis and GMP compliance. Key major players include Bachem Holding AG, PolyPeptide Group, Lonza Group AG, CordenPharma International, and Thermo Fisher Scientific (Patheon). These companies maintain their competitive edge by continually investing in advanced manufacturing capacity and proprietary peptide synthesis technologies to handle the increasing volume and complexity of therapeutic peptides.

Q5. Which country is the largest player?

North America holds the largest market share by revenue, with the United States being the dominant country. This leadership is attributed to a highly mature biopharmaceutical ecosystem, extensive research and development (R&D) investments, and the significant presence of major pharmaceutical and biotech companies. Favorable regulatory policies from agencies like the FDA further position the U.S. as a preferred hub for complex peptide drug development and contract manufacturing.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model