Autonomous Vehicle Operations Specialist Market Overview and Analysis

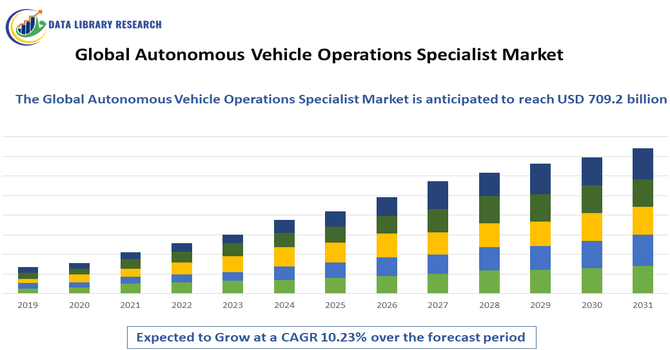

The Global Autonomous Vehicle Operations Specialist Market revenue was valued at USD 283.75 billion in 2026 and is expected to attain around USD 709.2 billion in 2033, growing with a CAGR of 10.23% from 2026-2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Autonomous Vehicle Operations Specialist Market refers to the expanding industry that supplies professionals responsible for overseeing, monitoring, and optimizing operations of autonomous vehicles (AVs). These specialists ensure safe AV deployment, manage remote supervision systems, interpret vehicle performance data, and coordinate responses to technical or environmental challenges. Rising adoption of self-driving cars, delivery robots, and autonomous public transport fuels demand for skilled operators across automotive, logistics, tech, and government sectors.

Autonomous Vehicle Operations Specialist Market Latest Trends

The Global Autonomous Vehicle Operations Specialist market is shaped by rapid technological evolution in AI, machine learning, and sensor systems that enable greater autonomy. Increasing pilot programs for self-driving taxis, trucks, and last-mile delivery vehicles are driving demand for remote operations specialists who can monitor fleets in real time. Partnerships between automotive OEMs, tech firms, and logistics companies expand opportunities for specialized operational roles. Regulatory frameworks are gradually maturing, encouraging deployments while emphasizing safety oversight. Additionally, cloud-based teleoperation platforms and data analytics tools are becoming standard, requiring specialists with hybrid technical and operational skills. Workforce training programs are rapidly emerging to meet this demand.

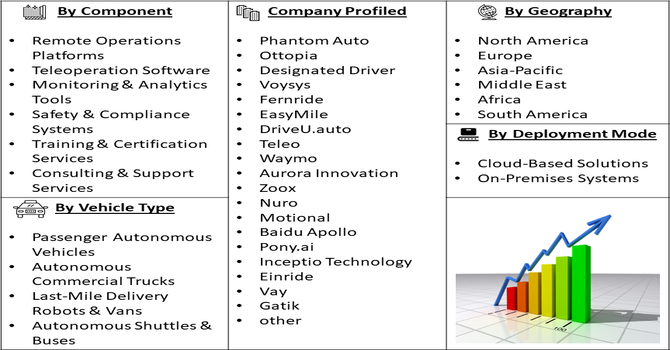

Segmentation: The Global Autonomous Vehicle Operations Specialist Market is segmented by Component (Remote Operations Platforms, Teleoperation Software, Monitoring & Analytics Tools, Safety & Compliance Systems, Training & Certification Services and Consulting & Support Services), Vehicle Type (Passenger Autonomous Vehicles (Robotaxis, Cars), Autonomous Commercial Trucks, Last-Mile Delivery Robots & Vans, Autonomous Shuttles & Buses and ndustrial Autonomous Vehicles (AGVs, forklifts)), Deployment Mode (Cloud-Based Solutions and On-Premises Systems), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

- Rapid Expansion of Autonomous Vehicle Deployments

The accelerating deployment of autonomous vehicles across passenger transport, logistics, and industrial applications is a major driver for the Global Autonomous Vehicle Operations Specialist Market. Robotaxis, autonomous trucks, delivery robots, and shuttles require continuous human oversight to ensure safety, efficiency, and regulatory compliance.

In December 2025, Recent service disruptions involving Waymo’s autonomous vehicles in San Francisco highlighted critical connectivity risks and impacted the Global Autonomous Vehicle Operations Specialist Market and the rapid expansion of autonomous vehicle deployments. Reliance on a single network limited operational resilience during outages, increasing the need for specialists to manage network redundancy, remote intervention, and contingency planning, while underscoring connectivity robustness as a key requirement for scalable autonomous mobility. As pilot projects transition into commercial-scale operations, fleet sizes increase, significantly raising demand for trained specialists.

- Increasing Focus on Safety, Regulation, and Human Oversight

Heightened emphasis on safety and regulatory compliance is driving the need for autonomous vehicle operations specialists. Governments and transportation authorities often mandate human-in-the-loop supervision to manage complex traffic scenarios, cybersecurity risks, and system failures. Operations specialists provide real-time decision-making support, ensuring vehicles respond appropriately to unpredictable road conditions. Public acceptance of autonomous technology also depends on visible safety controls, which these specialists help maintain. As regulations evolve, companies must employ skilled professionals to interpret compliance requirements, manage reporting, and implement operational safeguards, making specialized operational roles a critical component of autonomous vehicle deployment strategies.

Market Restraints:

- Shortage of Skilled Workforce and High Training Costs

A key restraint facing the Global Autonomous Vehicle Operations Specialist Market is the limited availability of skilled professionals and the high cost of training. Operating autonomous vehicle systems requires a multidisciplinary skill set combining software understanding, real-time decision-making, safety protocols, and regulatory knowledge. Developing such expertise demands extensive training programs, simulation tools, and ongoing certification, increasing operational expenses for companies. Smaller firms and startups may struggle to attract or retain qualified specialists due to competition from large technology companies.

Socioeconomic Impact on Autonomous Vehicle Operations Specialist Market

The rise of autonomous vehicle operations specialists has significant socioeconomic implications. As AV deployments grow, these specialists create new skilled employment opportunities across urban and rural regions, reducing geographic labor imbalances. They increase transportation safety by managing remote interventions and automated systems, potentially lowering accident rates and healthcare costs. However, the shift toward autonomy also disrupts traditional driving and logistics jobs, necessitating reskilling initiatives and social safety nets. Broader adoption can improve mobility access for the elderly and disabled, boosting inclusion.

Segmental Analysis:

- Remote Operations Platforms segment is expected to witness highest growth over the forecast period

The Remote Operations Platforms segment is expected to witness the highest growth over the forecast period due to their critical role in ensuring safe and efficient autonomous vehicle deployment. These platforms enable real-time monitoring, remote intervention, diagnostics, and performance optimization across large autonomous fleets. As autonomous systems still face edge cases and unpredictable environments, human-in-the-loop oversight remains essential. Growing fleet sizes in robotaxis, delivery vehicles, and autonomous trucks are increasing demand for scalable, centralized control systems. Advancements in low-latency connectivity, AI-driven alerts, and integrated analytics further enhance platform capabilities, making remote operations solutions indispensable for commercial autonomous vehicle operations.

- Autonomous Commercial Trucks segment is expected to witness highest growth over the forecast period

The Autonomous Commercial Trucks segment is expected to witness the highest growth over the forecast period, driven by rising demand for efficient freight transportation and persistent driver shortages. Logistics companies are increasingly adopting autonomous trucking solutions to reduce operating costs, improve delivery reliability, and support long-haul operations. However, these vehicles require continuous supervision to manage complex highway conditions, border crossings, and emergency scenarios. Autonomous vehicle operations specialists play a key role in remote monitoring, route optimization, and safety compliance. Growing investments in autonomous freight corridors and regulatory approvals for pilot programs are further accelerating demand for operational expertise in this segment.

- Cloud-based segment is expected to witness highest growth over the forecast period

The Cloud-based segment is expected to witness the highest growth over the forecast period due to its scalability, flexibility, and cost-effectiveness. Cloud platforms enable centralized management of autonomous vehicle fleets, real-time data processing, and seamless software updates across multiple locations. They support advanced analytics, AI-driven decision-making, and remote collaboration among operations specialists. As fleets expand, cloud-based solutions allow companies to scale operations without heavy infrastructure investments. Additionally, integration with IoT, 5G connectivity, and cybersecurity frameworks enhances reliability and performance. The shift toward software-defined vehicles and remote workforce models further strengthens adoption of cloud-based autonomous operations systems.

- North American Region is expected to witness highest growth over the forecast period

The North American region is expected to witness the highest growth over the forecast period due to strong technological infrastructure, early adoption of autonomous mobility, and significant investments by leading automotive and technology companies.

The presence of major autonomous vehicle developers, logistics firms, and teleoperation platform providers supports rapid commercialization. For instance, in October 2023, Uber’s integration of Waymo’s self-driving vehicle service into its platform accelerated the growth of the Global Autonomous Vehicle Operations Specialist Market. The launch of robotaxi booking in Phoenix increased demand for specialists to manage fleet supervision, remote assistance, safety monitoring, and service reliability, reinforcing the importance of human oversight in large-scale autonomous mobility operations.

Favorable regulatory frameworks in the United States and Canada encourage pilot programs and large-scale deployments of robotaxis and autonomous trucks. Additionally, rising demand for efficient freight transportation, smart mobility solutions, and safety-driven operations is boosting the need for autonomous vehicle operations specialists across the region.

| Report Matrics |

Details |

| Market Size Value |

USD 709.2 billion |

| Growth Rate |

CAGR of 10.23% |

| Forecast |

2026-2033 |

| Historical data |

2021-2024 |

| Base Year |

2025 |

| Report Coverage |

Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage |

Type, Application, End-User, Geography |

| Regional Scope |

North America, Europe, Asia Pacific, Middle East |

| Customized scope |

Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report |

Request a Free Sample Copy |

Autonomous Vehicle Operations Specialist Market Competitive Landscape

The competitive landscape of the autonomous vehicle operations specialist market is diverse, encompassing tech giants, automotive manufacturers, logistics firms, and specialized service providers. Major autonomous system developers compete to build robust remote operation platforms, while cloud and AI vendors offer analytics and teleoperation tools that differentiate service offerings. Training and certification bodies vie to become standard-setters for workforce readiness. Startups focusing on niche teleoperation solutions challenge established players by offering agility and targeted features. Strategic alliances and acquisitions are common as companies seek to scale capabilities. Competitive advantage rests on technological integration, regulatory compliance expertise, talent development, and the ability to support large, distributed AV fleets.

The major players for above market are:

- Phantom Auto

- Ottopia

- Designated Driver

- Voysys

- Fernride

- EasyMile

- DriveU.auto

- Teleo

- Waymo

- Aurora Innovation

- Zoox

- Nuro

- Motional

- Baidu Apollo

- Pony.ai

- Inceptio Technology

- Einride

- Vay

- Gatik

Recent Development

- In September 2024, Peachtree Corners, among the first smart city networks in the United States built on T-Mobile’s 5G and connected infrastructure, collaborated with May Mobility to deploy autonomous vehicles. As part of this partnership, May Mobility launched its on-demand autonomous transportation service, marking its first operational deployment in the state of Georgia.

- In May 2024, Renault Group unveiled a Level 4 autonomous vehicle designed for use in public transportation systems. While the company continues to advance ADAS technologies to enhance vehicle safety and passenger comfort, it emphasized that achieving full autonomy is essential to meet the growing demand for zero-emission solutions in public transit networks.

Frequently Asked Questions (FAQ) :

Q1. What are the main growth-driving factors for this market?

Rapid advancements in AI and sensor technology are primary drivers, as companies shift from testing to commercial deployment. Increasing demand for "Robotaxis" and autonomous logistics solutions necessitates skilled human operators. Furthermore, heavy investment from tech giants and automotive OEMs accelerates the need for specialized personnel to manage fleet safety and performance.

Q2. What are the main restraining factors for this market?

Regulatory uncertainty and fragmented safety standards across different regions remain significant hurdles. Public skepticism regarding the safety of self-driving technology can also slow adoption. Additionally, the high cost of training specialized personnel and the technical complexity of maintaining diverse AV fleets can strain the budgets of smaller startups in the sector.

Q3. Which segment is expected to witness high growth?

The "Remote Operations and Teleoperation" segment is expected to witness the highest growth. As fully driverless vehicles face edge-case scenarios they cannot solve alone, human specialists must intervene remotely. This "human-in-the-loop" infrastructure is critical for the legal and operational scaling of autonomous delivery services and urban ride-hailing networks.

Q4. Who are the top major players for this market?

The market is led by industry pioneers like Waymo (Alphabet), Cruise (GM), and Zoox (Amazon). Other key players include Aurora Innovation, Motional, and Baidu’s Apollo. These companies employ vast teams of operations specialists to monitor vehicle health, analyze sensor data, and manage the complex logistics of large-scale autonomous fleet testing.

Q5. Which country is the largest player?

The United States is currently the largest player in this market. This is due to a high concentration of autonomous vehicle headquarters in Silicon Valley, supportive testing regulations in states like Arizona and California, and massive venture capital flow. The U.S. remains the primary hub for early-stage commercial AV deployments.

List of Figures

Figure 1: Global Autonomous Vehicle Operations Specialist Market Revenue Breakdown (USD Billion, %) by Region, 2022 & 2029

Figure 2: Global Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 1, 2022 & 2029

Figure 3: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 4: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 5: Global Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 2, 2022 & 2029

Figure 6: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 7: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 8: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 9: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 10: Global Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 3, 2022 & 2029

Figure 11: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 12: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 13: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 14: Global Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 15: Global Autonomous Vehicle Operations Specialist Market Value (USD Billion), by Region, 2022 & 2029

Figure 16: North America Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 1, 2022 & 2029

Figure 17: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 18: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 19: North America Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 2, 2022 & 2029

Figure 20: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 21: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 22: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 23: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 24: North America Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 3, 2022 & 2029

Figure 25: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 26: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 27: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 28: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 29: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by U.S., 2018-2029

Figure 30: North America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Canada, 2018-2029

Figure 31: Latin America Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 1, 2022 & 2029

Figure 32: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 33: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 34: Latin America Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 2, 2022 & 2029

Figure 35: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 36: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 37: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 38: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 39: Latin America Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 3, 2022 & 2029

Figure 40: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 41: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 42: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 43: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 44: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Brazil, 2018-2029

Figure 45: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Mexico, 2018-2029

Figure 46: Latin America Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Rest of Latin America, 2018-2029

Figure 47: Europe Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 1, 2022 & 2029

Figure 48: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 49: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 50: Europe Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 2, 2022 & 2029

Figure 51: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 52: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 53: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 54: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 55: Europe Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 3, 2022 & 2029

Figure 56: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 57: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 58: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 59: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 60: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by U.K., 2018-2029

Figure 61: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Germany, 2018-2029

Figure 62: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by France, 2018-2029

Figure 63: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Italy, 2018-2029

Figure 64: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Spain, 2018-2029

Figure 65: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Russia, 2018-2029

Figure 66: Europe Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Rest of Europe, 2018-2029

Figure 67: Asia Pacific Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 1, 2022 & 2029

Figure 68: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 69: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 70: Asia Pacific Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 2, 2022 & 2029

Figure 71: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 72: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 73: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 74: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 75: Asia Pacific Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 3, 2022 & 2029

Figure 76: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 77: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 78: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 79: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 80: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by China, 2018-2029

Figure 81: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by India, 2018-2029

Figure 82: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Japan, 2018-2029

Figure 83: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Australia, 2018-2029

Figure 84: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Southeast Asia, 2018-2029

Figure 85: Asia Pacific Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Rest of Asia Pacific, 2018-2029

Figure 86: Middle East & Africa Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 1, 2022 & 2029

Figure 87: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 88: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 89: Middle East & Africa Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 2, 2022 & 2029

Figure 90: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 91: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 92: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 93: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 94: Middle East & Africa Autonomous Vehicle Operations Specialist Market Value Share (%), By Segment 3, 2022 & 2029

Figure 95: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 96: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 97: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 98: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Others, 2018-2029

Figure 99: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by GCC, 2018-2029

Figure 100: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by South Africa, 2018-2029

Figure 101: Middle East & Africa Autonomous Vehicle Operations Specialist Market Forecast (USD Billion), by Rest of Middle East & Africa, 2018-2029

List of Tables

Table 1: Global Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 2: Global Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 3: Global Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 4: Global Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Region, 2018-2029

Table 5: North America Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 6: North America Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 7: North America Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 8: North America Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 9: Europe Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 10: Europe Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 11: Europe Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 12: Europe Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 13: Latin America Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 14: Latin America Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 15: Latin America Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 16: Latin America Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 17: Asia Pacific Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 18: Asia Pacific Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 19: Asia Pacific Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 20: Asia Pacific Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 21: Middle East & Africa Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 22: Middle East & Africa Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 23: Middle East & Africa Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 24: Middle East & Africa Autonomous Vehicle Operations Specialist Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Research Process

Data Library Research are conducted by industry experts who offer insight on

industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager

and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

![research-methodology1]()

Primary Research

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary Research

Secondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size Estimation

Both, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model

![research-methodology2]()