Get Complete Analysis Of The Report - Download Updated Free Sample PDF

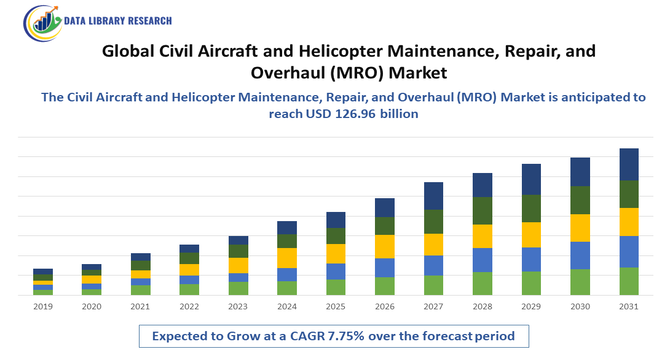

The Global Civil Aircraft and Helicopter Maintenance, Repair, and Overhaul (MRO) Market involves services that keep commercial airplanes and helicopters safe, functional, and efficient. It includes routine inspections, repairs, component replacements, and upgrades. Growing air travel, stricter safety regulations, and the need to extend aircraft lifespan drive demand for MRO services, making them critical for airlines and aviation operators worldwide.

The growth of the global civil aircraft and helicopter MRO market is driven by rising air travel demand, which increases aircraft utilization and maintenance needs. Strict aviation safety regulations and compliance standards compel airlines to perform regular inspections and repairs. Aging fleets require more frequent overhauls and component replacements to extend service life. Additionally, technological advancements in predictive maintenance, engine diagnostics, and aircraft monitoring systems enhance efficiency and reduce downtime, further boosting market growth globally.

The civil aircraft and helicopter MRO market has been witnessing several key trends. Airlines are increasingly adopting predictive and condition-based maintenance powered by AI, IoT, and big data analytics to reduce downtime and costs. Outsourcing MRO services to specialized third-party providers is growing due to operational efficiency and expertise advantages. There is a rising focus on sustainable and eco-friendly practices, including lightweight components and fuel-efficient engine maintenance. Additionally, regional hubs are expanding, with Asia-Pacific seeing significant growth due to increasing air traffic and fleet expansions. Technological integration and automation are shaping the future of MRO operations globally.

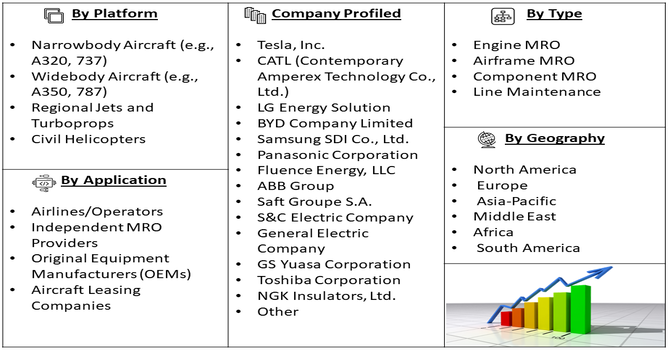

Segmentation: The Civil Aircraft and Helicopter MRO market is segmented by MRO Service Type (Engine MRO, Airframe MRO, Component MRO and Line Maintenance), Aircraft Platform (Narrowbody Aircraft (e.g., A320, 737), Widebody Aircraft (e.g., A350, 787), Regional Jets and Turboprops and Civil Helicopters), End-User (Airlines/Operators, Independent MRO Providers, Original Equipment Manufacturers (OEMs) and Aircraft Leasing Companies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The global civil aircraft and helicopter MRO market was strongly driven by rising air travel demand and fleet expansion, particularly in emerging economies. As more people chose air transport for business and leisure, airlines increased utilization of aircraft, leading to higher maintenance requirements. For instance, in October 2024, Safran Aircraft Engines announced over EUR 1 billion in investments to expand its global MRO network, aiming to support the growing LEAP engine fleet. The investment enhanced Safran’s maintenance, repair, and overhaul capabilities, addressing rising demand for aftersales services. As LEAP engines power nearly 4,000 narrowbody aircraft, including Airbus A320neo, Boeing 737 MAX, and COMAC C919, this expansion strengthened the global civil aircraft and helicopter MRO market by boosting service capacity and operational readiness.

Simultaneously, many carriers expanded their fleets with both fixed-wing aircraft and helicopters. The growing size of aging fleets required more frequent inspections, repairs, and overhauls to maintain safety and reliability. As a result, MRO providers saw increasing long-term contracts, recurring revenue, and strong demand for both scheduled maintenance and unscheduled repair services.

Tightening aviation safety regulations and higher certification standards significantly fueled the MRO market. Aviation authorities around the world imposed more frequent inspections, mandatory component replacements, and rigorous airworthiness checks to ensure passenger safety and operational reliability. Furthermore, aircraft manufacturers and operators adopted predictive maintenance systems using data analytics, real-time monitoring, and digital diagnostics to comply with regulatory requirements. This drove demand for advanced MRO services, including structural repairs, engine diagnostics, and avionics upgrades. The push to reduce downtime, avoid safety violations, and prevent in-flight failures created a robust market for high-quality, compliance-focused maintenance operations.

Market Restraints:

A major restraint for the global MRO market was the high capital cost associated with setting up and maintaining MRO infrastructure. Establishing or expanding maintenance facilities, hangars, and specialized workshops required large investments in physical infrastructure, tooling, and skilled labor. Additionally, MRO companies needed to invest in advanced diagnostic equipment, training programs, and parts inventory, which increased operating costs. For smaller regional providers, this barrier limited scalability. Further, fluctuating demand for maintenance and economic downturns could lead to underutilized capacity. These financial and operational challenges constrained market entry, especially in underserved regions, slowing the expansion of MRO services.

The MRO market significantly influences global economies by supporting aviation safety, operational efficiency, and employment. Regular maintenance ensures reliable air travel, promoting tourism, trade, and business connectivity. The sector generates high-skilled jobs, from engineers to technicians, and supports ancillary industries such as spare parts, logistics, and aerospace manufacturing. Investments in MRO infrastructure stimulate regional economic development, particularly near major airports. Enhanced aircraft reliability reduces delays and accidents, improving consumer confidence in air travel. In developing regions, expanding MRO facilities also strengthen aviation capabilities, contributing to economic growth, connectivity, and the globalization of trade and tourism.

Segmental Analysis:

The Engine MRO segment was expected to witness the highest growth over the forecast period due to increasing demand for maintenance, repair, and overhaul of aircraft engines. Rising air traffic, growing airline fleets, and stringent safety regulations required frequent engine inspections, repairs, and part replacements. Advanced engines with complex technology also necessitated specialized expertise and equipment, which independent and airline-affiliated MRO providers offered. Additionally, airlines sought cost-efficient solutions to extend engine life, improve fuel efficiency, and reduce operational downtime. Predictive maintenance technologies and digital monitoring systems further supported segment growth, ensuring proactive engine servicing and optimized performance, driving sustained demand for engine-focused MRO services globally.

The Widebody Aircraft segment, including models such as the Airbus A350 and Boeing 787, was projected to witness the highest growth over the forecast period. Increasing long-haul international travel and airline fleet expansion fueled demand for MRO services specific to widebody aircraft. These aircraft require complex maintenance due to larger engines, advanced avionics, and structural components. Airlines prioritized reliable, cost-effective solutions to minimize downtime, maintain operational safety, and meet regulatory standards. The trend of airlines modernizing fleets with fuel-efficient widebody aircraft increased the need for regular engine, airframe, and systems maintenance. MRO providers with expertise in widebody aircraft services were well-positioned to capitalize on this growth.

The Independent MRO Providers segment was expected to experience the highest growth due to increasing airline outsourcing and the need for cost-efficient maintenance solutions. Many airlines preferred independent providers over in-house MROs to reduce operational costs, benefit from specialized expertise, and access flexible capacity for routine and unscheduled maintenance. Independent MROs offered competitive pricing, advanced technologies, and quick turnaround times, making them attractive partners for both small and large operators. Expansion in emerging markets, coupled with global fleet growth, further fueled demand. Additionally, regulatory compliance requirements and rising complexity of modern aircraft systems created opportunities for independent MROs to provide specialized engine, avionics, and component repair services.

The North America region was expected to witness the highest growth in the civil aircraft and helicopter MRO market during the forecast period. The region’s well-established aviation infrastructure, high airline fleet concentration, and extensive commercial and business aviation operations supported MRO expansion.

Airlines and operators increasingly outsourced maintenance to reduce costs and improve efficiency, while independent MRO providers offered advanced services with faster turnaround times. Regulatory oversight from the FAA and strict safety compliance ensured sustained demand for maintenance services.

Additionally, the presence of major aircraft manufacturers, strong R&D investments, and a focus on fleet modernization reinforced North America as a dominant and fast-growing market for both fixed-wing and rotary-wing aircraft MRO services. For instance, in Febraury 2025, CCC announced a government-to-government contract with Montenegro’s Ministry of Defense for MRO services provided by Bell Textron Canada Limited. The agreement supported the continued operation of Bell 505 and 412 helicopters acquired in 2020, ensuring aircraft reliability and longevity. By facilitating such contracts through the International Prime Contractor service, CCC strengthened North America’s civil aircraft and helicopter MRO market, enhancing regional service capabilities and reinforcing the prominence of Canadian vertical lift manufacturers in global defense aviation.

Thus, such factors are expected to drive the growth of above market in this region.

To Learn More About This Report - Request a Free Sample Copy

The civil aircraft and helicopter MRO market is highly competitive, with established players and emerging third-party providers vying for contracts. Key competitors focus on technological innovation, expanding service networks, and strategic partnerships to secure airline contracts. Companies differentiate through specialized services such as engine overhaul, avionics upgrades, and line maintenance. Regional expansions and acquisitions help firms capture growing markets, particularly in Asia-Pacific and the Middle East. Cost efficiency, service quality, and turnaround time are critical competitive factors. Major market participants invest in training programs, advanced diagnostic tools, and predictive maintenance technologies to strengthen their market position and sustain long-term growth.

The 20 major players for above market:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the massive increase in the global commercial aircraft fleet, particularly in the Asia-Pacific region, requiring scheduled maintenance. Growth is also fueled by the increasing average age of existing aircraft, which necessitates more frequent and complex maintenance checks. Furthermore, strict aviation safety regulations imposed by bodies like the FAA and EASA mandate scheduled, non-negotiable MRO activity, ensuring consistent and sustained demand for services.

Q2. What are the main restraining factors for this market?

A key constraint is the high capital investment required to build and equip sophisticated MRO facilities and the substantial cost of highly specialized tooling and spare parts. The market also suffers from a severe shortage of skilled MRO technicians and engineers, leading to increased labor costs and operational bottlenecks. Additionally, extended maintenance turnaround times (TATs) can cause scheduling issues and revenue losses for airline operators.

Q3. Which segment is expected to witness high growth?

The Engine MRO Segment is projected to witness the highest growth, as modern, complex jet engines (like the next-generation geared turbofans) are the most expensive and technologically advanced parts of an aircraft. Their maintenance requires frequent, high-value shop visits and specialized proprietary processes. The high cost of new engines, coupled with the need to maximize the operational life of existing ones, guarantees continuous, high-revenue demand for engine MRO providers.

Q4. Who are the top major players for this market?

The MRO market is dominated by three main types of players: airline-owned facilities, specialized independent providers, and Original Equipment Manufacturers (OEMs). Top major players include Lufthansa Technik, GE Aviation, Safran S.A., and ST Engineering Aerospace. Competition is focused on providing comprehensive, integrated maintenance solutions and leveraging advanced technologies like predictive maintenance and data analytics to reduce downtime and increase service efficiency.

Q5. Which country is the largest player?

The United States is the largest country player in the Global Civil MRO Market, driven by the massive size of its domestic air travel industry and the presence of major MRO providers and leading aerospace OEMs. The country benefits from a vast existing MRO infrastructure, high government defense and civil aviation spending, and stringent regulatory oversight that ensures consistent demand for certified maintenance services across North America's immense fleet.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model