Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The global Deep Vein Thrombosis (DVT) market focuses on the prevention, diagnosis, and treatment of blood clots in deep veins, primarily in the legs. DVT is a serious cardiovascular condition that can lead to pulmonary embolism if untreated, driving demand for effective anticoagulants, thrombolytics, diagnostic imaging systems, and wearable monitoring devices. Rising prevalence due to aging populations, sedentary lifestyles, obesity, and post-surgical complications has increased awareness and healthcare spending. The market also benefits from technological advancements in imaging, minimally invasive procedures, and personalized therapy.

The global DVT market is driven by innovations in diagnostics, therapeutics, and preventive care. Advanced imaging techniques, including Doppler ultrasound, CT, and MRI, improve early detection and reduce complications. There is increasing adoption of direct oral anticoagulants (DOACs) and minimally invasive thrombectomy devices for safer, more effective treatment. Integration of wearable monitoring devices and AI-enabled predictive analytics enhances patient management and adherence. Growing awareness programs about DVT risks post-surgery or during prolonged immobility are expanding preventive measures.

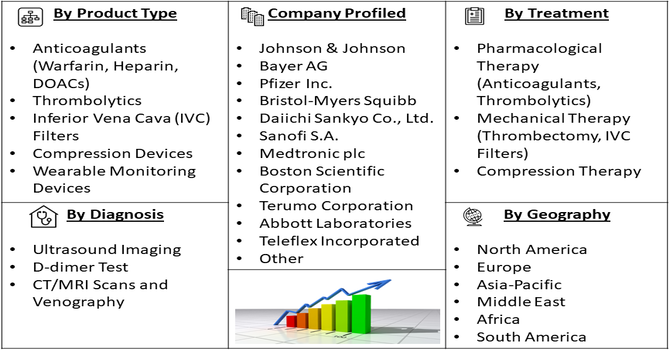

Segmentation: The global Deep Vein Thrombosis (DVT) market is segmented by Product Type (Anticoagulants (Warfarin, Heparin, DOACs), Thrombolytics, Inferior Vena Cava (IVC) Filters, Compression Devices, and Wearable Monitoring Devices), Diagnosis (Ultrasound Imaging, D-dimer Test, CT/MRI Scans and Venography), Treatment (Pharmacological Therapy (Anticoagulants, Thrombolytics), Mechanical Therapy (Thrombectomy, IVC Filters) and Compression Therapy), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing prevalence of Deep Vein Thrombosis (DVT) is a key driver of the global market. Aging populations, sedentary lifestyles, obesity, cancer, and post-surgical immobility contribute to higher DVT incidence worldwide. For instance, in 2023 World Obesity Federation, reported that more than one billion people in the world are now living with obesity, nearly 880 million adults and 159 million children and adolescents aged 5-19 years. Similarly, WHO reported that in 2022, there were an estimated 20 million new cancer cases.

Growing awareness of life-threatening complications such as pulmonary embolism has prompted early screening, preventive interventions, and timely treatment. Hospitals and clinics are increasingly adopting anticoagulants, thrombolytics, and mechanical devices to manage high-risk patients. Government and healthcare initiatives promoting preventive care and patient education further support market growth. This rising patient pool and enhanced focus on early detection and management continue to expand the global DVT market.

Advancements in diagnostic imaging, AI-powered ultrasound, wearable monitoring devices, and minimally invasive interventional therapies are driving growth in the global DVT market. Modern Doppler ultrasound, CT, and MRI technologies enable early and accurate detection of blood clots, improving clinical outcomes.

In May 2025, Fortis Hospital Mohali advanced the global DVT market by implementing state-of-the-art clot retrieval technologies under Dr. Ravul Jindal. The adoption of non-thrombolytic mechanical thrombectomy devices improved treatment safety, speed, and efficacy for patients with extensive clots, demonstrating the potential of advanced interventional solutions and driving broader clinical adoption and market growth in DVT management worldwide. Thus, the continuous research and development by medical device and pharmaceutical companies support innovation, broaden clinical applications, and strengthen adoption, positioning technological progress as a major growth driver for the DVT market.

Market Restraint:

High costs of DVT treatment and advanced diagnostic technologies remain a significant restraint for market growth. Anticoagulants, thrombolytics, imaging systems, and mechanical devices often require substantial investment, limiting access in low- and middle-income regions. Specialized infrastructure, trained personnel, and hospital-based interventions further increase healthcare expenditure. Limited insurance coverage and reimbursement challenges reduce patient affordability, particularly for novel therapies and minimally invasive procedures. These economic barriers restrict widespread adoption of advanced DVT management solutions, slowing market penetration in emerging economies. Until costs decrease and accessibility improves, the global DVT market may face constraints despite rising prevalence and technological advancements.

DVT imposes significant socioeconomic challenges, including healthcare costs, lost productivity, and long-term morbidity. Early diagnosis and effective treatment reduce hospital stays, prevent life-threatening complications like pulmonary embolism, and improve patient quality of life. Widespread preventive care, especially in high-risk populations such as post-surgical or immobile patients, lowers overall economic burden. However, limited access to advanced diagnostics and high-cost anticoagulants in low-income regions restricts equitable care. Investments in awareness programs, healthcare infrastructure, and affordable therapies help mitigate disparities.

Segmental Analysis:

The anticoagulants segment, including Warfarin, Heparin, and direct oral anticoagulants (DOACs), is expected to witness the highest growth over the forecast period. Increasing prevalence of DVT, atrial fibrillation, and post-surgical complications has driven demand for effective oral and injectable anticoagulants. DOACs are gaining preference due to ease of use, predictable pharmacokinetics, and reduced monitoring requirements. Growing awareness of preventive care and rising adoption in hospitals and clinics further fuel market expansion. Continuous R&D in safer, more targeted anticoagulants and favorable reimbursement policies also support growth, making anticoagulants a leading contributor to the DVT therapeutics market.

The ultrasound imaging segment is projected to witness the highest growth over the forecast period due to its non-invasive, cost-effective, and accurate diagnostic capabilities. Doppler and duplex ultrasound are widely used for early detection of DVT, enabling rapid clinical decisions and reducing complications such as pulmonary embolism. Increasing use in hospitals, diagnostic centers, and outpatient clinics, along with technological improvements like portable and AI-enabled devices, has boosted adoption. Awareness campaigns promoting timely DVT diagnosis and routine screening in high-risk populations also drive growth. The segment benefits from continuous innovation in image resolution, workflow efficiency, and integration with electronic health systems.

The pharmacological therapy segment, comprising anticoagulants and thrombolytics, is expected to witness significant growth due to increasing clinical adoption for DVT management. Anticoagulants prevent clot formation, while thrombolytics dissolve existing clots, providing comprehensive treatment options. Rising prevalence of DVT, post-operative complications, and chronic comorbidities like cancer and cardiovascular diseases drive demand. Innovations in safer, more targeted drugs with fewer side effects and simplified dosing regimens enhance patient adherence. Growing awareness among physicians and patients regarding early pharmacological intervention, coupled with supportive insurance coverage, further accelerates adoption across hospitals and specialty care centers globally.

The compression therapy segment is expected to witness the highest growth over the forecast period due to its proven efficacy in DVT prevention and management. Graduated compression stockings, pneumatic devices, and bandages help improve venous blood flow, reduce clot formation, and prevent post-thrombotic complications. Rising adoption in post-surgical, bedridden, and high-risk patients, along with growing awareness about preventive care, has fueled market expansion. Technological advancements in comfort, durability, and patient compliance have increased usage in hospitals and home care settings. Additionally, integration with multidisciplinary DVT management programs supports adoption, positioning compression therapy as a key segment in preventive strategies.

North America is expected to witness the highest growth in the DVT market over the forecast period due to advanced healthcare infrastructure, high prevalence of DVT risk factors, and widespread adoption of innovative diagnostics and therapies.

Strong hospital networks, skilled healthcare professionals, and early adoption of anticoagulants, thrombolytics, and compression devices enhance market penetration. Government initiatives, favorable reimbursement policies, and growing patient awareness further support growth. For instance, in 2024, The National Blood Clot Alliance and partners launched the “Get Out the Clot” campaign ahead of World Thrombosis Day to address gaps in patient care, standardize treatment, and expand access to innovations. This initiative strengthened North America’s DVT market by promoting awareness, improving care quality, and accelerating adoption of advanced diagnostics and therapies across healthcare settings.

Additionally, continuous R&D by leading pharmaceutical and medical device companies in the U.S. and Canada accelerates innovation and clinical adoption, making North America the largest and fastest-growing regional market for DVT management.

| Report Matrics | Details |

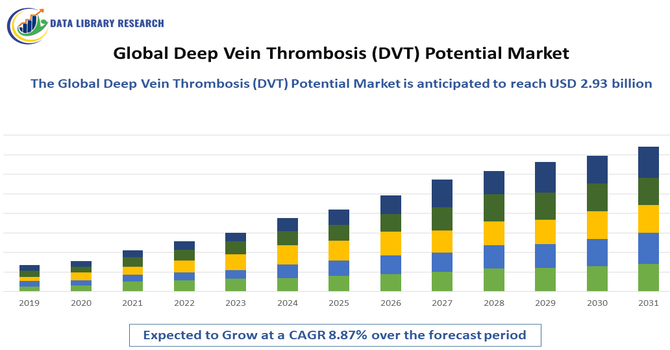

| Market Size Value | USD 2.93 billion |

| Growth Rate | CAGR of 8.87 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The DVT market is highly competitive, featuring pharmaceutical giants, medical device manufacturers, and diagnostic solution providers. Key players compete through product innovation, strategic partnerships, mergers, and acquisitions to enhance treatment and diagnostic portfolios. Pharmaceutical companies focus on novel anticoagulants, thrombolytics, and combination therapies, while device manufacturers develop advanced catheters, filters, and monitoring systems. Market entry barriers include stringent regulatory approvals, clinical trial requirements, and high development costs. Companies that provide cost-effective, clinically validated, and integrated DVT solutions gain a competitive edge. Continuous R&D, regional expansion, and collaborations with hospitals and research institutions drive market leadership and adoption worldwide.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is primarily driven by an aging global population and the rising prevalence of chronic conditions like obesity and cardiovascular diseases. Increased surgical procedures, prolonged hospitalization, and sedentary lifestyles significantly elevate DVT risks. Furthermore, advancements in diagnostic technologies and a growing awareness of pulmonary embolism risks fuel market expansion.

Q2. What are the main restraining factors for this market?

High costs associated with advanced anticoagulant therapies and surgical interventions act as significant barriers. Additionally, the risk of major bleeding complications linked to blood thinners often limits patient compliance. Stringent regulatory approval processes for new drugs and a lack of specialized medical infrastructure in emerging economies further hinder market growth.

Q3. Which segment is expected to witness high growth?

The Anticoagulants drug segment is expected to see substantial growth, particularly Direct Oral Anticoagulants (DOACs). These are favored over traditional heparin due to their ease of administration and lack of frequent monitoring. Additionally, the Compression Devices segment is rising rapidly as a non-invasive, preventive standard in post-surgical patient care.

Q4. Who are the top major players for this market?

Key industry leaders include pharmaceutical giants and medical device innovators such as Bristol-Myers Squibb, Pfizer, Bayer AG, Johnson & Johnson, and Sanofi. In the device sector, Medtronic, Cardinal Health, and Boston Scientific dominate by providing advanced venous stents and mechanical thrombectomy systems aimed at improving patient outcomes.

Q5. Which country is the largest player?

The United States is currently the largest player in the DVT market. This dominance is attributed to a sophisticated healthcare system, high healthcare expenditure, and the presence of major pharmaceutical companies. A proactive approach toward venous thromboembolism (VTE) prevention protocols in hospitals and high diagnostic rates further solidify its leadership.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model