Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The global electric capacitors market encompasses the production and sale of components that store and release electrical energy in circuits. Driven by demand from consumer electronics, automotive, and renewable energy sectors, the market includes various types—ceramic, electrolytic, and film capacitors—offering performance, reliability, and energy efficiency across applications.

The electric capacitors market is primarily driven by the rapid growth of consumer electronics, electric vehicles, and renewable energy systems, which require efficient energy storage and power management solutions. Rising demand for miniaturized, high-performance capacitors in smartphones, laptops, and industrial automation, along with advancements in capacitor materials and technologies, further propels market growth.

The electric capacitors market is witnessing trends such as the adoption of high-capacitance, low-equivalent series resistance (ESR) capacitors, and the integration of advanced dielectric materials like ceramic, tantalum, and polymer. Increasing miniaturization and energy-efficient designs are shaping component selection, while applications in electric vehicles, renewable energy storage, consumer electronics, and IoT devices are driving demand for specialized, high-performance capacitors. Additionally, manufacturers are focusing on improving reliability, thermal stability, and lifecycle performance to meet evolving industry standards and enhance integration into compact, high-frequency electronic circuits.

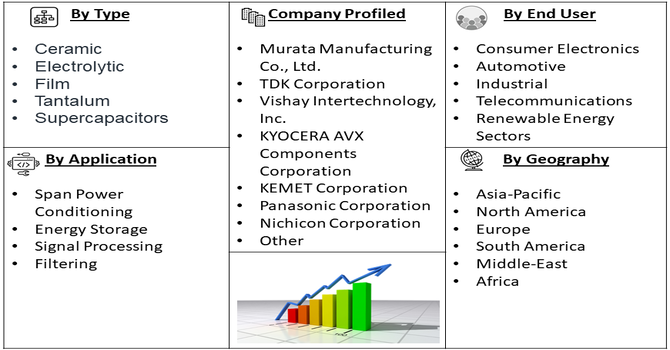

Segmentation: The Global Electric Capacitor Market is segmented based on Type (Ceramic, Electrolytic, Film, Tantalum, and Supercapacitors), Applications (Span Power Conditioning, Energy Storage, Signal Processing, and Filtering), End-Users (Consumer Electronics, Automotive, Industrial, Telecommunications, and Renewable Energy Sectors) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The rising adoption of electric vehicles (EVs) and renewable energy systems has significantly fueled the demand for high-performance capacitors. Electric vehicles require capacitors for power management, voltage stabilization, and fast energy storage to ensure efficient battery operation and reduced charging times. Similarly, renewable energy installations, including solar and wind power systems, rely on capacitors for energy conversion, storage, and grid stabilization. The push for greener energy solutions, government incentives for EV adoption, and increasing consumer awareness regarding sustainable technologies have all contributed to this trend. Consequently, manufacturers are investing in advanced ceramic and electrolytic capacitors capable of withstanding higher voltages and temperatures, further accelerating market growth globally.

Continuous innovations in capacitor technology, such as multilayer ceramic capacitors (MLCCs), polymeric film capacitors, and high-energy-density supercapacitors, have driven market expansion. Advances in material science, including doping, nanostructures, and hybrid composites, have improved capacitance, voltage tolerance, and operational longevity. Manufacturers are also developing compact, high-performance capacitors suitable for miniaturized electronics, aerospace, and industrial automation. These innovations enable higher efficiency, reduced heat generation, and better reliability in high-frequency and high-power applications. As industries demand smaller yet more powerful components, technological progress in capacitor design supports their integration across consumer electronics, automotive, and renewable energy sectors, propelling the global electric capacitors market forward.

Market Restraints:

Fluctuating costs of essential raw materials, including tantalum, aluminum, and specialty ceramics, pose significant challenges for capacitor manufacturers. Sudden price increases affect production costs and profitability, particularly for high-performance capacitors requiring rare or engineered materials. Additionally, global supply chain disruptions, such as semiconductor shortages, logistics delays, and geopolitical tensions, further complicate procurement and production schedules. These uncertainties hinder consistent manufacturing, slow product launches, and may lead end-users to seek alternative technologies. The combined effect of raw material volatility and supply chain instability restrains market growth, particularly for small and medium-scale capacitor producers dependent on steady, cost-effective material supply.

The global electric capacitors market has had a significant socioeconomic impact by enabling advancements in consumer electronics, electric vehicles, renewable energy, and industrial automation, driving technological progress and efficiency. Increased adoption of high-performance capacitors supports sustainable energy solutions, reduces carbon emissions, and enhances power reliability. The market has also created employment opportunities in manufacturing, R&D, and distribution, while fostering innovation in emerging economies. Improved electronic infrastructure enhances productivity across industries, contributing to economic growth and supporting societal shifts toward cleaner, energy-efficient technologies worldwide.

Segmental Analysis:

The ceramic capacitor segment dominated the electric capacitors market due to its high stability, low loss, and reliability in high-frequency applications. These capacitors are widely used in automotive electronics, consumer electronics, and industrial machinery for power filtering, energy storage, and decoupling purposes. Increasing demand for miniaturized and high-performance electronic devices, coupled with their long service life and ability to withstand extreme temperatures, has driven significant adoption. Technological advancements in multi-layer ceramic capacitors (MLCCs) have further enhanced capacitance density and efficiency. As electronic devices continue to become more compact and complex, ceramic capacitors are expected to witness the highest growth over the forecast period, reinforcing their critical role in modern electronics.

The power conditioning application segment is anticipated to lead growth in the electric capacitors market due to the increasing demand for efficient energy management and stable power supply. Capacitors play a vital role in maintaining voltage stability, filtering harmonics, and improving power factor in renewable energy systems, industrial machinery, and data centers. The rise in renewable energy adoption, including solar and wind energy, has created the need for capacitors capable of handling fluctuating loads and stabilizing electrical networks. Furthermore, smart grid initiatives and energy storage systems rely heavily on capacitors for efficient energy flow. As industries and utilities seek sustainable and reliable power solutions, the power conditioning segment is poised for significant expansion.

The consumer electronics end-user segment is expected to drive substantial growth in the electric capacitors market due to the rapid proliferation of smartphones, tablets, laptops, wearable devices, and smart home products. Capacitors are critical in these devices for energy storage, filtering, decoupling, and voltage stabilization, ensuring optimal performance and longevity. Increasing consumer preference for high-performance, miniaturized, and energy-efficient devices is boosting demand for advanced capacitor technologies, particularly multi-layer ceramic capacitors (MLCCs). Moreover, rising disposable income and technology adoption in emerging economies further fuel market growth. With continuous innovations in electronics and increasing reliance on portable and connected devices, consumer electronics will remain a dominant end-user segment throughout the forecast period.

The Asia Pacific region is projected to witness the highest growth in the electric capacitors market due to rapid industrialization, urbanization, and increasing electronics manufacturing in countries such as China, Japan, South Korea, and India. The region serves as a global hub for consumer electronics, automotive, and renewable energy production, driving strong demand for high-performance capacitors. Government initiatives to promote smart infrastructure, electric vehicles, and renewable energy projects further support market expansion.

Additionally, the presence of key capacitor manufacturers and ongoing R&D in advanced technologies enhances product availability and innovation. For instance, in September 2025, SK Keyfoundry, an 8-inch pure-play foundry in Korea, launched its Multi-Level Thick IMD process for capacitors, enabling up to three stacked inter-metal dielectric layers with a total thickness of 18 μm. The process achieved high breakdown voltage of 19,000 V and improved capacitance, enhancing device safety, reliability, and noise immunity. This innovation strengthened capacitor performance, driving adoption in digital isolation and electronic circuits, and is expected to boost growth in the Asia Pacific electric capacitors market.

Also, all above factors coupled with growing industrial automation and rising adoption of electronic devices among consumers are expected to sustain robust market growth in Asia Pacific.

| Report Matrics | Details |

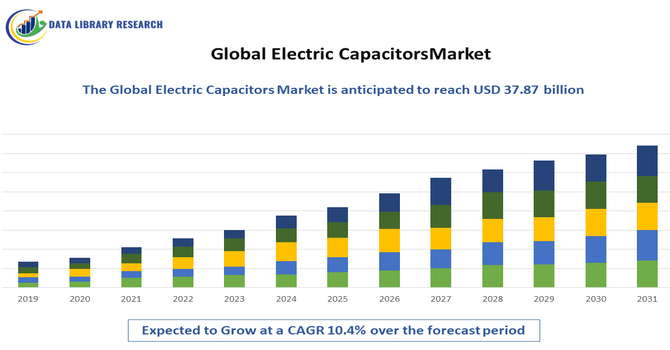

| Market Size Value | USD 37.87billion |

| Growth Rate | CAGR of 10.4% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The global electric capacitor market is highly competitive, characterized by the presence of major multinational manufacturers and innovative regional players. Key companies focus on continuous R&D, product innovation, and strategic partnerships to strengthen their market positions. Industry leaders like Murata Manufacturing, TDK Corporation, KEMET Corporation, Panasonic Corporation, and Vishay Intertechnology emphasize advanced capacitor technologies such as multi-layer ceramic capacitors (MLCCs), high-voltage film capacitors, and energy-efficient solutions. Companies also adopt mergers, acquisitions, and geographic expansion strategies to enhance production capabilities and meet growing demand across automotive, consumer electronics, industrial, and renewable energy sectors. The competitive environment encourages technological advancement, product differentiation, and cost optimization to capture market share.

The 20 major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The electric capacitors market is primarily driven by the massive expansion of the consumer electronics industry and the global shift toward automotive electrification (EVs). The demand for smaller, more functional devices, like smartphones and IoT gadgets, necessitates compact, high-performance capacitors. For EVs, high-voltage capacitors are critical for energy management in inverters and battery systems. Furthermore, advancements in 5G technology and the integration of renewable energy sources require reliable capacitor solutions for power stability and filtering.

Q2. What are the main restraining factors for this market?

The market faces significant restraints primarily related to the supply chain and cost. Volatile prices of raw materials, such as nickel, palladium, and specialized ceramic powders, lead to high and fluctuating production costs for manufacturers. Additionally, traditional capacitors have a lower energy density compared to batteries, limiting their application as primary energy sources in long-duration devices. Global supply chain disruptions can also cause material shortages and delays, impacting market stability.

Q3. Which segment is expected to witness high growth?

The Supercapacitors/Electric Double-Layer Capacitors (EDLCs) segment is projected to witness the highest growth. This is due to their exceptional power density, fast charge/discharge capabilities, and long cycle life, making them ideal for applications requiring quick bursts of power. By end-use, the Automotive sector, driven by the increasing production of electric and hybrid vehicles which utilize thousands of high-performance capacitors for power electronics, will continue its exponential demand.

Q4. Who are the top major players for this market?

The global market is dominated by large, established Asian and European component manufacturers. Top major players include Japanese giants Murata Manufacturing Co., Ltd., TDK Corporation, and Taiyo Yuden Co., Ltd.; South Korean conglomerate Samsung Electro-Mechanics Co., Ltd.; and key players like Kyocera AVX Components Corporation (formerly AVX/KEMET). These companies are leaders in Multilayer Ceramic Capacitors (MLCCs) and constantly invest in miniaturization technology.

Q5. Which country is the largest player?

The Asia-Pacific region holds the largest market share globally, primarily driven by China. China dominates due to its status as the world's largest manufacturing hub for consumer electronics, coupled with massive government and private investment in electric vehicle production and advanced telecommunications (5G). The strong regional presence of major capacitor manufacturers in China, Japan, and South Korea further solidifies APAC's leading position in terms of both production and consumption.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model