Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The global face recognition lockers market is experiencing robust growth as organizations and individuals increasingly demand secure, contactless, and convenient storage solutions across multiple sectors, including retail, healthcare, gyms, logistics and hospitality. Rising security concerns, growth in e-commerce and parcel delivery, and a broader trend toward smart, biometric-enabled physical infrastructure have significantly boosted the adoption of lockers that use facial recognition for access control. Technological advances especially in AI, machine learning, and 3D or infrared recognition systems have improved the accuracy, speed, and reliability of authentication, making face recognition lockers more viable and attractive.

The latest trends in the global face recognition lockers market reflect rapid technological innovation and changing user expectations — pushing the market toward smarter, more secure, and more integrated locker solutions. Another emerging pattern is cloud and IoT enabled management of locker fleets: lockers are increasingly connected to remote platforms for monitoring, usage analytics, access control, and maintenance. This allows operators (e.g. logistics firms, apartment complexes, offices) to manage many lockers across locations efficiently and gives users real time notifications, remote unlocking options, and a smoother user experience.

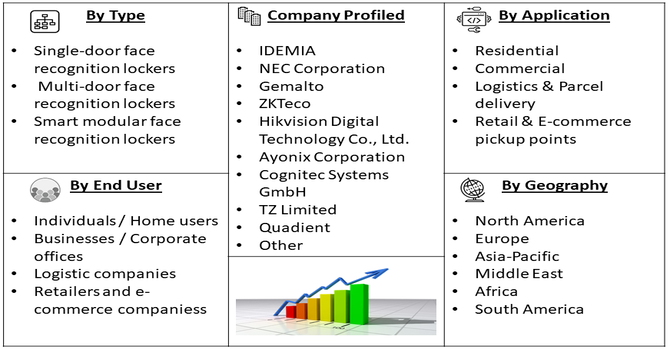

Segmentation: Global Face Recognition Lockers Market is segmented By Type (Single-door face recognition lockers, Multi-door face recognition lockers, Smart modular face recognition lockers), Application (Residential, Commercial, Logistics & Parcel delivery, Retail & E-commerce pickup points), End User (Individuals / Home users, Businesses / Corporate offices, Logistic companies, Retailers and e-commerce companies), Technology (2D facial recognition systems, 3D facial recognition systems, Infrared / Thermal facial recognition systems), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The primary driver for the face recognition lockers market is the growing need for secure, contactless access in residential, commercial, and public spaces. With increasing security concerns, theft prevention, and the need to protect sensitive items, facial recognition provides a reliable, non-transferable authentication method compared to traditional key, PIN, or card-based systems. For instance, in July 2025, Stadiums’ expanded use of facial authentication demonstrated high-capacity, secure access management, driving adoption of face recognition lockers and positively influencing the growth and innovation of the global face recognition lockers market.

In sectors like logistics and e-commerce, face recognition lockers enable secure parcel deliveries without human contact, ensuring both operational efficiency and safety. This rising emphasis on convenience, security, and hygiene is significantly driving adoption across multiple industries.

Another key driver is the incorporation of advanced AI, machine learning, and IoT-enabled technologies in face recognition lockers. Modern lockers can now accurately identify users under varying lighting conditions, recognize multiple users, and detect spoofing attempts, improving reliability and user confidence.

Additionally, integration with cloud platforms and smart building management systems allows operators to monitor locker usage remotely, track inventory, generate analytics, and provide real-time notifications to users. This automation and data-driven management reduce operational costs, enhance user experience, and make lockers scalable for large facilities, further boosting market growth. The trend toward smart infrastructure and Industry 4.0 adoption strongly supports increased deployment of intelligent face recognition lockers worldwide.

Market Restraints

The high initial costs of advanced biometric lockers, particularly those with AI-enabled 3D facial recognition and IoT connectivity, make them less accessible for small businesses and residential users. Privacy and data security concerns also pose a significant challenge, as facial data is highly sensitive and subject to strict regulations such as GDPR, requiring secure storage, encryption, and compliance protocols. Technical limitations, such as decreased recognition accuracy under poor lighting conditions, obstructions, or rapid environmental changes, can impact reliability and user confidence.

The global face recognition lockers market is significantly influenced by socioeconomic factors, as rising urbanization, increasing disposable incomes, and growing awareness of security and privacy drive adoption across commercial, residential, and institutional sectors. In developed economies, higher technological literacy and investment in smart infrastructure accelerate market growth, while in emerging regions, government initiatives promoting digital security and modernization of public facilities enhance demand. Additionally, societal concerns around safety, coupled with shifting workplace and educational norms, further stimulate adoption. Economic disparities, however, may limit penetration in low-income areas, highlighting the market’s sensitivity to both income levels and social awareness.

Segmental Analysis:

Smart modular face recognition lockers are emerging as a leading type due to their flexibility, scalability, and adaptability across various environments. Unlike traditional single- or multi-door lockers, modular systems can be customized in size, configuration, and number of compartments, allowing businesses and institutions to efficiently manage space and user requirements. They are increasingly adopted in logistics hubs, offices, gyms, and residential complexes where varying locker sizes and smart access features are required, enhancing operational efficiency and user convenience.

The logistics and parcel delivery sector is one of the fastest-growing applications for face recognition lockers. With the boom in e-commerce and increasing demand for last-mile delivery solutions, secure lockers enable contactless parcel collection and drop-off. Facial recognition ensures that only the intended recipient can access the package, reducing theft and misdelivery risks. This application is particularly critical in urban areas, residential complexes, and corporate campuses where multiple parcels are delivered daily.

Corporate offices represent a major end-user segment as businesses increasingly adopt face recognition lockers to secure personal belongings, sensitive documents, and IT equipment. These lockers improve workplace security while providing employees with convenient, contactless access. Integration with office management systems allows administrators to monitor usage, manage multiple users, and streamline facility operations, supporting broader corporate digitalization initiatives.

3D facial recognition systems are gaining traction over 2D systems due to higher accuracy, reliability, and enhanced security. Unlike 2D recognition, 3D systems capture depth and contours of a face, making them less susceptible to lighting variations, facial expressions, or spoofing attempts with photographs. This makes them ideal for high-security applications in logistics, corporate offices, and public facilities where accuracy and fraud prevention are critical.

North America is a dominant regional market for face recognition lockers due to advanced technology adoption, strong security awareness, and widespread use of smart infrastructure in residential and commercial sectors.

The region has a high concentration of e-commerce operations, corporate offices, and tech-forward residential complexes, which drives demand for smart, AI-enabled locker systems. Supportive regulations, investment in smart building technologies, and robust R&D activities further strengthen market growth in this region. For instance, in May 2023, Parks Associates’ whitepaper highlighted growing consumer interest in AI-driven face recognition for smart home security, emphasizing convenience and enhanced safety. While 86% valued AI features in purchase decisions, 26% expressed data privacy concerns. These insights influenced the US face recognition lockers market by driving innovation, increasing adoption in residential and commercial sectors, and prompting solutions addressing privacy and security challenges.

Similarly, in 2020, Rite Aid’s deployment of facial recognition systems across 200 U.S. stores marked one of the largest retail rollouts, showcasing the technology’s scalability and operational potential. Its use in diverse urban neighborhoods highlighted both market expansion opportunities and privacy concerns, influencing the U.S. face recognition lockers market by accelerating adoption while prompting discussions on ethical use and regulatory compliance.

| Report Matrics | Details |

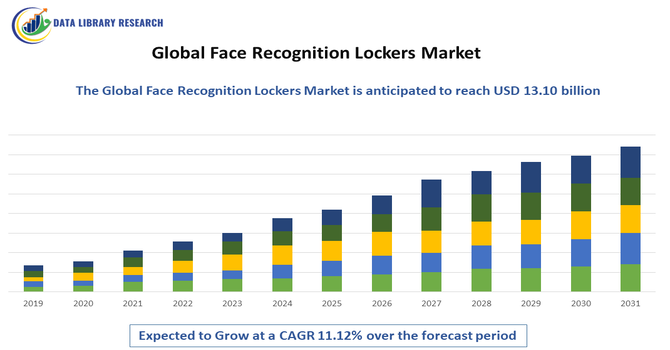

| Market Size Value | USD 13.10 billion |

| Growth Rate | CAGR of 11.12% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive terrain in the global face recognition lockers market is crowded and evolving rapidly, shaped by a mixture of long standing security and access control firms, smart locker specialists, and emerging technology providers. Key players compete primarily on the basis of facial recognition accuracy and robustness (2D, 3D, thermal, AI/ML), product range (single-door, multi door, modular lockers, parcel lockers), integration capabilities (IoT/cloud, building/security infrastructure, package management systems), and service footprint (global vs regional). Strategic partnerships, alliances, and M&A are commonplace as companies aim to combine hardware, biometric software, cloud services, and locker management platforms into unified solutions — blurring lines between security systems, smart logistics, and access control offerings.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is primarily driven by the rising demand for enhanced security and the push for contactless, convenient access solutions. The need for hygienic, touchless interactions, accelerated by recent global health concerns, boosts adoption in public spaces like gyms, airports, and offices. Also, the expansion of smart city initiatives requiring integrated access control fuels demand.

Q2. What are the main restraining factors for this market?

The main hurdles are the high initial investment cost required to implement these advanced locker systems, which often includes complex hardware and software integration. Significant public concerns regarding data privacy and the security of stored biometric information, along with evolving government regulations on data usage, also slow down market growth.

Q3. Which segment is expected to witness high growth?

The airport and transportation application segment is anticipated to witness the highest growth. Airports require seamless, high-security, and rapid access management for passengers and staff. Face recognition lockers offer the perfect contactless solution to enhance efficiency during processes like baggage drop-off and staff access control across facilities.

Q4. Who are the top major players for this market?

The market includes key players who specialize in biometric technology and access control systems. Major global players often include large technology corporations like NEC Corporation, Thales, and IDEMIA, who leverage their expertise in facial recognition software and comprehensive smart city solutions to dominate the hardware and integrated locker system space.

Q5. Which country is the largest player?

The United States, within the North American region, currently holds the largest market share. This dominance is due to high technological adoption rates, established smart infrastructure, significant investments in advanced security systems across commercial and government sectors, and strong emphasis on high-level identity verification technologies.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model