Human Growth Hormone Treatment and Drug Market Overview and Analysis:

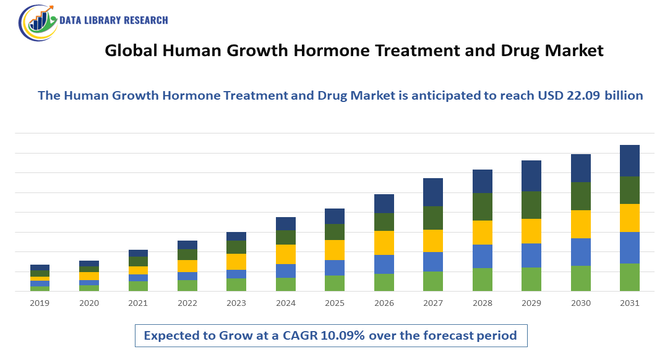

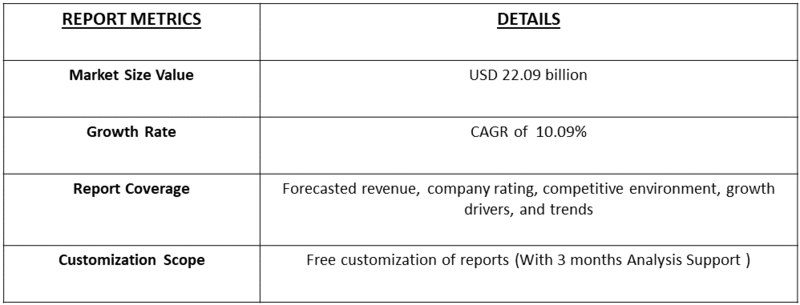

- The Global Human Growth Hormone (HGH) Treatment and Drug Market is a rapidly expanding sector, valued at around USD 7.2 billion in 2025 and projected to reach USD 22.09 billion by 2032, growing at a strong CAGR of 10.09% from 2025-2032.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Human Growth Hormone (HGH) Treatment and Drug Market involves the production, distribution, and use of HGH therapies for treating growth hormone deficiencies, pediatric growth disorders, and adult endocrine conditions. It includes recombinant HGH drugs, injection devices, and related therapies, driven by rising awareness, technological advancements, and increasing prevalence of growth disorders and aging-related hormonal imbalances worldwide.

The Global Human Growth Hormone (HGH) Treatment and Drug Market is primarily driven by the rising prevalence of growth hormone deficiencies in children and adults, coupled with increasing awareness among healthcare providers and patients about the benefits of HGH therapy. Technological advancements in recombinant DNA technology have improved drug efficacy and safety, while expanding applications in anti-aging, metabolic disorders, and muscle-wasting conditions further fuel demand.

Human Growth Hormone Treatment and Drug Market Latest Trends

The Global Human Growth Hormone (HGH) Treatment and Drug Market is witnessing significant trends, including a shift toward recombinant HGH therapies and long-acting formulations that improve patient compliance. Personalized treatment plans based on genetic profiling and hormone level monitoring are gaining traction. The rise of digital health platforms and telemedicine has enabled remote monitoring and adherence support. Increasing off-label usage in anti-aging and wellness segments is also observed, though regulated. Additionally, collaborations between biotech firms and healthcare providers for drug innovation and improved delivery systems are shaping the competitive landscape. These trends are enhancing market growth, efficiency, and patient outcomes globally.

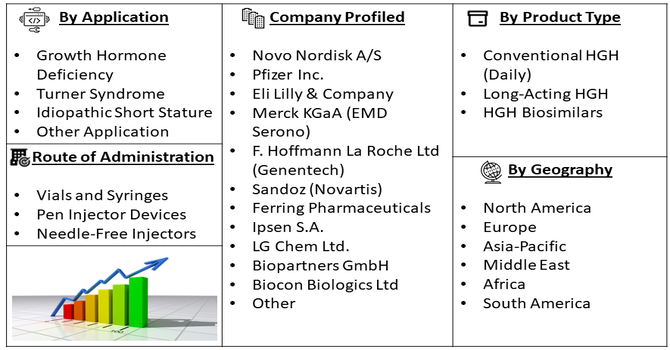

Segmentation: The Human Growth Hormone (HGH) market is segmented by Product Type (Conventional HGH (Daily), Long-Acting HGH and HGH Biosimilars), Application (Growth Hormone Deficiency, Turner Syndrome, Idiopathic Short Stature and Other Application), Route of Administration (Vials and Syringes, Pen Injector Devices and Needle-Free Injectors), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

- Introduction of Long-Acting Formulations and Improved Compliance

A major driver is the successful introduction and rapid adoption of long-acting Human Growth Hormone (HGH) formulations. Historically, HGH therapy required daily injections, which led to significant challenges with patient adherence, particularly in children and adolescents. New, innovative drug delivery systems allow for once-weekly administration, fundamentally changing the burden of treatment. This significant improvement in convenience and compliance is making HGH therapy more manageable and effective for long-term use.

As more pharmaceutical companies secure regulatory approvals for these once-weekly products and integrate user-friendly injection pens, the demand from both clinicians and patients will continue to accelerate market growth globally. For instance, SKYTROFA/TRANSCON hGH (lonapegsomatropin-tcgd) was a pegylated, long-acting human growth hormone designed for once-weekly subcutaneous administration. It had been approved in the US and EU for pediatric patients with growth failure due to inadequate GH levels, acting via GH receptors to regulate metabolism, protein synthesis, fat breakdown, and chondrocyte development. Its successful regulatory approvals and clinical adoption significantly boosted the acceptance and growth of long-acting HGH formulations globally.

- Expanding Indications and Enhanced Diagnostic Accuracy

The market is significantly expanding due to an increase in the number of treatable conditions, coupled with more accurate diagnostic tools. Beyond the traditional treatment of Pediatric Growth Hormone Deficiency (GHD), HGH is increasingly prescribed for conditions like Turner Syndrome, Idiopathic Short Stature (ISS), and specific adult GHD cases. Advances in diagnostic testing and increased awareness among pediatricians and endocrinologists allow for earlier and more precise identification of patients who can benefit. This combination of an expanded patient pool across both pediatric and adult populations, alongside the clinical necessity of the treatment, ensures a sustained and powerful growth trajectory for the market.

Market Restraints:

- High Treatment Costs and Regulatory Scrutiny

The primary constraint on the HGH market is the extremely high cost of therapy, which often involves years of treatment, placing a heavy financial burden on patients and healthcare systems. Although HGH is a life-changing treatment, its premium price limits accessibility, especially in developing economies or for patients without comprehensive insurance coverage. Furthermore, due to the history of HGH misuse in anti-aging and athletic performance enhancement, the market faces intense regulatory scrutiny. This scrutiny translates into complex and strict prescribing guidelines and rigorous authorization procedures, which can delay or deny treatment access even for legitimate medical cases.

Socio-Economic Impact on Human Growth Hormone Treatment and Drug Market

The HGH treatment market has considerable socioeconomic impact, improving quality of life for patients with growth hormone deficiencies and related conditions. Pediatric patients experience normalized growth, while adults benefit from enhanced metabolic and musculoskeletal health. Wider access to HGH therapies reduces long-term healthcare costs by preventing complications associated with hormone deficiencies. Moreover, the market generates employment opportunities in research, manufacturing, and clinical services. However, high treatment costs and unequal access in low-income regions create disparities. Public health initiatives and insurance coverage expansions help mitigate these challenges, enabling broader societal benefits while supporting economic growth within the biotechnology and pharmaceutical sectors.

Segmental Analysis:

- Long-Acting HGH segment is expected to witness the highest growth over the forecast period

The Long-Acting Human Growth Hormone (HGH) segment is expected to witness the highest growth over the forecast period due to its ability to improve patient compliance and convenience. Traditional daily HGH injections often pose challenges for adherence, whereas long-acting formulations reduce injection frequency, enhancing therapeutic outcomes and quality of life. Advances in drug delivery technologies, including sustained-release formulations and PEGylation, have further improved stability and efficacy. Rising awareness among physicians and patients about these benefits, coupled with strong clinical support, is driving adoption. Additionally, regulatory approvals and increasing availability in both developed and emerging markets are supporting market expansion, positioning long-acting HGH as a dominant growth segment.

- Vials and Syringes segment is expected to witness the highest growth over the forecast period

The Vials and Syringes segment is projected to witness the highest growth over the forecast period, driven by their widespread use for precise dosing of HGH therapies. Vials provide flexibility in dose adjustments, while prefilled syringes improve convenience and minimize dosing errors, which is critical for pediatric and adult patients. The segment benefits from advancements in user-friendly, pen-injection devices that enhance safety, portability, and adherence. Rising patient populations requiring growth hormone therapy, along with growing hospital, clinic, and homecare adoption, are accelerating demand. Additionally, healthcare providers increasingly prefer these delivery methods for accurate dosing and monitoring, reinforcing their dominance in the global HGH treatment and drug market.

- Growth Hormone Deficiency segment is expected to witness the highest growth over the forecast period

The Growth Hormone Deficiency (GHD) segment is expected to witness the highest growth over the forecast period due to increasing diagnosis rates in both children and adults. In pediatric patients, untreated GHD leads to stunted growth, whereas in adults it can cause metabolic issues, reduced bone density, and diminished quality of life. Rising awareness among caregivers, patients, and healthcare professionals, combined with improved diagnostic techniques and screening programs, is boosting treatment adoption. Technological advancements in recombinant HGH formulations and supportive reimbursement policies are further driving market penetration. The segment’s growth is also fueled by expanding clinical research and patient support initiatives, making GHD the largest application area for HGH therapies globally.

- North America region is expected to witness the highest growth over the forecast period

The North America region is expected to witness the highest growth in the HGH treatment and drug market due to high healthcare expenditure, advanced medical infrastructure, and greater awareness of hormone therapies. Increasing prevalence of growth hormone deficiencies, combined with rising adoption of long-acting formulations and innovative delivery devices, further supports market growth. For instance, an article published by NCBI in April 2025, reported that the U.S., adult GHD prevalence ranged from 0.2 (confirmed) to 37.0 (confirmed plus at-risk) per 100,000. Among 268 confirmed and 54,310 at-risk individuals, average age was 50, with a majority being female. GH treatment was initiated in 9.7% of confirmed cases and 3.1% of at-risk individuals. Treated patients had more endocrine conditions, while untreated patients showed higher metabolic and cardiovascular comorbidities, and only 32.2% remained on therapy throughout follow-up. Thus, such stats indicate high number of GHD cases in US, thereby driving the growth of above market in the North American region.

The U.S. and Canada have robust regulatory frameworks and strong access to specialty clinics for growth hormone disorders, facilitating early diagnosis and treatment. Additionally, favorable insurance coverage and reimbursement policies encourage patients to seek treatment. Strong presence of leading HGH manufacturers and ongoing clinical research also reinforce North America’s position as the fastest-growing regional market globally. For instance, Cigna Healthcare had implemented a new Evaluation and Management (E/M) Coding Accuracy (R49) policy on October 1, 2025, to address overbilling of high-level E/M codes. The policy reviewed claims billed with CPT codes 99204-99205, 99214-99215, and 99244-99245, adjusting reimbursement only when documentation did not support the reported level. Providers could submit records for reconsideration or appeal if original coding was justified, ensuring accurate coverage, timely payments, and adherence to AMA guidelines for insurance reimbursement across North America.

Thus, such factors for above market in the region.

To Learn More About This Report - Request a Free Sample Copy

Human Growth Hormone Treatment and Drug Market Competitive Landscape

The competitive landscape of the HGH treatment and drug market is dominated by major biotechnology and pharmaceutical companies investing in research, development, and strategic partnerships. Key players focus on innovation in recombinant HGH production, long-acting formulations, and improved delivery devices. Mergers, acquisitions, and collaborations enhance product pipelines and global market presence. Market players also emphasize regulatory compliance and clinical trial advancements to gain a competitive advantage. Emerging regional companies are expanding into developing markets, intensifying competition. Price strategies, patient support programs, and distribution networks are critical for differentiation. Continuous innovation and strategic partnerships define the highly competitive, growth-driven global HGH market.

The major players for the above market:

- Novo Nordisk A/S

- Pfizer Inc.

- Eli Lilly & Company

- Merck KGaA (EMD Serono)

- F. Hoffmann La Roche Ltd (Genentech)

- Sandoz (Novartis)

- Ferring Pharmaceuticals

- Ipsen S.A.

- LG Chem Ltd.

- GeneScience Pharmaceuticals

- Anhui Anke Biotechnology

- Ascendis Pharma A/S

- Teva Pharmaceutical Industries Ltd.

- Changchun High Tech Industries

- Shenzhen Kexing Pharmaceutical Co.

- JCR Pharmaceuticals Co. Ltd.

- Daewoong Pharmaceutical Co. Ltd.

- Biopartners GmbH

- Biocon Biologics Ltd

Recent Development

- In June 2025, Ascendis Pharma A/S announced that the U.S. FDA approved SKYTROFA (lonapegsomatropin-tcgd), developed as TransCon hGH, for adult growth hormone deficiency (GHD) treatment. The therapy, a prodrug of somatropin, had previously been approved in 2021 for pediatric GHD. Administered once weekly, it provided sustained release of active, unmodified human growth hormone, offering improved convenience and therapeutic outcomes.

- In June 2023, Pfizer Inc. and OPKO Health Inc. announced that the U.S. FDA approved NGENLA (somatrogon-ghla), a once-weekly human growth hormone analog. The therapy was indicated for treating pediatric patients aged three years and older experiencing growth failure due to insufficient endogenous growth hormone secretion. This approval marked a significant advancement in convenient, long-acting HGH treatment for children.

Frequently Asked Questions (FAQ) :

Q1. What are the main growth-driving factors for this market?

The primary driver is the increasing diagnosis and awareness of growth hormone deficiency (GHD) in children and the recognition of GHD-related complications in adults. Significant advancements in recombinant DNA technology have made synthetic HGH safer and more accessible than earlier forms. Furthermore, the development of long-acting HGH formulations, which require less frequent injections (e.g., weekly instead of daily), greatly improves patient compliance and quality of life, boosting demand and market growth.

Q2. What are the main restraining factors for this market?

The major restraint is the high cost associated with HGH therapy, which often requires treatment spanning several years and places a significant financial burden on patients and healthcare systems. Although most developed markets offer insurance coverage, coverage criteria can be strict and complex. Additionally, the historical issue of misuse and abuse of HGH in sports and anti-aging contexts, while distinct from legitimate medical use, contributes to a negative public perception and stringent regulatory scrutiny, potentially slowing market expansion.

Q3. Which segment is expected to witness high growth?

The Long-Acting HGH Segment is projected to witness the highest growth. Traditional HGH therapy requires daily subcutaneous injections, which leads to poor compliance, especially in pediatric patients. The new generation of long-acting drugs, administered once per week, significantly addresses this barrier. As more long-acting products receive regulatory approval and enter the market, offering substantial benefits in terms of patient adherence, convenience, and treatment efficacy, this segment will rapidly capture market share from traditional daily formulations.

Q4. Who are the top major players for this market?

The HGH market is dominated by global biopharmaceutical companies with extensive expertise in complex biologic manufacturing. Top major players include Novo Nordisk A/S, Pfizer Inc., Merck KGaA, and Eli Lilly and Company. These companies compete fiercely by investing heavily in next-generation long-acting technologies and developing sophisticated injection devices. Their existing global infrastructure for manufacturing, distribution, and clinical development ensures they maintain a leading position in this high-value therapeutic area.

Q5. Which country is the largest player?

The United States, within the North American region, is the largest country market. This dominance is due to the country's well-established clinical practice guidelines for GHD diagnosis and treatment, a large number of specialized endocrinologists, and high per-capita healthcare spending. Furthermore, the presence of major pharmaceutical companies and a generally favorable reimbursement environment for complex specialty drugs ensure that the U.S. continues to lead both in terms of market value and the early adoption of innovative HGH formulations.

List of Figures

Figure 1: Global Human Growth Hormone Treatment and Drug Market Revenue Breakdown (USD Billion, %) by Region, 2022 & 2029

Figure 2: Global Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 1, 2022 & 2029

Figure 3: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 4: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 5: Global Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 2, 2022 & 2029

Figure 6: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 7: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 8: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 9: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 10: Global Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 3, 2022 & 2029

Figure 11: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 12: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 13: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 14: Global Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 15: Global Human Growth Hormone Treatment and Drug Market Value (USD Billion), by Region, 2022 & 2029

Figure 16: North America Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 1, 2022 & 2029

Figure 17: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 18: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 19: North America Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 2, 2022 & 2029

Figure 20: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 21: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 22: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 23: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 24: North America Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 3, 2022 & 2029

Figure 25: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 26: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 27: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 28: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 29: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by U.S., 2018-2029

Figure 30: North America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Canada, 2018-2029

Figure 31: Latin America Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 1, 2022 & 2029

Figure 32: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 33: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 34: Latin America Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 2, 2022 & 2029

Figure 35: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 36: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 37: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 38: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 39: Latin America Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 3, 2022 & 2029

Figure 40: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 41: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 42: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 43: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 44: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Brazil, 2018-2029

Figure 45: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Mexico, 2018-2029

Figure 46: Latin America Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Rest of Latin America, 2018-2029

Figure 47: Europe Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 1, 2022 & 2029

Figure 48: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 49: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 50: Europe Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 2, 2022 & 2029

Figure 51: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 52: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 53: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 54: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 55: Europe Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 3, 2022 & 2029

Figure 56: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 57: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 58: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 59: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 60: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by U.K., 2018-2029

Figure 61: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Germany, 2018-2029

Figure 62: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by France, 2018-2029

Figure 63: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Italy, 2018-2029

Figure 64: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Spain, 2018-2029

Figure 65: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Russia, 2018-2029

Figure 66: Europe Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Rest of Europe, 2018-2029

Figure 67: Asia Pacific Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 1, 2022 & 2029

Figure 68: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 69: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 70: Asia Pacific Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 2, 2022 & 2029

Figure 71: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 72: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 73: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 74: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 75: Asia Pacific Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 3, 2022 & 2029

Figure 76: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 77: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 78: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 79: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 80: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by China, 2018-2029

Figure 81: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by India, 2018-2029

Figure 82: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Japan, 2018-2029

Figure 83: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Australia, 2018-2029

Figure 84: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Southeast Asia, 2018-2029

Figure 85: Asia Pacific Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Rest of Asia Pacific, 2018-2029

Figure 86: Middle East & Africa Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 1, 2022 & 2029

Figure 87: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 88: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 89: Middle East & Africa Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 2, 2022 & 2029

Figure 90: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 91: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 92: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 93: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 94: Middle East & Africa Human Growth Hormone Treatment and Drug Market Value Share (%), By Segment 3, 2022 & 2029

Figure 95: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 96: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 97: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 98: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Others, 2018-2029

Figure 99: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by GCC, 2018-2029

Figure 100: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by South Africa, 2018-2029

Figure 101: Middle East & Africa Human Growth Hormone Treatment and Drug Market Forecast (USD Billion), by Rest of Middle East & Africa, 2018-2029

List of Tables

Table 1: Global Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 2: Global Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 3: Global Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 4: Global Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Region, 2018-2029

Table 5: North America Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 6: North America Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 7: North America Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 8: North America Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 9: Europe Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 10: Europe Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 11: Europe Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 12: Europe Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 13: Latin America Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 14: Latin America Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 15: Latin America Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 16: Latin America Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 17: Asia Pacific Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 18: Asia Pacific Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 19: Asia Pacific Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 20: Asia Pacific Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 21: Middle East & Africa Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 22: Middle East & Africa Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 23: Middle East & Africa Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 24: Middle East & Africa Human Growth Hormone Treatment and Drug Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Research Process

Data Library Research are conducted by industry experts who offer insight on

industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager

and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

![research-methodology1]()

Primary Research

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary Research

Secondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size Estimation

Both, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model

![research-methodology2]()